/Arthur%20J_%20Gallagher%20%26%20Co_%20billboard-%20by%20monticello%20via%20Shutterstock.jpg)

Arthur J. Gallagher & Co. (AJG) is a global insurance brokerage, risk management, and consulting services company headquartered in Rolling Meadows, Illinois. With a market cap. of $52.6 billion, the company has grown into one of the world’s largest insurance brokers, serving businesses, institutions, and individuals across more than 130 countries through a combination of owned operations and international partnerships.

Shares of Arthur J. Gallagher have underperformed the broader market over the past 52 weeks. AJG stock has declined 39% over this time frame, while the broader S&P 500 Index ($SPX) has rallied 27.9%. Moreover, shares of the company are down 20.9% on a YTD basis, compared to SPX’s 9.2% gain.

Narrowing the focus, AJG stock has also lagged behind the State Street Financial Select Sector SPDR ETF’s (XLF) 3.4% rise over the past 52 weeks and 5.2% dip in 2026.

On May 20, Arthur J. Gallagher announced that its Risk Placement Services (RPS) division acquired McKee Risk Management, a Pennsylvania-based program administrator specializing in construction, public entity, and property insurance services. The acquisition is expected to strengthen RPS’s underwriting and program administration capabilities, with McKee’s leadership team joining Gallagher’s operations. Investors responded positively to the announcement, sending AJG shares up 1.9% in the following trading session.

For the current year ending in December 2026, analysts expect AJG’s EPS to grow 23.7% year over year to $13.22 on a diluted basis. The company’s earnings surprise history is mixed. It surpassed the consensus estimate in one of the last three quarters while missing on two other occasions.

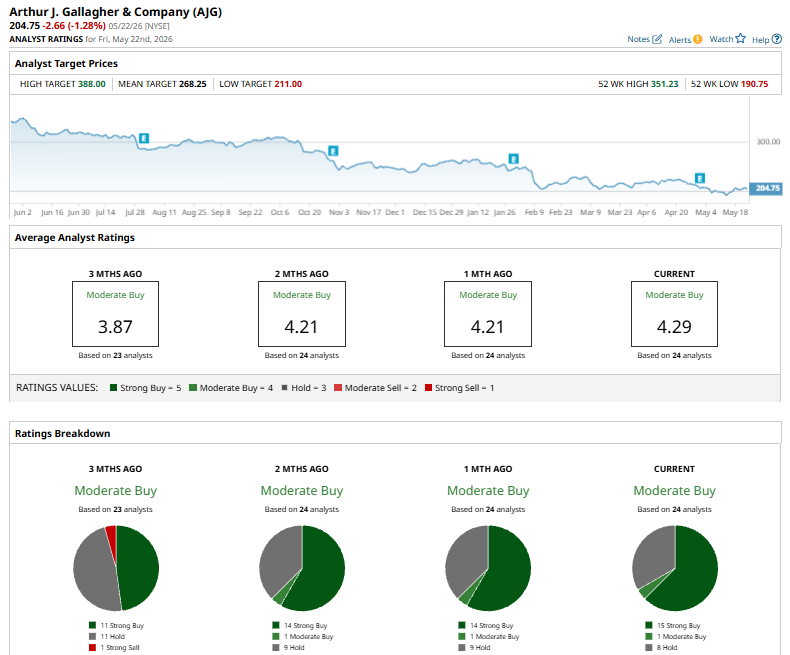

Among the 24 analysts covering AJG stock, the consensus is a “Moderate Buy.” That’s based on 15 “Strong Buy” ratings, one “Moderate Buy,” and eight “Holds.”

The configuration is bullish than a month ago, when the stock had 14 “Strong Buy” suggestions.

On May 6, Morgan Stanley lowered its price target on Arthur J. Gallagher to $265 from $275 while maintaining an “Overweight” rating, following the company’s first-quarter 2026 results and management’s updated outlook. The firm revised its financial model to reflect lower expectations for the adjusted EBITDA margin in Gallagher’s Brokerage segment, based on management commentary regarding the remainder of the year.

The mean price target of $268.25 indicates 31% premium to AJG’s current price levels. Its Street-high target of $388 suggests a 89.5% potential upside.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Space/Rocket%20launching%20into%20space%20by%20BEST%20BACKGROUNDS%20via%20Shutterstock.jpg)

/A%20Palantir%20office%20building%20in%20Tokyo_%20Image%20by%20Hiroshi-Mori-Stock%20via%20Shutterstock_.jpg)

/Close-up%20shot%20of%20Rivian%20R1T_%20Image%20by%20Trong%20Nguyen%20via%20%20Shutterstock_.jpg)