Dell Technologies DELL is scheduled to report its first-quarter fiscal 2027 results on May 28, 2026.

For the to-be-reported quarter, revenues are expected to be between $34.7 billion and $35.7 billion, with the mid-point of $35.2 billion suggesting 51% year-over-year growth. Non-GAAP earnings are expected to be $2.90 per share (+/- 10 cents) at the midpoint, indicating 87% growth year over year.

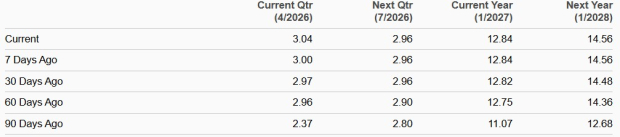

The Zacks Consensus Estimate for fiscal first-quarter revenues is pegged at $35.46 billion, suggesting 51.7% growth from the figure reported in the year-ago quarter. The consensus mark for quarterly earnings is pegged at $3.04 per share, up 2.4% over the past 30 days and suggesting year-over-year growth of 96.1%.

Dell Technologies’ earnings beat the Zacks Consensus Estimate in three of the trailing four quarters, while missing the same in the remaining quarter, with an earnings surprise of 1.22% on average.

Consensus Estimate Trend

Image Source: Zacks Investment Research

Let’s see how things have shaped up for DELL shares prior to this announcement.

Dell Technologies Inc. Price and EPS Surprise

Dell Technologies Inc. price-eps-surprise | Dell Technologies Inc. Quote

Key Factors to Note Ahead of DELL’s Q1

Dell Technologies’ fiscal first-quarter results are expected to benefit from the robust demand for AI-optimized servers, driven by ongoing digital transformation and heightened interest in generative AI applications. In the fourth quarter of fiscal 2026, DELL booked $34.1 billion in AI orders, which reflected accelerating demand as customers deploy AI at scale, a trend expected to have continued in the to-be-reported quarter.

In the fiscal first quarter, Dell Technologies anticipates 53% growth at the midpoint for the combined Infrastructure Solutions Group (ISG) and Client Solutions Group (CSG). While ISG is expected to grow more than 100%, supported by $13 billion of AI server revenue, CSG is expected to be up roughly 2%. DELL is expected to have benefited from an expanding clientele that surpassed 4,000 with growth across neoclouds, sovereigns and enterprise customers, another trend expected to have continued in the fiscal first quarter.

However, the company is facing a challenging macroeconomic environment, along with stiff competition in the PC market from companies like Apple AAPL, HP and Lenovo. Dell Technologies faces challenges from weaker demand for traditional servers and storage in North America, slower federal spending, and declining consumer PC revenue. Supply-chain costs and competitive pressures in the AI market are also expected to have negatively impacted profitability in the to-be-reported quarter.

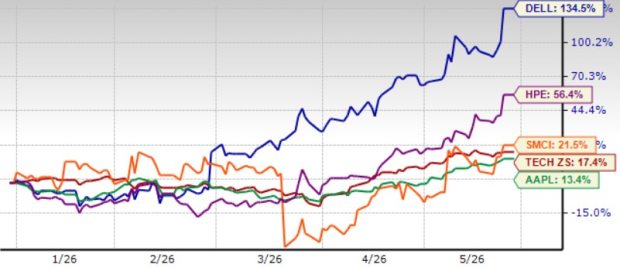

DELL Shares Outperform Sector, Peers

Year to date (YTD), Dell Technologies’ shares have surged 134.5%, outperforming the broader Zacks Computer & Technology sector’s return of 17.4%.

Dell Technologies shares have outperformed its peers, including Apple, Super Micro Computer SMCI and Hewlett-Packard HPE. YTD, Apple, Super Micro Computer and Hewlett-Packard have jumped 13.4%, 21.5% and 56.4%, respectively.

DELL Stock’s Price Performance

Image Source: Zacks Investment Research

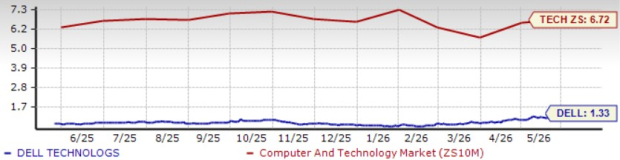

Dell Technologies shares are cheap, as suggested by a Value Score of B.

Dell Technologies’ stock is trading at a significant discount with a forward 12-month P/S of 1.33X compared with the broader sector’s 6.72X.

DELL Stock's Valuation

Image Source: Zacks Investment Research

DELL’s Strong AI Growth Boosts Competitive Prowess

Dell Technologies is benefiting from accelerating AI infrastructure demand. In fiscal 2026, the company recorded more than $64 billion in AI-optimized server orders and shipped above $25 billion worth of AI infrastructure, ending the year with a record backlog of $43 billion.

The company has become a key supplier of AI-optimized servers and data center solutions, benefiting from surging enterprise demand for AI training and inference workloads. Dell Technologies’ partnerships with leading chipmakers such as NVIDIA allow it to deliver high-performance AI systems that enterprises increasingly need to modernize operations and deploy generative AI applications.

The company’s integrated rack-scale systems and data center solutions allow customers to deploy AI clusters efficiently, while managing the total cost of ownership. These capabilities are helping Dell Technologies capture opportunities as organizations scale AI workloads across industries. This is expected to drive top-line growth with AI server revenues to reach $50 billion in fiscal 2027, indicating more than 100% year-over-year growth.

These factors are expected to help DELL steer off competition against the likes of Hewlett Packard Enterprise and Super Micro Computer in the AI infrastructure space.

Conclusion

Dell Technologies’ prospects ride on strong AI infrastructure demand, impressive liquidity position and cheap valuation. An expanding clientele across neoclouds, sovereigns and enterprise customers bodes well for the company’s top-line growth.

DELL currently has a Zacks Rank #2 (Buy) and a Growth Score of A, a favorable combination that offers a strong investment opportunity, per the Zacks Proprietary methodology. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

7 Best Stocks for the Next 30 Days

Just released: Experts distill 7 elite stocks from the current list of 220 Zacks Rank #1 Strong Buys. They deem these tickers "Most Likely for Early Price Pops."

Since 1988, the full list has beaten the market more than 2X over with an average gain of +23.9% per year. So be sure to give these hand picked 7 your immediate attention.

See them now >>This article originally published on Zacks Investment Research (zacks.com).

/Qualcomm%2C%20Inc_%20logo%20on%20phone-by%20viewimage%20via%20Shutterstock.jpg)

/Micron%20Technology%20Inc_billboard-by%20Poetra_RH%20via%20Shutterstock.jpg)

/Abbott%20Laboratories%20vials%20and%20Logo-by%20Melniov%20Dmitriy%20via%20Shutterstock.jpg)