As the craze of earnings season draws to a close, here’s a look back at some of the most exciting (and some less so) results from Q1. Today, we are looking at infrastructure stocks, starting with Excelerate Energy (NYSE:EE).

Energy infrastructure companies build, own, and operate assets including pipelines, storage facilities, and processing plants that transport and handle oil, natural gas, and related products. These businesses often generate fee-based revenues providing cash flow stability. Tailwinds include growing production volumes requiring expanded takeaway capacity and export infrastructure demand. Long-term contracts with creditworthy counterparties reduce commodity price exposure. Headwinds include permitting and regulatory challenges delaying new projects, environmental opposition to pipeline construction, and potential long-term demand decline from energy transition. High capital intensity and interest rate sensitivity affecting financing costs present additional considerations.

The 8 infrastructure stocks we track reported a strong Q1. As a group, revenues beat analysts’ consensus estimates by 14.9%.

Amidst this news, share prices of the companies have had a rough stretch. On average, they are down 5.8% since the latest earnings results.

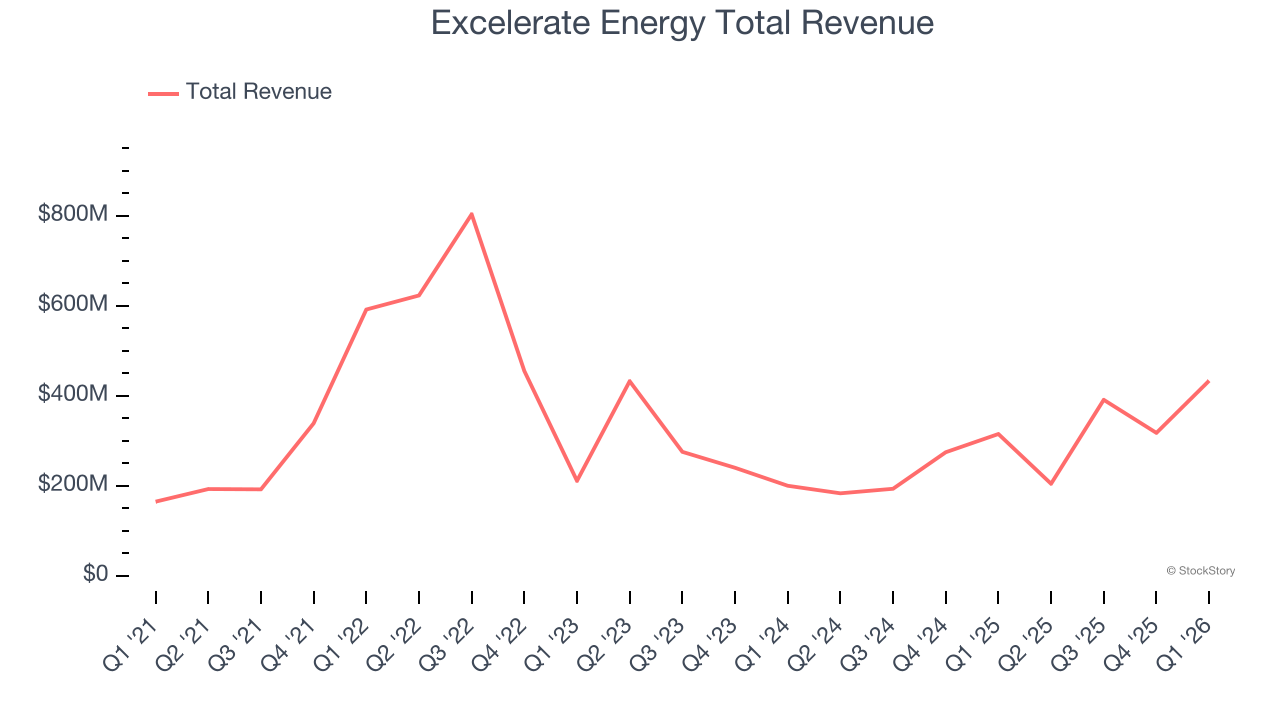

Excelerate Energy (NYSE:EE)

Operating specialized vessels that can deliver up to 1.2 billion cubic feet of natural gas per day, Excelerate Energy (NYSE:EE) provides liquified natural gas regasification services using floating vessels that convert LNG back into natural gas.

Excelerate Energy reported revenues of $433.4 million, up 37.6% year on year. This print exceeded analysts’ expectations by 26.4%. Despite the top-line beat, it was still a mixed quarter for the company with a decent beat of analysts’ EBITDA estimates but a significant miss of analysts’ EPS estimates.

Unsurprisingly, the stock is down 4.8% since reporting and currently trades at $32.70.

Is now the time to buy Excelerate Energy? Access our full analysis of the earnings results here, it’s free.

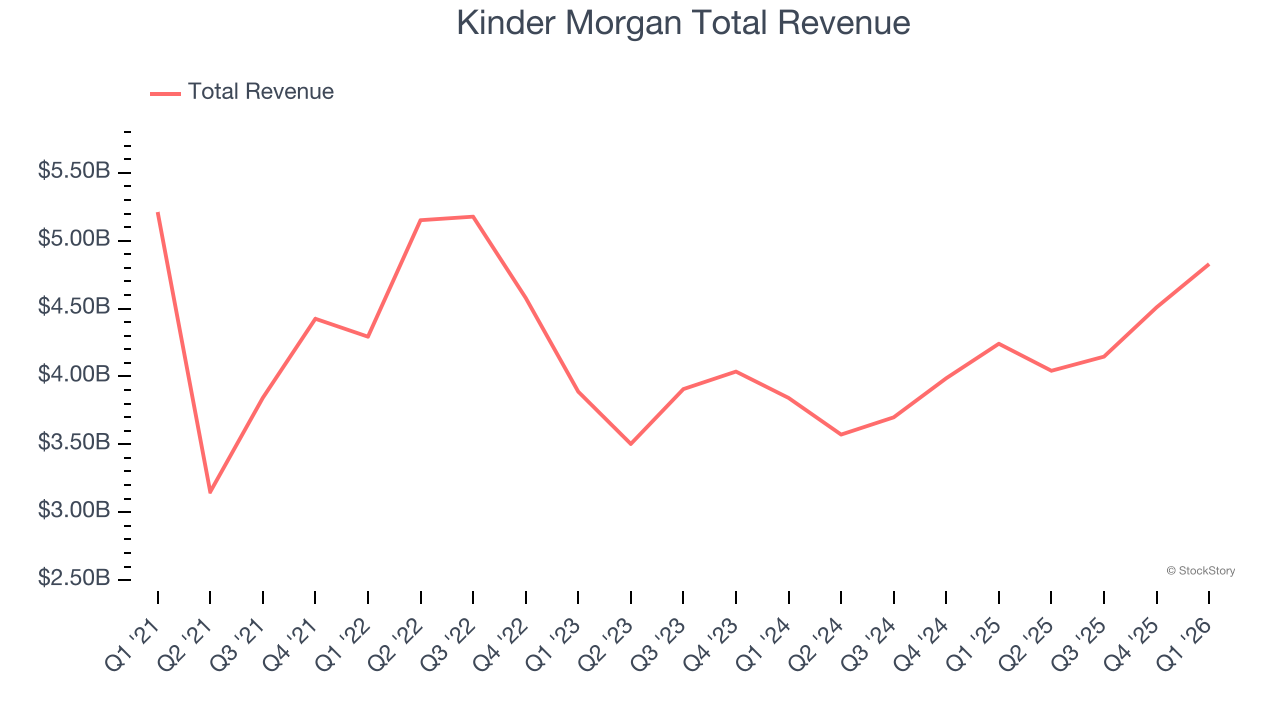

Best Q1: Kinder Morgan (NYSE:KMI)

Operating what amounts to the toll roads of the energy industry, Kinder Morgan (NYSE:KMI) transports natural gas, refined petroleum products, and crude oil through its pipeline network across North America.

Kinder Morgan reported revenues of $4.83 billion, up 13.8% year on year, outperforming analysts’ expectations by 3.3%. The business had a stunning quarter with a beat of analysts’ EPS and EBITDA estimates.

Although it had a fine quarter compared to its peers, the market seems unhappy with the results as the stock is down 2.8% since reporting. It currently trades at $30.93.

Is now the time to buy Kinder Morgan? Access our full analysis of the earnings results here, it’s free.

Weakest Q1: Calumet (NASDAQ:CLMT)

With roots dating back to 1919 and facilities strategically positioned from Louisiana to Montana, Calumet (NASDAQ:CLMT) refines crude oil into specialty products like lubricating oils, solvents, and waxes used in cosmetics, batteries, and industrial applications.

Calumet reported revenues of $1.03 billion, up 3.6% year on year, exceeding analysts’ expectations by 8%. Still, it was a softer quarter as it posted a significant miss of analysts’ EBITDA and EPS estimates.

Calumet delivered the slowest revenue growth in the group. Interestingly, the stock is up 2.3% since the results and currently trades at $35.41.

Read our full analysis of Calumet’s results here.

Tenaris (NYSE:TEN)

Operating industrial facilities across the Americas, Europe, Middle East, and Asia, Tenaris (NYSE:TEN) manufactures seamless and welded steel pipes used in oil and gas drilling and transportation.

Tenaris reported revenues of $253 million, up 28.4% year on year. This result topped analysts’ expectations by 17.1%. It was an exceptional quarter as it also recorded a beat of analysts’ EPS and EBITDA estimates.

The stock is down 14.2% since reporting and currently trades at $37.86.

Read our full, actionable report on Tenaris here, it’s free.

Expand Energy (NASDAQ:EXE)

Rebranded from Chesapeake Energy in 2024 after emerging from bankruptcy, Expand Energy (NASDAQ:EXE) produces natural gas, oil, and natural gas liquids from underground shale formations in Louisiana, Pennsylvania, Ohio, and West Virginia.

Expand Energy reported revenues of $4.53 billion, up 41% year on year. This print surpassed analysts’ expectations by 48.2%. Overall, it was an exceptional quarter as it also logged an impressive beat of analysts’ EBITDA and EPS estimates.

Expand Energy delivered the biggest analyst estimate beat among its peers. The stock is down 4.3% since reporting and currently trades at $92.81.

Read our full, actionable report on Expand Energy here, it’s free.

Market Update

Late in 2025 into early 2026, there was hand-wringing around artificial intelligence. For software companies, the fear was that AI would erode pricing power and compress margins as new tools made it easier to replicate what once required expensive enterprise platforms. Crypto investors had their own version of the same anxiety: if AI agents could trade, allocate capital, and manage wallets autonomously, what exactly was the long-term value of today’s crypto infrastructure?

These concerns triggered a noticeable rotation away from these sectors and into safer havens. But markets rarely dwell on one narrative for long. Spring 2026 came, and the focus shifted abruptly from technological disruption to geopolitical risk. The US’ conflict with Iran became the dominant driver of market psychology, and when geopolitics takes center stage, the script changes quickly. Investors stop debating growth rates and start worrying about oil supply, inflation, and global stability.

Want to invest in winners with rock-solid fundamentals? Check out our Top 5 Quality Compounder Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.

/A%20corporate%20sign%20for%20SK%20Hynix%20by%20Tada%20Images%20via%20Adobe%20Stock.jpeg)

/2d%20illustration%20of%20Cloud%20computing%20by%20Blackboard%20via%20Shutterstock.jpg)

/Server%20racks%20by%20dotshock%20via%20Shutterstock.jpg)