For years, enterprise software was one of Wall Street’s safest growth trades, powered by sticky subscriptions, high margins, and the belief that businesses would keep spending on digital transformation no matter the economic backdrop. But now, one of the world’s most influential hedge funds appears to be questioning that narrative.

Bridgewater Associates, founded by Ray Dalio, has exited major positions in several high-profile SaaS names, including Salesforce (CRM), Workday (WDAY), ServiceNow (NOW), and GoDaddy (GDDY), according to its latest 13F filing. At the same time, the fund sharply increased exposure to artificial intelligence (AI) infrastructure and semiconductor plays, signaling a potential shift away from application-layer software and toward the hardware powering the AI boom.

The timing is notable. Across markets, investors are increasingly debating whether generative AI could fundamentally disrupt the traditional SaaS business model by reducing the need for expensive, seat-based enterprise software. Bridgewater’s own CIOs recently warned that AI poses an “existential threat” to parts of the legacy software industry, drawing comparisons to how Amazon (AMZN) reshaped retail decades ago.

What should be your next move?

Stock #1: Salesforce

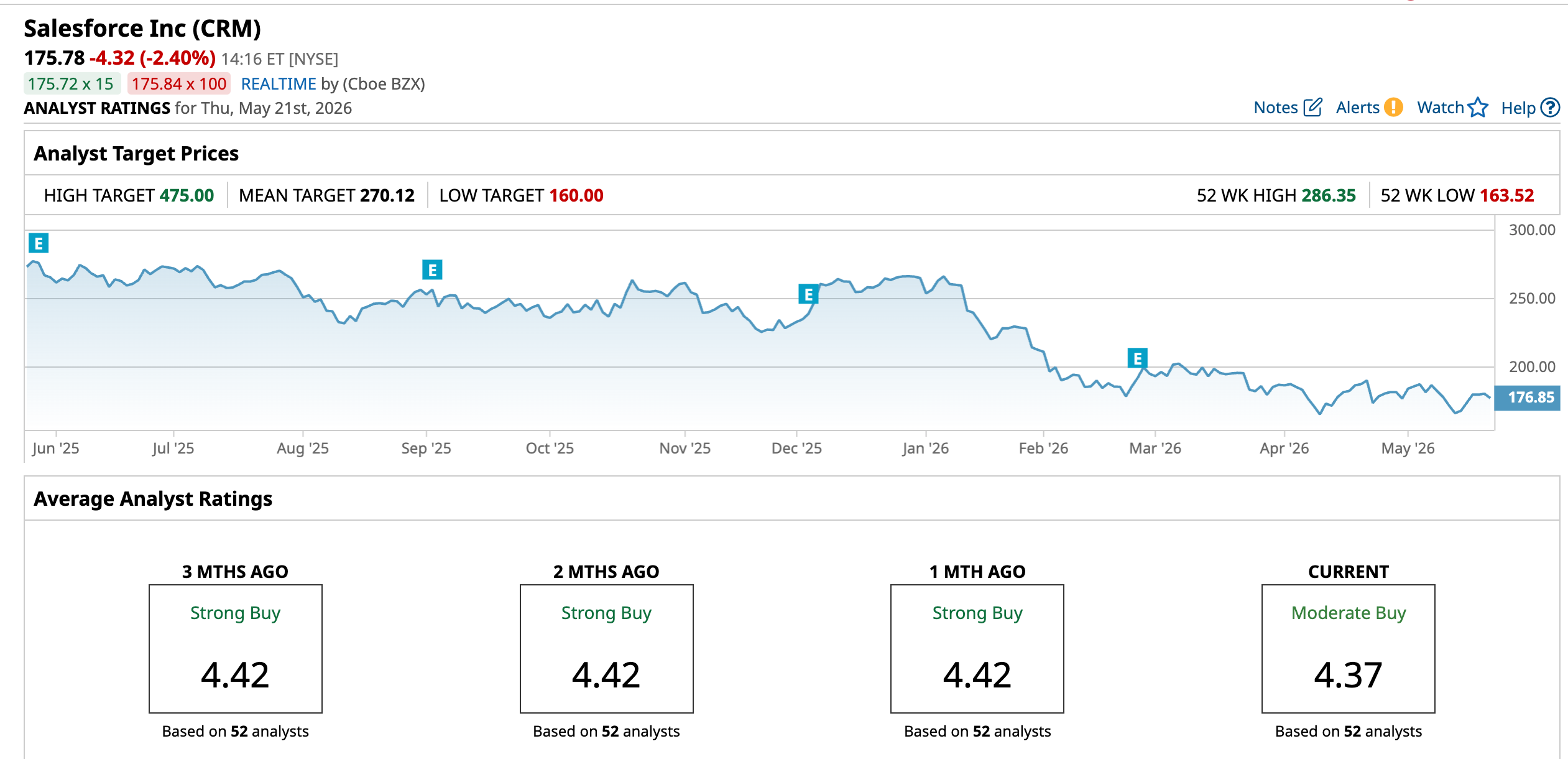

Based in San Francisco, California, Salesforce is a global cloud software giant best known for its customer relationship management (CRM) platform and expanding suite of AI-powered enterprise tools, including Agentforce, Slack, Tableau, and Data Cloud. The company has increasingly positioned itself at the center of the enterprise AI race as businesses adopt automation and agentic workflows across sales, service, and marketing operations. Salesforce currently carries a market cap of $147.36 billion.

CRM stock has struggled amid broader concerns that generative AI could disrupt the traditional SaaS business model. Shares are down 37.66% over the past 12 months and 33.57% year-to-date (YTD), significantly underperforming the broader S&P 500 Index ($SPX), which has gained 27.36% over the past year and 8.74% this year.

In terms of valuation, Salesforce trades at 3.19 times sales, a notable discount to many high-growth software peers as investors debate whether the company can reaccelerate growth through AI monetization and enterprise automation initiatives.

Salesforce reported strong fiscal fourth-quarter 2026 earnings on Feb. 25, with revenue rising 12% year-over-year (YOY) to $11.2 billion. Adjusted earnings per share (EPS) came in at $3.81, higher than the prior-year quarter value of $2.78, also topping analyst estimates. The company highlighted accelerating momentum in its AI business, with Agentforce annual recurring revenue surging 169% YOY to $800 million and total remaining performance obligations at the year’s end, climbing 14% to $72.4 billion.

Management emphasized that Salesforce is evolving into what CEO Marc Benioff calls the “operating system for the Agentic Enterprise,” combining humans, AI agents, apps, and enterprise data on a unified platform. The company also raised its long-term fiscal 2030 revenue target to $63 billion and announced a massive $50 billion share repurchase authorization, signaling confidence in its long-term AI-driven growth strategy despite near-term market skepticism.

Analysts tracking CRM project the company’s profit to reach $9.71 per share in the current fiscal year, up marginally from the prior year.

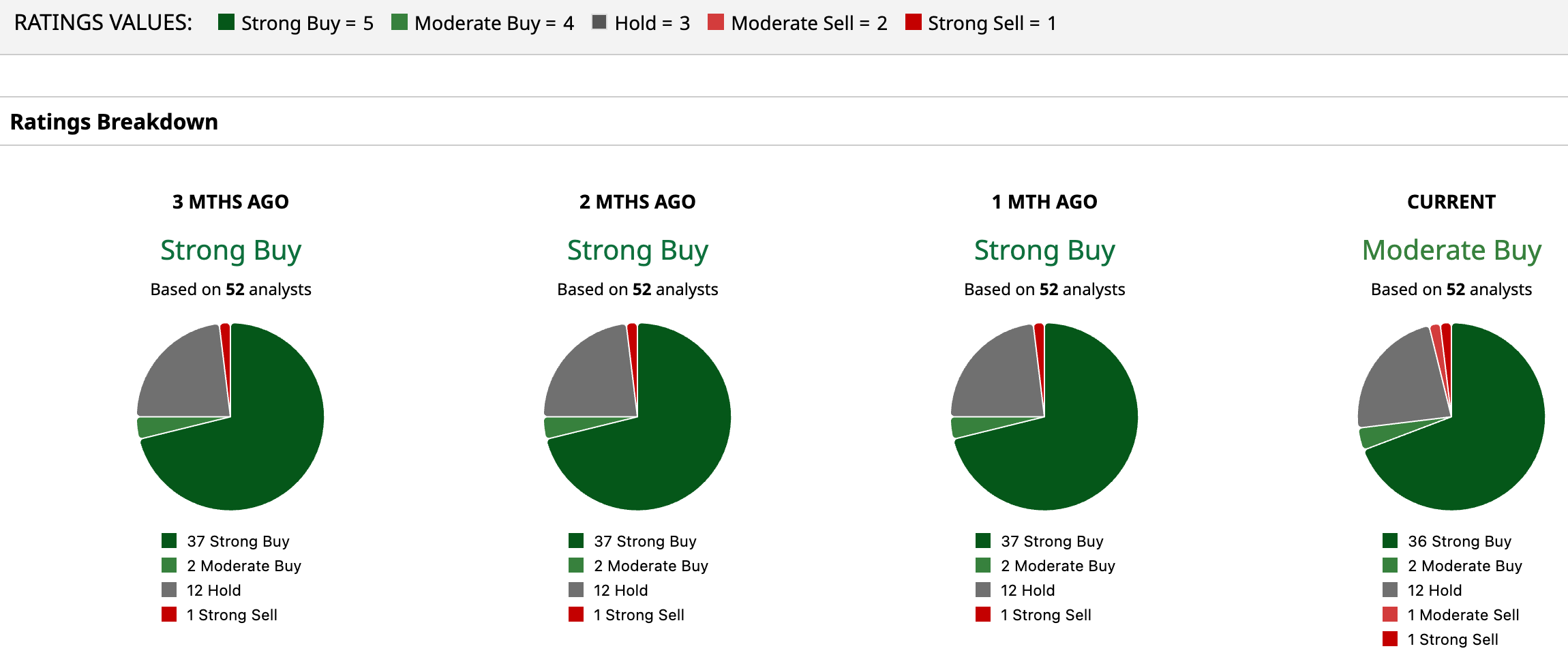

While Bridgewater painted a quite gloomy picture, Wall Street seems to be moderately bullish with a consensus “Moderate Buy” rating overall. Of 52 analysts covering the stock, 36 recommend a “Strong Buy,” two opt for a “Moderate Buy,” 12 suggest a “Hold,” one gives a “Moderate Sell,” and one advises a “Strong Sell.”

The average analyst price target of $270.12 indicates potential upside of 53.7% from the current price levels. The Street-high price target of $475 suggests that CRM could rally as much as 170.2% from here.

Stock #2: Workday

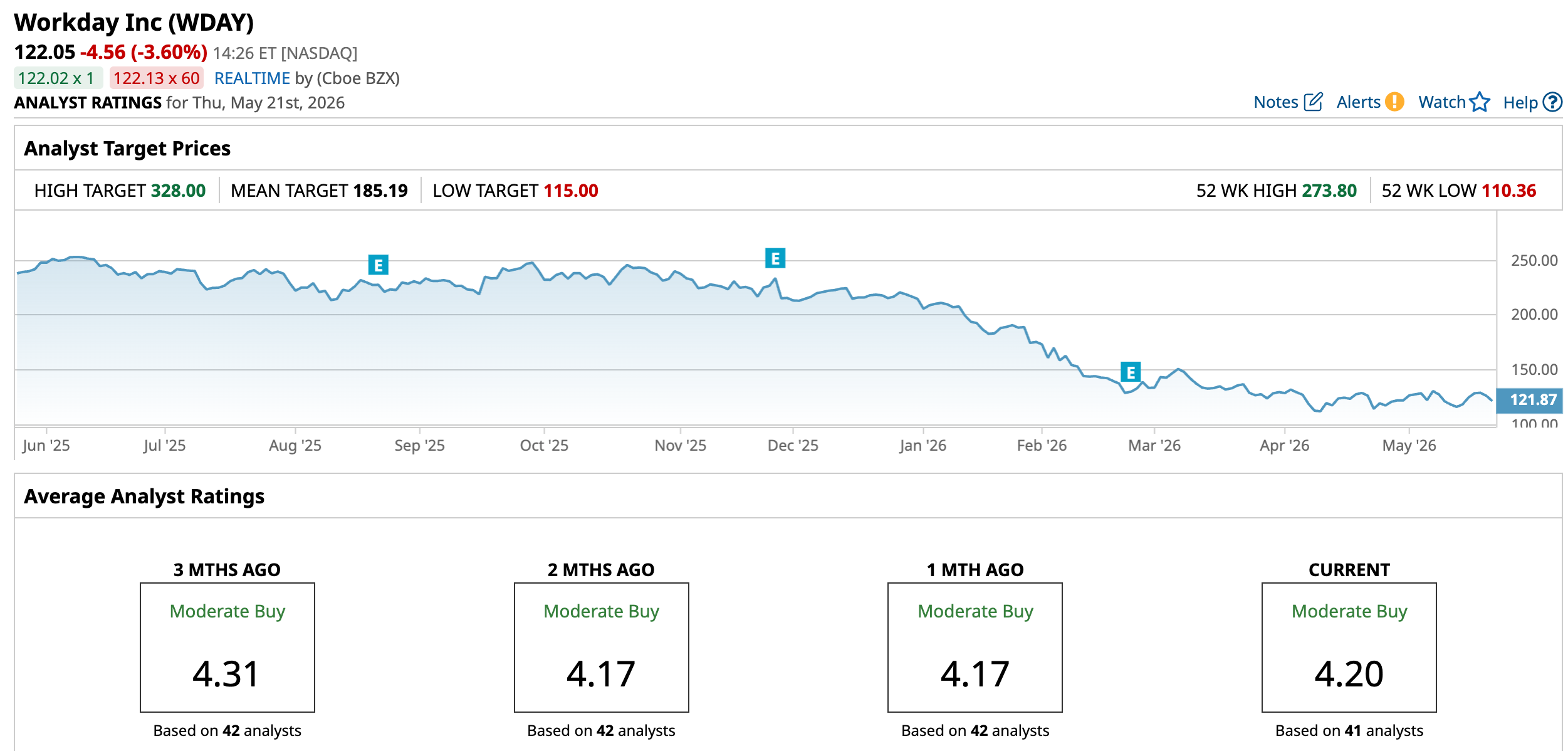

Based in Pleasanton, California, Workday is a leading enterprise cloud software company focused on human capital management (HCM), financial management, payroll, and planning solutions. The company has increasingly positioned itself as an AI-driven enterprise platform, integrating automation and agentic AI capabilities across HR and finance workflows for large organizations worldwide. Workday currently has a market cap of $32.5 billion.

WDAY stock has come under heavy pressure amid broader investor concerns that generative AI could disrupt traditional SaaS business models and reduce long-term seat-based software demand. Shares have plunged 54.92% over the past 52 weeks and are down 43.64% YTD, making Workday one of the weakest performers in the enterprise software sector and lagging behind the broader market.

The stock trades well below its historical software premium as investors weigh rising AI-related competition. It is trading at 25.33 times forward price-to-earnings.

Workday reported strong fiscal fourth-quarter 2026 earnings on Feb. 24, with total revenue rising 14.5% YOY to $2.5 billion, while subscription revenue climbed 15.7% to $2.4 billion. Adjusted EPS came in at $2.47, compared to $1.92 in the same period last year and ahead of Wall Street expectations, as the company continued benefiting from enterprise adoption of its AI-powered HR and finance platform.

Management highlighted accelerating AI momentum, noting that Workday delivered 1.7 billion AI actions across its platform during fiscal 2026 and expanded its ecosystem through new AI integrations, developer tools, and the acquisition of integration platform Pipedream. The company also emphasized growing adoption among large enterprises, with more than 11,500 global customers now using Workday products.

Moreover, Workday issued fiscal 2027 subscription revenue guidance of $9.93 billion to $9.95 billion.

On the other hand, fiscal 2027 profit is expected to be $5.11 per share according to the consensus, up 10.9% YOY, and rise another 31.1% to $6.70 per share in fiscal 2028.

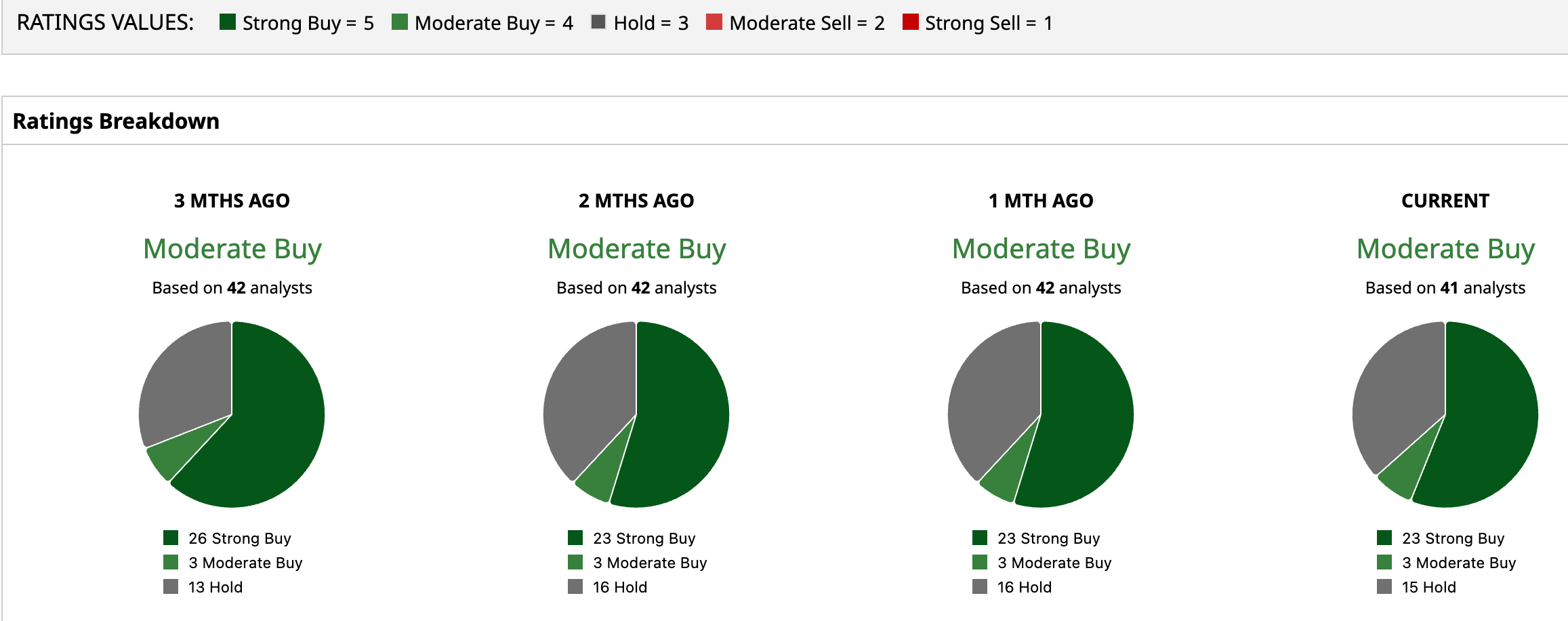

The stock has a consensus “Moderate Buy” rating overall. Of 41 analysts covering the stock, 23 recommend a “Strong Buy,” three advise for a “Moderate Buy,” and the remaining 15 suggest a “Hold.”

The average analyst price target of $185.19 indicates potential upside of 51.7% from the current price levels, while the Street-high price target of $328 suggests that the stock could rally as much as 168.7% from here.

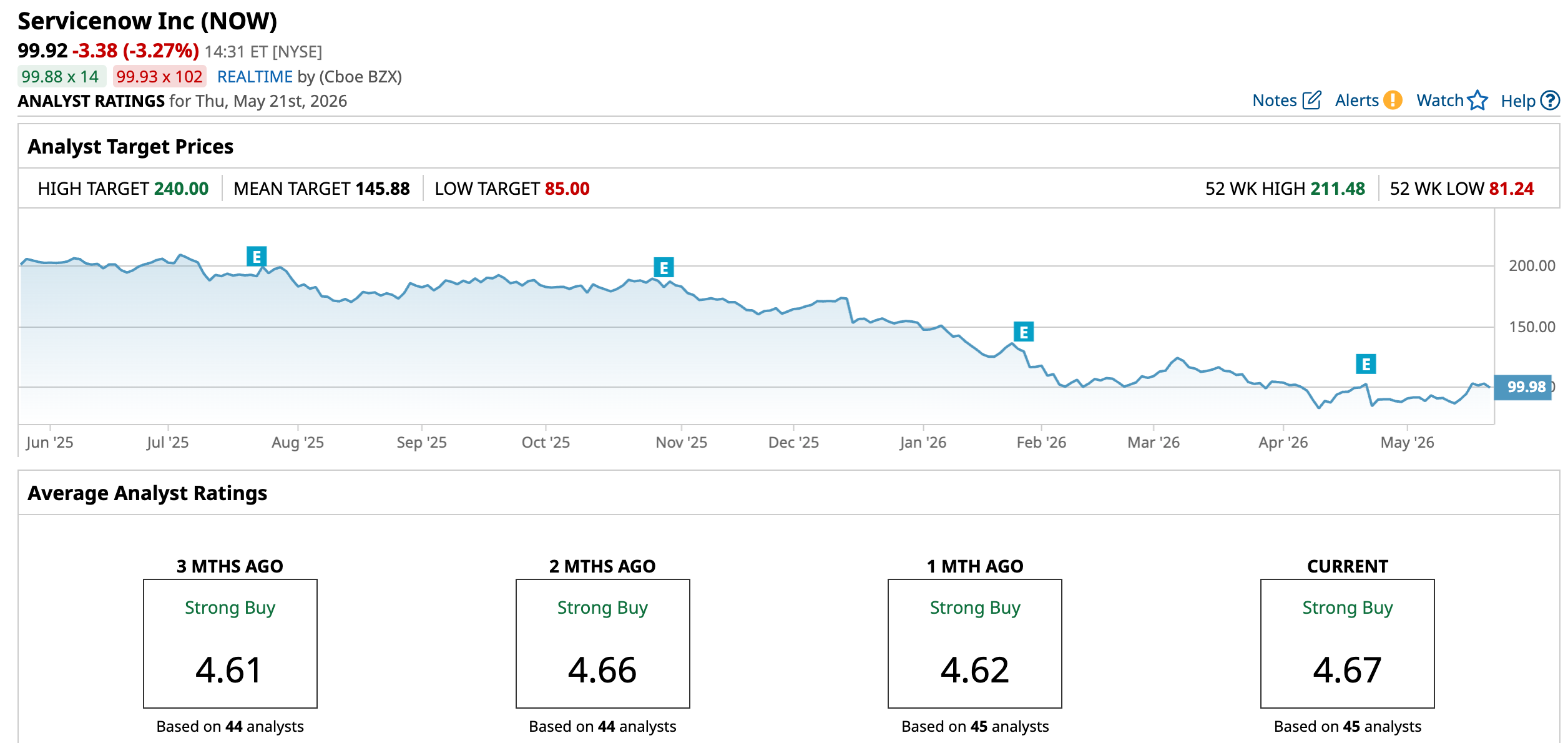

Stock #3: ServiceNow

ServiceNow is a leading enterprise software company that provides a cloud-based platform for automating and managing digital workflows across IT service management, customer service, HR, security, and other business functions. The company is headquartered in Santa Clara, California and has a market cap of $106.5 billion, reflecting its position as one of the most valuable enterprise software providers globally with strong recurring revenue and broad adoption among large organizations.

Shares of ServiceNow have experienced a dramatic fall over the past year, reflecting Wall Street’s anxiety around AI disruption. The stock remains deeply below its prior highs, with shares down 50.74% over the past 52 weeks and 34.74% YTD, underperforming the broader market.

The stock is currently trading at 43.26 times forward price-to-earnings, which is higher than the sector median but below its own historical average.

ServiceNow reported first-quarter 2026 earnings on April 22. For Q1 2026, subscription revenue increased 22% YOY to $3.7 billion, while total revenue also rose 22% to $3.8 billion.

Current remaining performance obligations (cRPO), a key forward-looking indicator of contracted revenue expected over the next 12 months, climbed 22.5% YOY to $12.6 billion. Remaining performance obligations (RPO) increased 25% YOY to $27.7 billion, reflecting continued strong enterprise spending commitments on the platform.

Moreover, non-GAAP operating margin expanded to 32%, while non-GAAP subscription gross margin was 81.5%. Non-GAAP net income rose to $1 billion, and non-GAAP EPS increased to $0.97 from $0.81 in the prior-year quarter.

Meanwhile, ServiceNow’s Q2 2026 guidance called for subscription revenue of $3.815 billion to $3.820 billion, representing 22.5% YOY growth, alongside projected cRPO growth of 19%.

Analysts covering NOW project the company’s EPS to rise 19.9% YOY to $2.35 in fiscal 2026 and grow 28.5% to $3.02 in fiscal 2027.

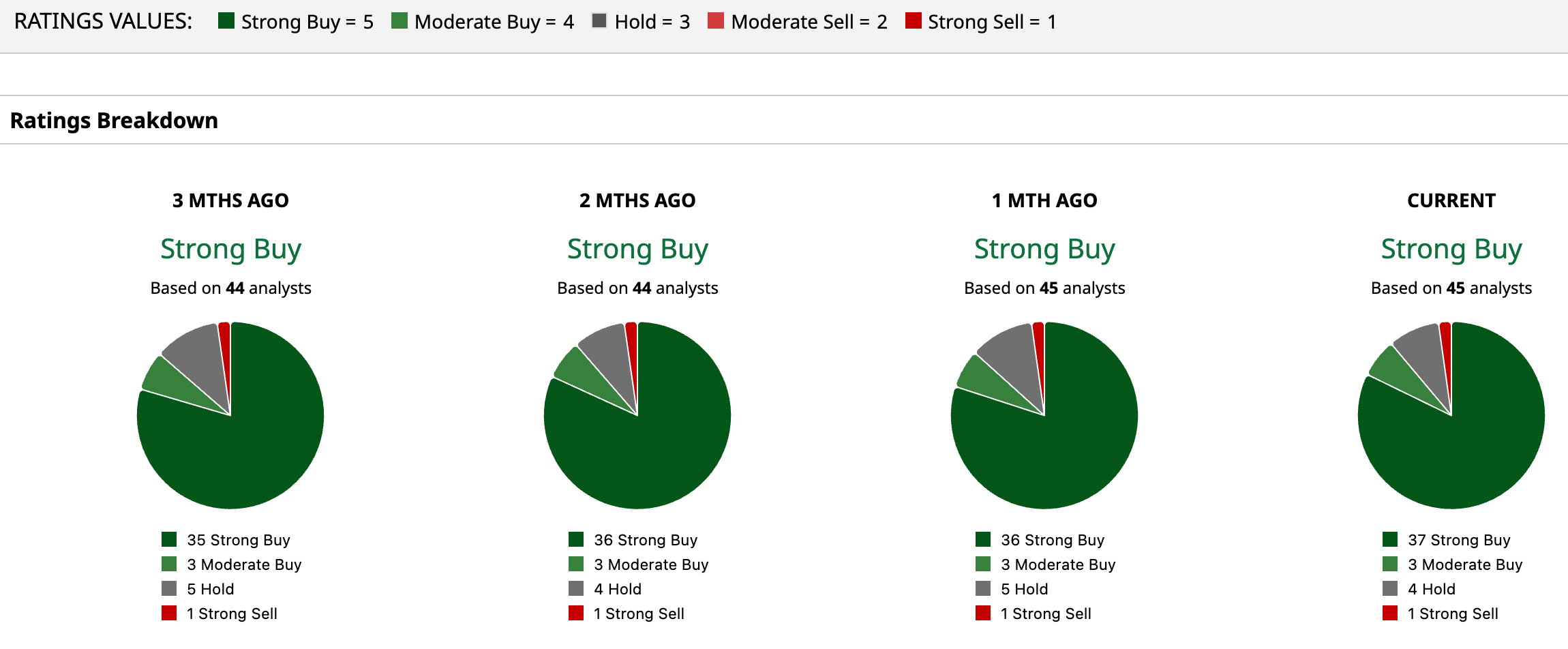

NOW has a consensus rating of a “Strong Buy” overall, showing analysts’ confidence despite the changing industry dynamics. Of the 45 analysts covering the stock, 37 advise a “Strong Buy,” three suggest a “Moderate Buy,” four analysts give it a “Hold” rating and one “Strong Sell.”

While NOW’s average price target of $145.88 suggests an upside of 46%, the Street-high target of $240 signals that the stock could rise as much as 140.2% from current levels.

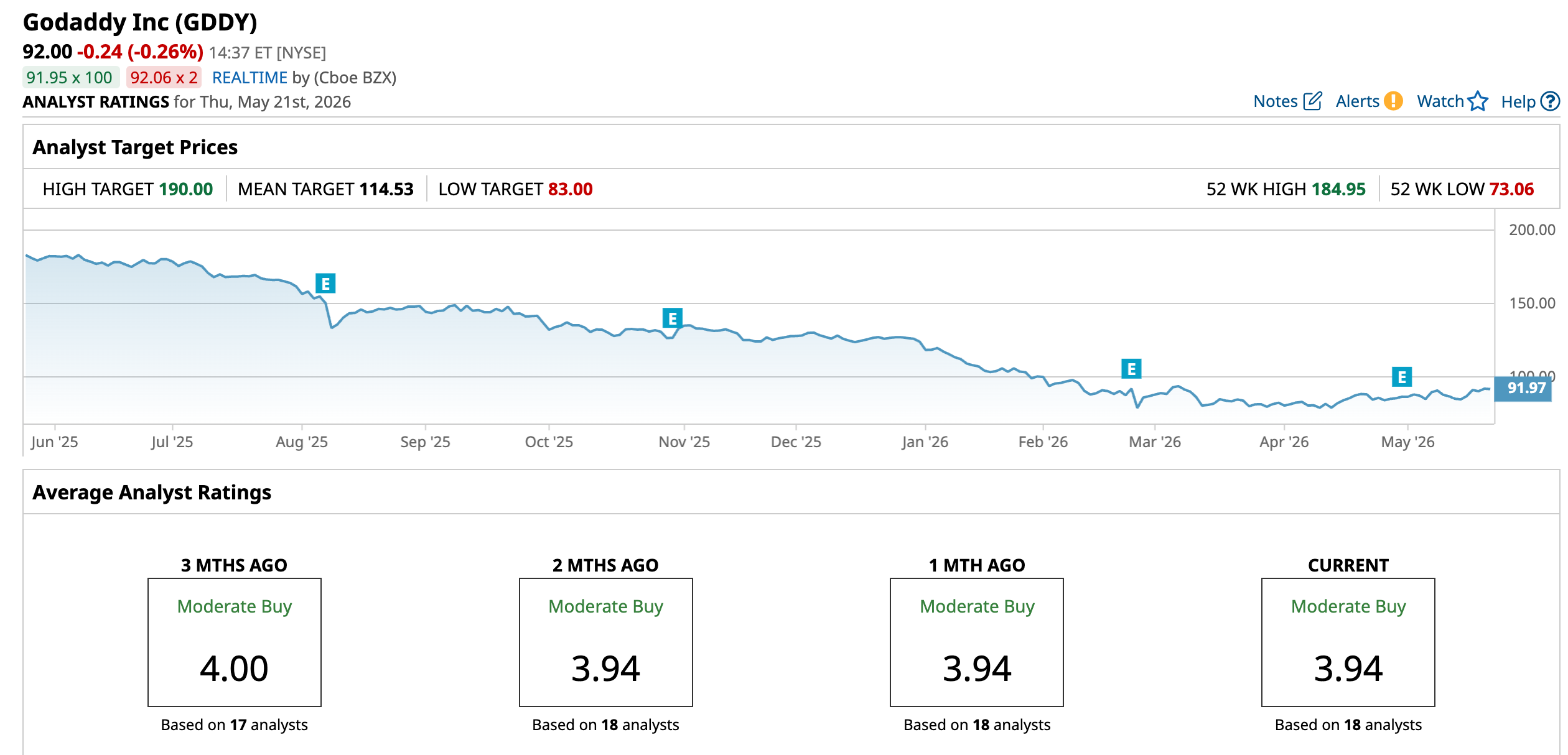

Stock #4: GoDaddy

Based in Tempe, Arizona, GoDaddy is a leading internet infrastructure and digital services company best known for its domain registration, website hosting, e-commerce, and online marketing solutions tailored for small businesses and entrepreneurs. The company has increasingly expanded its AI-powered offerings through its Airo platform, helping customers build websites, manage digital storefronts, and automate online business operations. GoDaddy currently has a market cap of $12.2 billion.

GDDY stock has faced significant pressure over the past year as investors questioned the durability of small-business spending and the company’s long-term growth outlook. Shares have declined 49.8% over the past 52 weeks and are down 25.76% YTD, sharply underperforming the broader market.

In terms of valuation, the stock trades at 12.62 times forward price-to-earnings and 2.33 times sales, representing a notable discount to many software peers.

GoDaddy reported solid first-quarter 2026 earnings on April 30, with revenue rising 6% YOY to $1.3 billion. Its EPS came in at $1.60, beating analyst estimates and improving from $1.51 in the prior-year quarter.

The company is seeing accelerating momentum in its Applications and Commerce segment, where revenue grew 12% YOY and accounts for a significant portion of the business. Also, GDDY pointed to early traction for its AI-powered Airo platform, which reportedly scaled to a multi-million dollar annualized bookings run rate within weeks of launch. Free cash flow increased 15% to $473.6 million.

Investor sentiment has remained cautious amid concerns that AI-native competitors could intensify pressure on GoDaddy’s core website and hosting business. Analysts continue to monitor whether the company’s AI initiatives can meaningfully reaccelerate bookings growth over the next several quarters.

For the full year ending Dec. 31, 2026, GoDaddy expects revenue within a range of $5.195 billion to $5.275 billion and free cash flow of around $1.8 billion.

Meanwhile, the consensus EPS estimate of $7.17 for 2026 indicates a rise of 20.1% YOY, and $8.92 for 2027, which reflects a growth of 24.4%.

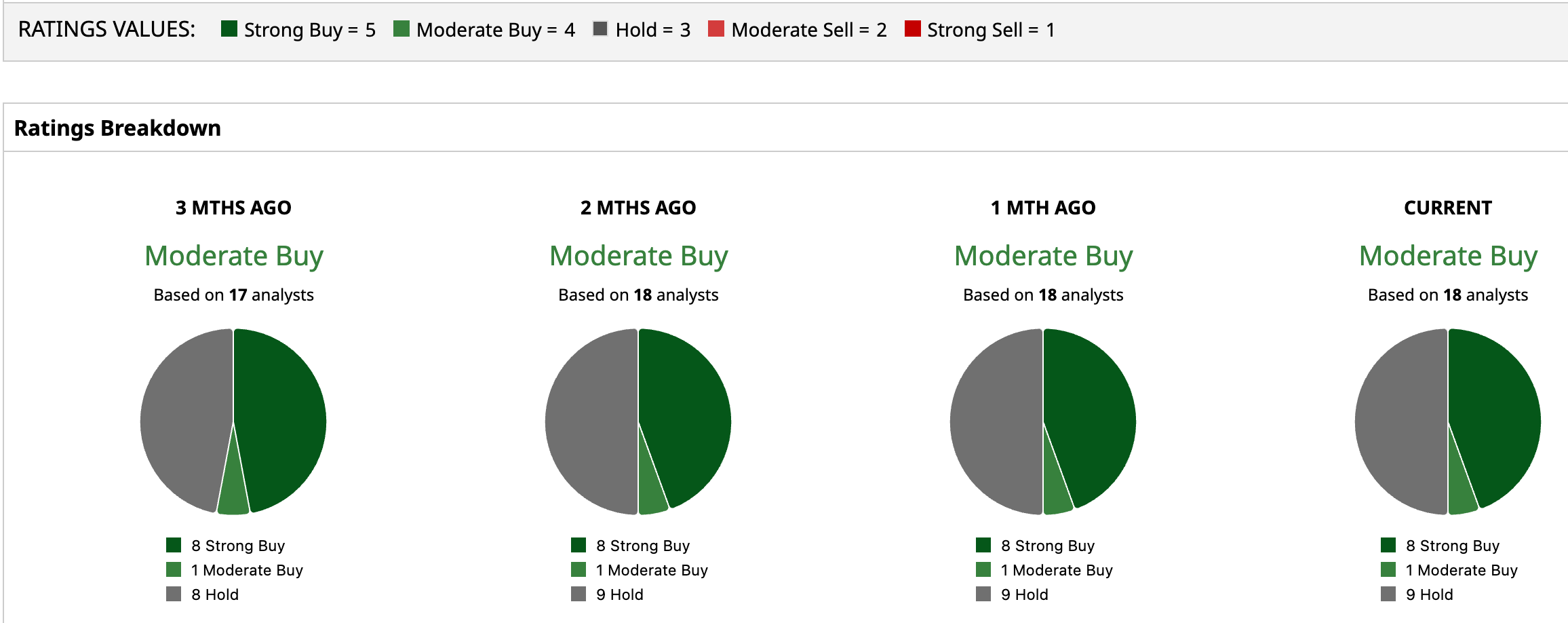

The stock has a consensus “Moderate Buy” rating overall. Of 18 analysts covering the stock, eight recommend a “Strong Buy,” one advises a “Moderate Buy,” and the remaining nine suggest a “Hold.”

Its average analyst price target is $114.53, which indicates potential upside of 24.5% and the Street-high price target of $190 suggests 106.5% upside from here.

On the date of publication, Subhasree Kar did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20photo%20of%20a%20Sandisk%20Solid%20State%20Drive%20by%20Top%20Popular%20Vector%20by%20Shutterstock.jpg)

/Abbott%20Laboratories%20vials%20and%20Logo-by%20Melniov%20Dmitriy%20via%20Shutterstock.jpg)

/Intuit%20Inc%20logo-by%20Mojahid%20Mottakin%20via%20Shutterstock.jpg)