/Fedex%20Corp%20delivery%20truck-by%20Sundry%20Photography%20via%20iStock.jpg)

Memphis, Tennessee-based FedEx Corporation (FDX) is one of the world’s largest transportation, logistics, and delivery services companies. With a market cap of $92.3 billion, it offers global shipping, e-commerce, freight, and supply chain solutions to businesses and consumers through FedEx Express and FedEx Freight segments.

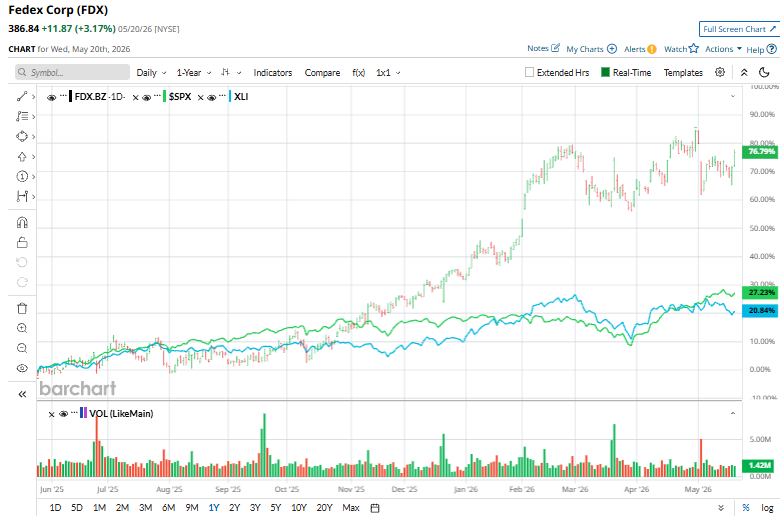

FedEx has outperformed the broader market over the past year. FDX stock prices have soared 74.9% over the past 52 weeks and 33.9% on a YTD basis, compared to the S&P 500 Index’s ($SPX) 25.1% gains over the past year and 8.6% return in 2026.

Narrowing the focus, FedEx has also outpaced the sector-focused State Street Industrial Select Sector SPDR Fund’s (XLI) 18.8% surge over the past 52 weeks and 10.1% YTD uptick .

On May 13, FedEx announced that its Board of Directors approved the previously announced separation of its FedEx Freight business. As part of the transaction, the board declared a pro rata dividend representing 80.1% of the outstanding shares of FedEx Freight Holding Company, Inc. to FedEx shareholders of record as of May 15, 2026.

Following the separation, FedEx Freight is expected to begin trading independently on the New York Stock Exchange under the ticker symbol “FDXF” starting June 1, 2026. Management said the move is intended to position both FedEx and FedEx Freight as standalone companies better equipped to strengthen their respective market leadership positions and drive long-term shareholder value. Under the distribution terms, FedEx shareholders will receive one share of FedEx Freight common stock for every two shares of FedEx common stock held on the record date, with cash payments issued in lieu of fractional shares.

Following the announcement, FedEx shares initially slipped 1.8% as investors assessed the implications of the separation. However, the stock rebounded in the following trading session, climbing 2.8% amid optimism surrounding the potential operational focus and value creation opportunities from the spin-off.

For fiscal 2026, ending in May, analysts expect FDX to deliver an adjusted EPS of $19.72, up 8.4% year over year. The company has a stellar earnings surprise history. It has surpassed the Street’s bottom-line estimates in each of the past four quarters.

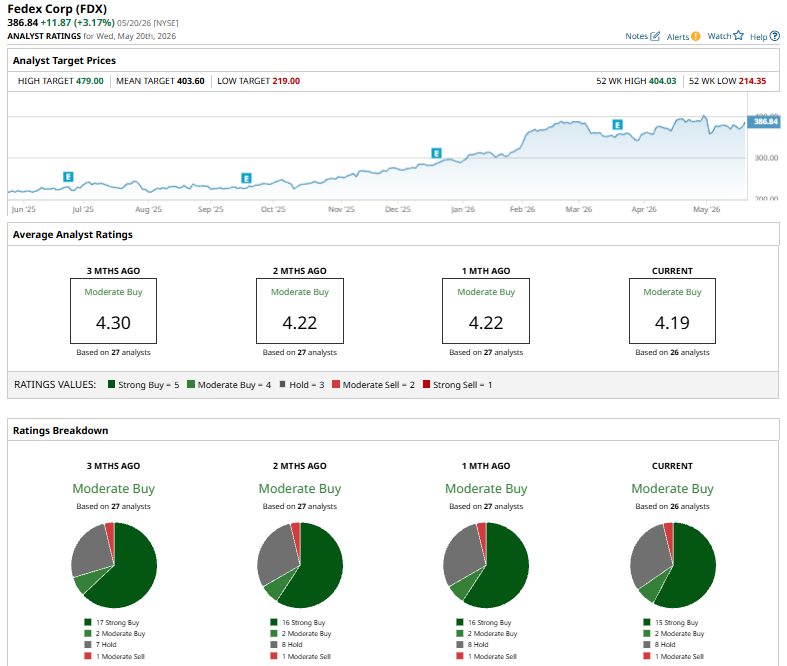

Among the 26 analysts covering the FDX stock, the consensus rating is a “Moderate Buy.” That’s based on 15 “Strong Buys,” two “Moderate Buys,” eight “Holds,” and one “Moderate Sell.”

This configuration is less optimistic than it was a month ago, when 16 analysts issued “Strong Buy” recommendations.

On Apr. 6, Argus raised its price target on FedEx to $400 from $350 while maintaining a “Buy” rating on the stock. The firm cited continued progress in FedEx’s transformation and cost-efficiency initiatives, which helped drive margin expansion in the FedEx segment through the first nine months of fiscal 2026 despite a softer demand environment.

Argus also noted that the company has been gaining market share in both the U.S. and Europe, supported by stronger pricing for premium services and improved operational efficiencies resulting from the ongoing consolidation of FedEx’s business operations.

FedEx’s mean price target of $403.60 represents a 4.3% premium to current price levels. Meanwhile, the Street-high target of $479 suggests a notable 23.8% upside potential.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/An%20aerial%20view%20of%20a%20data%20center%20cooling%20system%20by%20Sepia100%20via%20Adobe%20Stock.jpeg)