/Factset%20Research%20Systems%20Inc_%20logo%20on%20keyboard-by%20rafapress%20via%20Shutterstock.jpg)

Norwalk, Connecticut-based FactSet Research Systems Inc. (FDS) is a financial data and software company that provides integrated digital platforms and enterprise solutions for investment professionals. Valued at a market cap of $8.4 billion, the company aggregates extensive data from third-party suppliers, news sources, and exchanges into central workstations, providing critical portfolio analytics, risk management, and market intelligence solutions.

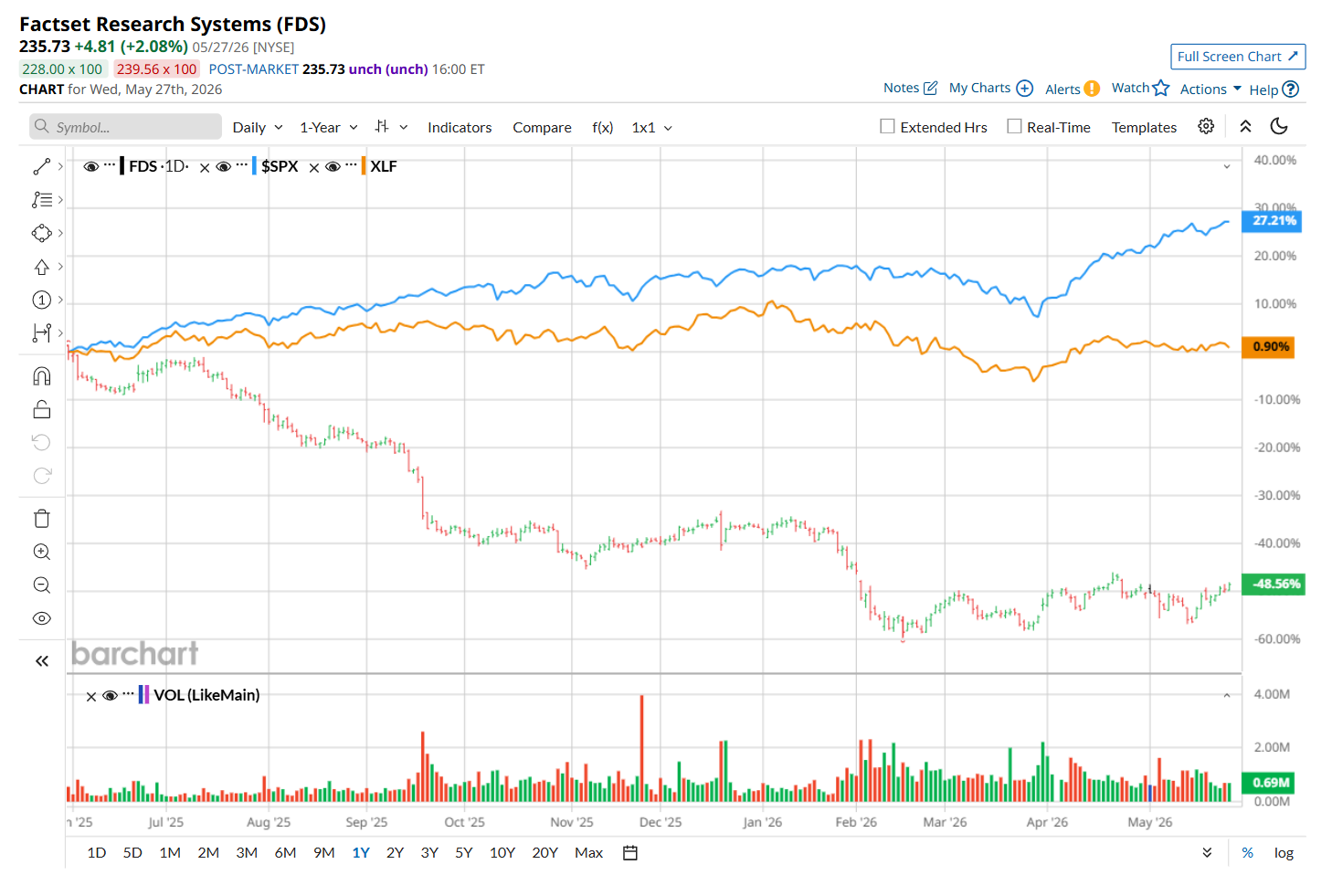

This financial company has notably underperformed the broader market over the past 52 weeks. Shares of FDS have declined 49.1% over this time frame, while the broader S&P 500 Index ($SPX) has soared 26.8%. Moreover, on a YTD basis, the stock is down 18.8%, compared to SPX’s 9.7% rise.

Zooming in further, FDS has also lagged the sector-focused State Street Financial Select Sector SPDR ETF’s (XLF) 1% rise over the past 52 weeks and 6.1% downtick on a YTD basis.

FDS shares surged 6.1% on Mar. 31, after delivering better-than-expected Q2 results. The company posted revenue of $611 million, an increase of 7.1% from the previous year-quarter, surpassing analyst forecasts of $605 million. Earnings also topped estimates, with adjusted EPS coming in at $4.46. Following the solid quarterly performance, management raised its full-year guidance. The company now anticipates fiscal 2026 revenue in the range of $2.45 billion to $2.47 billion and adjusted EPS between $17.25 and $17.75. The upbeat earnings report and improved outlook highlighted continued operational strength and reinforced investor confidence in the business.

For the current fiscal year, ending in August, analysts expect FDS’ EPS to grow 4% year over year to $17.65. The company’s earnings surprise history is mixed. It exceeded the consensus estimates in two of the last four quarters, while missing on two other occasions.

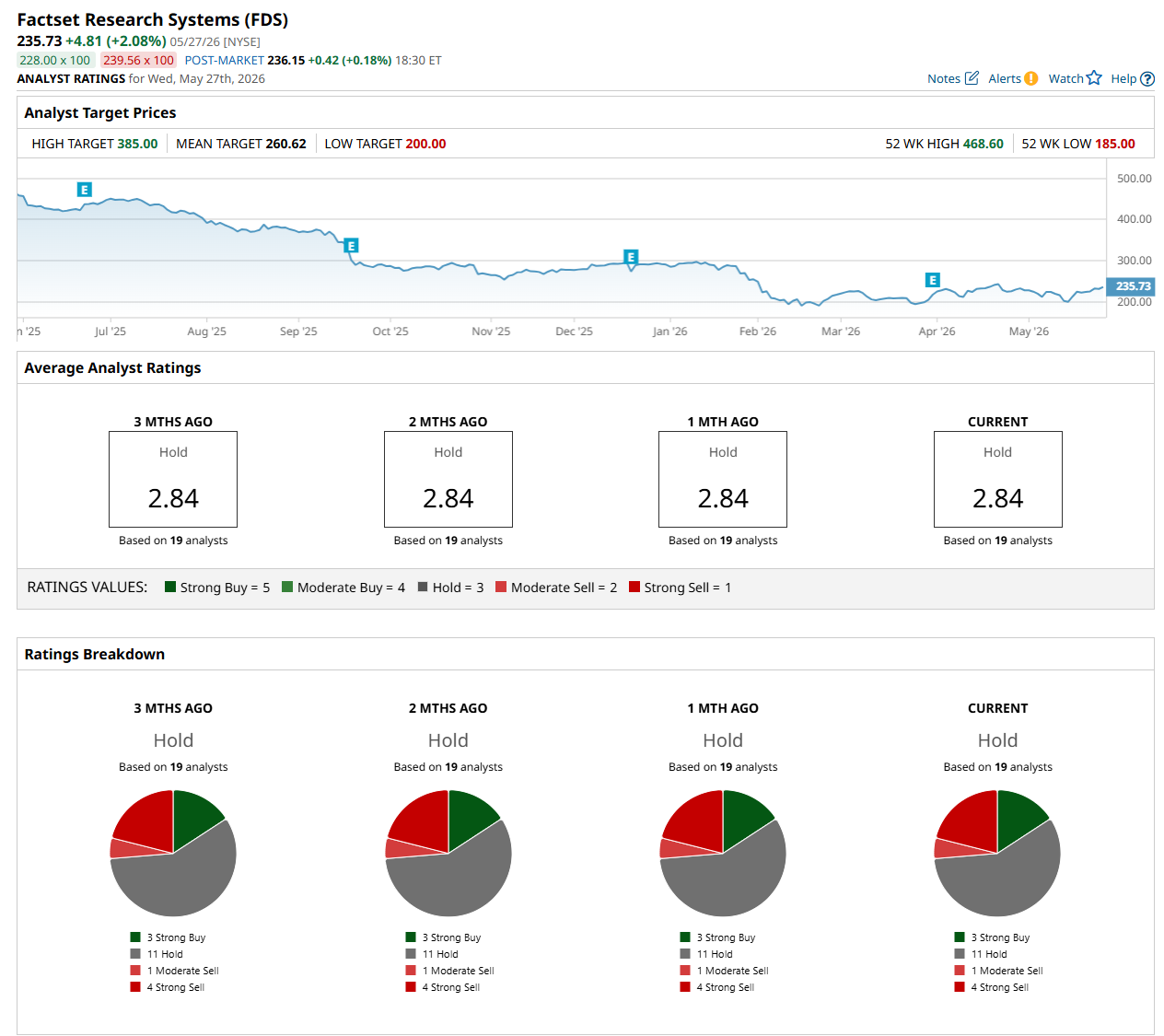

Among the 19 analysts covering the stock, the consensus rating is a "Hold," which is based on three “Strong Buy,” 11 “Hold,” one "Moderate Sell,” and four "Strong Sell” ratings.

The configuration has remained consistent over the past three months.

On May 27, RBC Capital analyst Ashish Sabadra maintained a “Sector Perform" rating on FDS and lowered its price target to $240, indicating a 1.8% potential upside from the current levels.

The mean price target of $260.62 suggests a 10.6% premium to its current price levels, while its Street-high price target of $385 implies a 63.3% potential upside.

On the date of publication, Neharika Jain did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20close-up%20of%20a%20SpaceX%20sign%20by%20Sundry%20Photography%20via%20Adobe%20Stock.jpeg)

/A%20close-up%20of%20the%20SpaceX%20sign%20on%20a%20black%20building%20by%20IanDewarPhotography%20via%20Adobe%20Stock.jpeg)

/NVIDIA%20Corp%20video%20chip-by%20Antonio%20Bordunovi%20via%20iStock.jpg)