/Eli%20Lilly%20%26%20Co_%20by%20Tada%20Images%20via%20Shutterstock.jpg)

With a market capitalization of $1 trillion, Eli Lilly and Company (LLY) is a global pharmaceutical company focused on developing and commercializing medicines across areas such as diabetes, obesity, oncology, immunology, neuroscience, and cardiovascular disease. Founded in 1876 and headquartered in Indianapolis, Indiana, the company is one of the world’s largest drugmakers and is widely recognized for its leadership in diabetes and weight-loss treatments.

Companies worth $200 billion or more are generally classified as “mega-cap stocks,” and Eli Lilly firmly fits that category, with its market capitalization well above this threshold. The company’s massive valuation reflects its strong influence and leadership within the global pharmaceutical industry, particularly in the rapidly expanding diabetes and obesity treatment markets driven by blockbuster drugs such as Mounjaro and Zepbound.

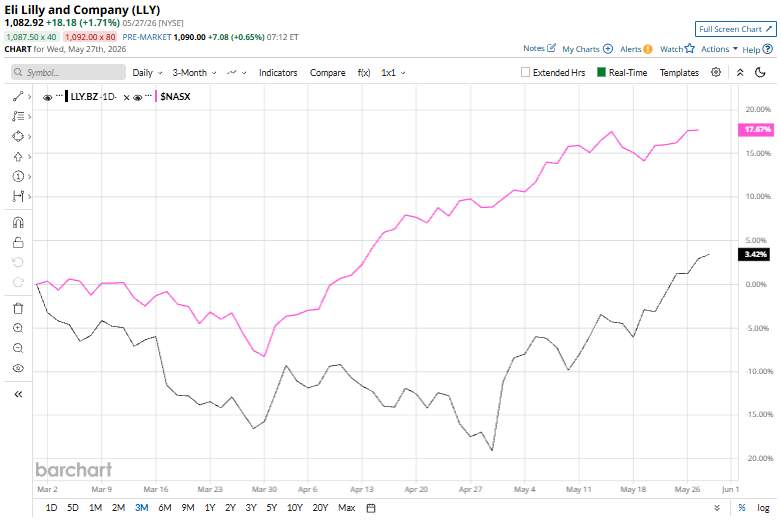

LLY stock is currently trading 4.5% below its 52-week high of $1,133.95, touched in January 2026. Its shares have soared 2.9% over the past three months, underperforming the broader Nasdaq Composite’s ($NASX) 17.7% rise over the same time frame.

On a year-to-date basis, Eli Lilly shares have posted marginal gains, while the broader index advanced 14.8%. Over the past 52 weeks, however, Eli Lilly has significantly outperformed the broader market, with its stock surging 49.3% compared to the benchmark index’s 38.9% gain.

The stock has also regained technical momentum, recently climbing back above its 50-day and 200-day moving averages early this month, signaling improving investor sentiment and strengthening price trends.

Since late April, Eli Lilly stock has surged nearly 25%, driven by continued momentum in its GLP-1 portfolio and strengthening investor confidence in the company’s long-term growth outlook. The rally extended into Tuesday and Wednesday after Lilly announced nearly $4 billion in acquisitions involving three private vaccine developers, further reinforcing bullish sentiment surrounding the stock. The Curevo deal gives Lilly a potential competitor to GSK’s shingles vaccine, Shingrix, with a candidate showing similar effectiveness but fewer side effects. The Vaccine Co. acquisition adds a scalable nanoparticle vaccine platform and an Epstein-Barr virus vaccine candidate, while the LimmaTech buyout strengthens Lilly’s position in antimicrobial resistance through vaccines targeting dangerous bacterial infections.

Eli Lilly’s rival Johnson & Johnson (JNJ) has outpaced LLY, delivering a 50.9% gain over the past 52 weeks and an 11.8% YTD rise.

Nevertheless, among 30 analysts covering the stock, the overall rating stands at a “Strong Buy.” Moreover, the average price target of $1,246.46 signals a premium of 15.1% from the current market prices.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20close-up%20of%20a%20SpaceX%20sign%20by%20Sundry%20Photography%20via%20Adobe%20Stock.jpeg)

/Green%20hydrogen%20by%20Scharfsinn%20via%20Shutterstock.jpg)

/Abbvie%20Inc%20HQ%20photo-by%20vzphotos%20via%20iStock.jpg)