/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

Nvidia Corporation (NVDA) has become the face of the artificial intelligence (AI) boom. The Silicon Valley chipmaker evolved from powering video games to driving the world’s biggest AI models, with nearly every tech giant building AI infrastructure now relying on its chips. Its latest fiscal 2027 Q1 results once again showed proof. The company delivered another blockbuster report, with explosive revenue growth and soaring profits as demand for AI chips stayed incredibly strong.

But instead of rallying, the stock slipped after earnings.

The issue is not Nvidia’s present performance, but is Wall Street’s expectations for the future. Investors are now asking how long the chip giant can maintain its dominance as competition starts heating up. The company itself acknowledged that some customers are developing their own custom AI chips for specific workloads. That has sparked concerns over future market share, pricing power, and whether Nvidia’s massive margins can stay untouched as the AI gold rush attracts more rivals.

Still, Bank of America (BAC) believes NVDA remains the top AI compute stock to own despite the recent weakness. The finance titan believes the broader AI infrastructure story is far from slowing down. According to analysts led by Wamsi Mohan, AI spending continues to increase because frontier AI labs are still growing rapidly, AI monetization is improving, token usage is exploding, and tech giants remain under pressure to keep investing aggressively.

The bank also believes this rally is being supported by actual earnings growth rather than pure excitement. And when it comes to the compute side of AI, Bank of America still sees Nvidia sitting firmly at the center of it all. With COMPUTEX around the corner and the AI giant pushing deeper into what it believes could become a $200 billion CPU opportunity, Nvidia's AI story may still be entering its next chapter.

About Nvidia Stock

Founded in 1993 and based in Santa Clara, California, Nvidia has become a pioneer in GPUs and AI-driven computing. From gaming to data centers and automotive tech, its innovations have reshaped industries, powering the AI revolution. Beyond technology, the chip company champions energy-efficient designs and diversity initiatives, combining cutting-edge innovation with responsibility, cementing its role as a cornerstone of modern high-performance computing.

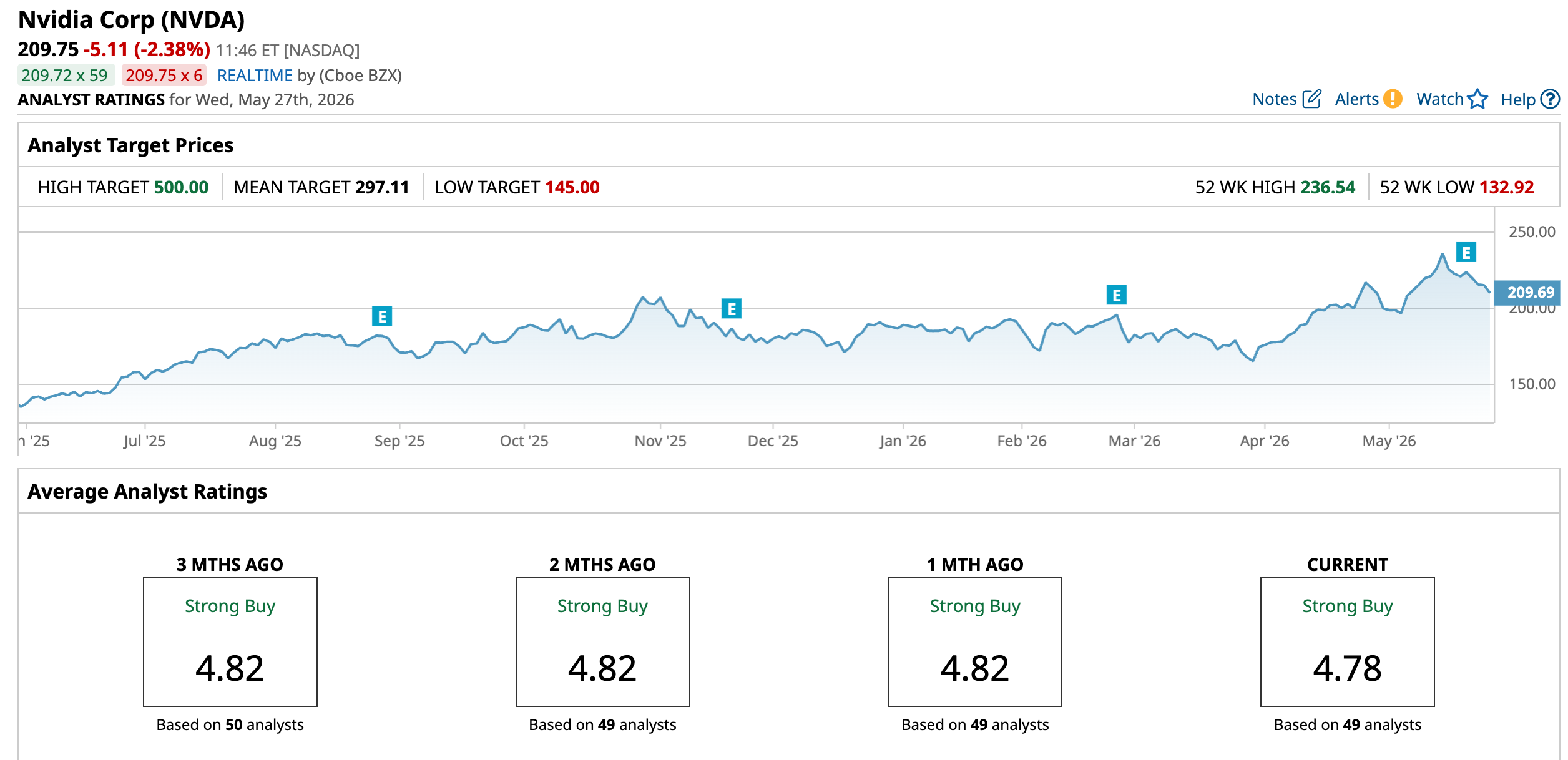

With a massive $5.2 trillion market cap, Nvidia has spent the past year trading like the heartbeat of the entire AI boom. NVDA stock has not moved in a straight line. Rather, it has sprinted higher, paused, shaken out nervous investors, and then taken off again. Over the past 52 weeks alone, NVDA hit fresh record highs 40 different times, showing just how aggressively Wall Street keeps returning to the AI trade. After touching a peak of $236.54 on May 14, the stock cooled off and slipped 11.24%, giving investors another reminder that even market favorites need room to breathe.

Despite the recent dip, NVDA has still delivered impressive gains. The stock is up 54.37% over the past 52 weeks and has a gain of 12.16% year-to-date (YTD), supported by relentless demand for AI chips and another string of blockbuster earnings reports.

Investors are starting to wrestle with bigger questions. Tech giants continue spending billions on AI infrastructure, but Wall Street keeps wondering about the sustainabilty of the pace. There’s also growing chatter around companies building their own in-house AI chips, which could eventually create more competition for Nvidia.

Yet optimism returned this month after reports that CEO Jensen Huang attended a China summit alongside President Trump, fueling hopes that Nvidia may move closer to selling more advanced chips into China again.

Technically, the chart still looks fairly healthy. The 14-day RSI has cooled to 48 after recently entering overbought territory, suggesting some of the recent frenzy has eased. The MACD oscillator continues flashing bullish momentum. The MACD line remains above the signal line, while the histogram is still printing positive bars, usually a sign that buyers still have control, even if the rally has slowed down a bit for now.

Valuation-wise, Nvidia still looks surprisingly reasonable for a company sitting at the center of the AI boom. The stock trades at around 24.2 times forward earnings, below both the sector average and its own historical median. Its price-to-sales ratio of 13.30 times is higher than many chip peers, but still below Nvidia’s five-year average. Investors seem willing to pay that premium because Nvidia’s growth and profit margins remain far ahead of the pack.

Plus, the company is rewarding shareholders along the way. Nvidia recently raised its quarterly dividend by 2,400%, from $0.01 to $0.25 per share, highlighting the company’s massive cash-generating strength.

Nvidia Surges Past Q1 Estimates

Nvidia’s latest fiscal first-quarter 2027 report, released on May 20, showed that the AI boom is still running at full speed. The chip giant once again delivered numbers that comfortably beat Wall Street’s expectations. Revenue surged 85% year-over-year (YOY) to $81.6 billion, while adjusted EPS jumped 140% annually to $1.87.

Nvidia reshaped how it reports its business, organizing operations around two major platforms – Data Center and Edge Computing – to better reflect how AI is being deployed across industries. The biggest growth engine remained Nvidia's data center business, where demand for AI computing systems continues to explode as hyperscalers, enterprises, industrial customers, and even governments race to build AI capabilities.

Data center revenue alone climbed 92% annually to $75.2 billion, helped by strong demand for Nvidia's Blackwell systems and networking products. Within that business, hyperscale revenue soared 115% to $37.9 billion, while the company’s AI Clouds, Industrial and Enterprise (ACIE) segment grew 74% to $37.4 billion. Edge Computing revenue rose 29% YOY to $6.4 billion, supported mainly by workstation demand despite softer consumer PC trends.

Meanwhile, the company’s operating segments showed strength, with Compute & Networking segment remaining the main growth machine, with revenue jumping 88% annually to $74.55 billion. Graphics revenue also rose 58% to $7.07 billion.

And, management made it clear during the earnings call that Nvidia is no longer relying only on Big Tech customers. The company said growth is broadening across AI cloud providers, enterprise deployments, and sovereign AI projects worldwide. Interestingly, Nvidia maintained a cautious stance on China, noting that its outlook does not currently assume any meaningful data center compute revenue contribution from the country.

The company’s balance sheet continues to look incredibly robust. It ended the quarter with $80.6 billion in cash, cash equivalents, and marketable securities, while generating a massive $48.6 billion in free cash flow. That gave Nvidia plenty of room to reward shareholders through dividends and stock buybacks. Nvidia returned $19.3 billion through stock buybacks and $243 million via dividends in Q1.

Looking ahead, Nvidia expects the momentum to continue. The management projects Q2 revenue of nearly $91 billion, plus or minus 2%, pointing to another massive quarter fueled by relentless AI spending. At the midpoint, that would translate to about 12% sequential growth and about 95% YOY growth.

Meanwhile, analysts estimate fiscal Q2 2027 EPS to grow 89.9% YOY to $1.88. For fiscal year 2027, the bottom line is expected to surge 75.9% annually to $8.04 per share, before rising by another 35.32% YOY increase in fiscal 2028 to $10.88 per share.

What Do Analysts Expect for Nvidia Stock?

After Nvidia reported Q1 earnings, the stock dip was less about bad numbers and more about impossible expectations. The company’s massive AI-driven rally has pushed the company into valuation levels rarely seen for chipmakers, meaning investors now expect near-perfect results every quarter. Concerns around China export restrictions, slowing hyperscaler spending, and custom AI chips from companies like Microsoft (MSFT) and Amazon (AMZN) also continue weighing on sentiment. Still, Baird analyst Tristan Gerra believes the market is missing the bigger picture.

The analyst believes the market is still underestimating just how much bigger Nvidia could become beyond its core GPU business. That confidence is why he kept an “Outperform” rating on NVDA while raising the price target to a Street-high $500 from $300. According to Gerra, Nvidia is gaining even more ground in AI inferencing workloads and strengthening ties with hyperscalers and top AI model developers. He expects huge demand for the company’s upcoming Vera Rubin platform, potentially even stronger than what the company saw during the Blackwell launch.

The analyst is especially bullish on the chip giant’s growing CPU ambitions. Gerra believes Vera Rubin could open up a massive new market opportunity thanks to better efficiency and performance than traditional x86 processors. Nvidia itself sees a potential $200 billion market opportunity there, with nearly $20 billion in CPU revenue already visible this year.

Gerra pointed to Nvidia's broader AI ecosystem as a major advantage. From networking products like Spectrum-X and Infiniband to its full-stack AI platform approach, he believes competitors still struggle to match Nvidia's scale and integration. In his view, global AI infrastructure spending is only getting started, leaving Nvidia in one of the strongest positions across the entire AI industry.

Bank of America is also staying firmly bullish on NVDA, lifting its price target to $350 from $320 and maintained a “Buy” rating after what it called another strong earnings beat and guidance raise. BofA noted that Nvidia's shares have dropped after several recent earnings reports, but said investors should ignore the short-term noise and focus on the bigger story – Nvidia’s dominant full-stack AI position in what it sees as the fastest-growing technology market ever.

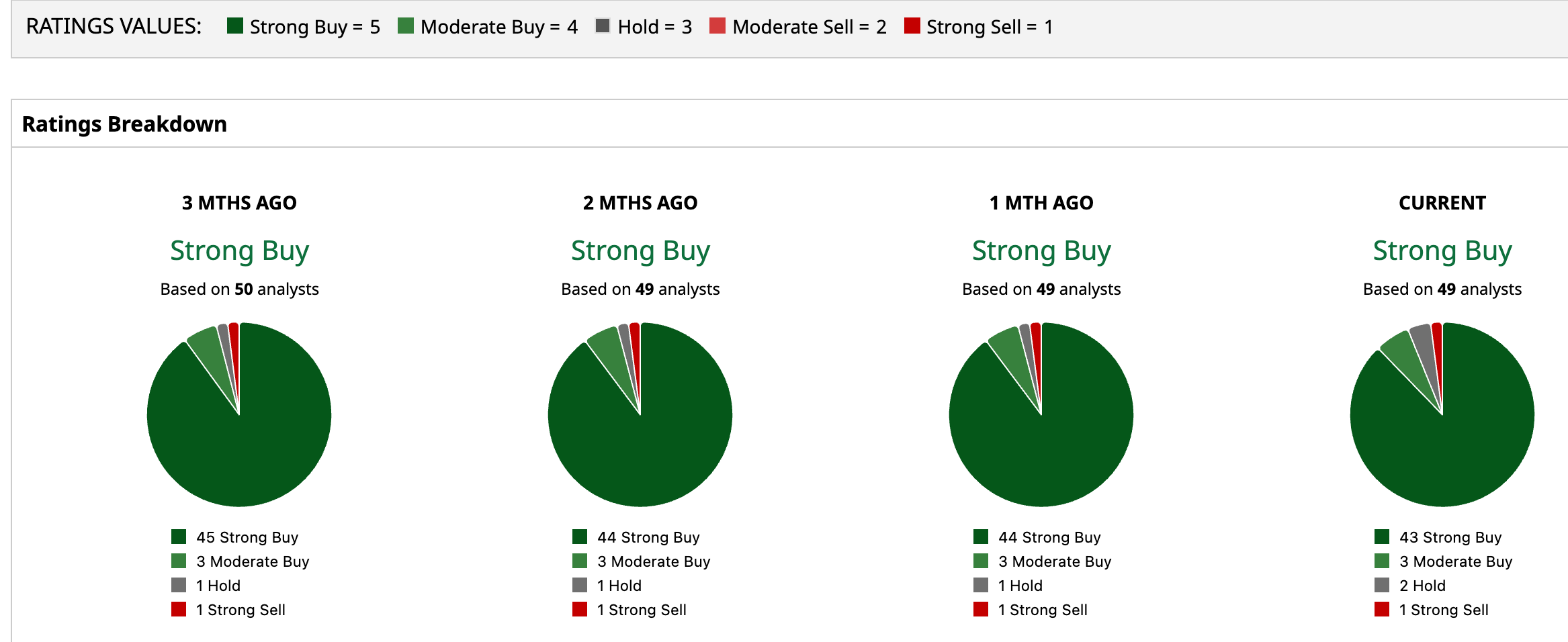

Overall, analysts are optimistic about NVDA’s growth potential, giving the stock a consensus rating of “Strong Buy.” Of the 49 analysts covering the stock, 43 advise a “Strong Buy,” while three suggest “Moderate Buy,” two advise a “Hold,” and only one suggests a “Strong Sell.”

The average analyst price target for NVDA is $297.11, indicating potential upside of 41.65%. The Street-high target price of $500 suggests that the stock could rally as much as 138.38% from here.

On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20close-up%20of%20a%20General%20Motors%20corporate%20sign%20by%20lindaparton%20via%20Adobe%20Stock.jpeg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Zoetis%20sign%20at%20their%20Canadian%20By%20JHVEPhoto.jpeg)

/Microsoft%20headquarters%20By%20Peter.jpeg)

/A%20SoFi%20logo%20on%20an%20office%20building%20by%20Tada%20Images%20via%20Shutterstock.jpg)