With a market cap of $23.4 billion, Expand Energy Corporation (EXE) is one of the largest independent natural gas producers in the United States. The company is headquartered in Oklahoma City and focuses primarily on the exploration, production, and development of natural gas and related hydrocarbons. It operates across key gas-rich regions such as the Marcellus, Utica, Haynesville, and Bossier shales.

Shares of EXE have notably underperformed the broader market over the past 52 weeks. EXE has dropped 14.4% over this period, while the broader S&P 500 Index ($SPX) has gained 27.9%. Additionally, shares of EXE are down 11.3% on a YTD basis, compared to SPX’s 9.2% rise.

Looking closer, the company has also trailed the S&P 500 Energy Sector SPDR Fund (XLE), which surged 45.6% over the past year and rallied 33.1% in 2026.

On Apr. 28, Expand Energy released its FY2026 Q1 earnings, and its shares popped 4.2% in the next trading session. The company continued to benefit from its scale as the largest U.S. natural gas producer following the Southwestern Energy merger. It reported revenue of approximately $4.40 billion, up 100.2% year over year and significantly above analyst expectations. Adjusted EBITDAX came in near $1.97 billion, while earnings per share of $4.81 also exceeded consensus estimates.

For the fiscal year ending in December 2026, analysts expect EXE’s adjusted EPS to increase 44.3% year-over-year to $8.80. The company's earnings surprise history is mixed. It beat the consensus estimates in three of the past four quarters while missing on another occasion.

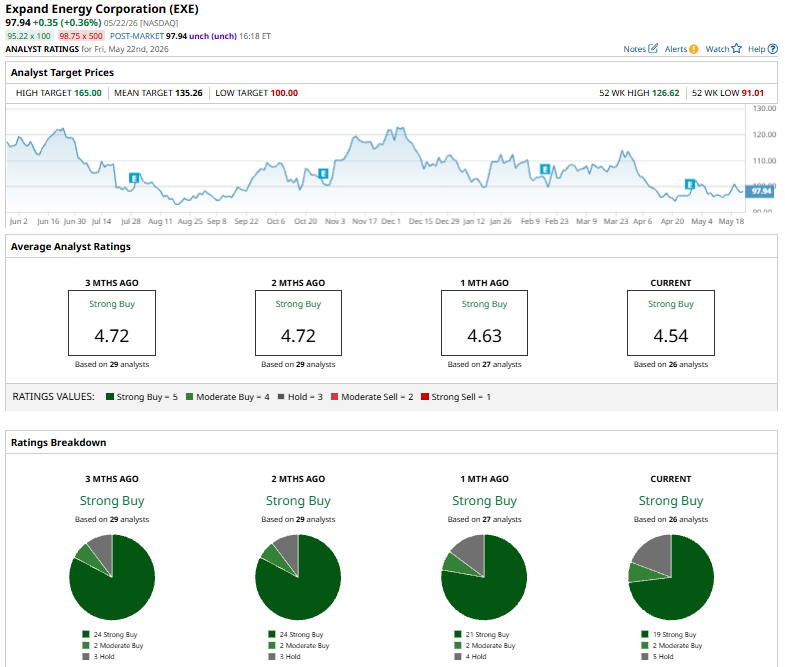

Among the 26 analysts covering the stock, the consensus rating is a “Strong Buy.” That’s based on 19 “Strong Buy” ratings, two “Moderate Buys,” and five “Holds.”

This configuration is more bearish than it was one month ago, with 21 “Strong Buy” suggestions for the stock.

On May 22, Morgan Stanley analyst Devin McDermott reiterated an “Overweight” rating on Expand Energy, while slightly lowering the firm’s price target to $139 from $141.

Expand Energy’s mean price target of $135.26 implies a 38.1% from the current market prices. The Street-high price target of $165 implies a potential upside of 68.5% from the current price levels.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20headquarters%20By%20Peter.jpeg)

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)