/Berkshire%20Hathaway%20Inc_%20logo%20on%20phone-by%20FelloeNeko%20via%20Shutterstock.jpg)

Berkshire Hathaway’s (BRK.A) (BRK.B) popular investment portfolio is undergoing some mammoth changes. The conglomerate filed its 13F report to the Securities and Exchange Commission for the period ending March 31, 2026 – making it the first report under the tenure of CEO Greg Abel, who succeeded Berkshire’s longtime leader Warren Buffett.

And if anyone thought that Abel would slowly ease into the job, they were sorely mistaken. Rather than dipping his toe into the water, this was the investing equivalent of a cannonball.

Abel’s Berkshire opened new positions in Macy’s (M) and Delta Air Lines (DAL) — two interesting picks considering the challenges facing brick-and-mortar retailers and airlines right now. He bought more than 3.5 million shares of Alphabet (GOOG) (GOOGL) stock, making that the company’s fifth-largest holding. And he tripled the company’s stake in New York Times Company (NYT), buying about 10 million shares. Berkshire now owns 9.3% of the entire company.

He dramatically lowered the company’s exposure in Chevron (CVX), selling 35% of the company’s shares; and in Constellation Brands (STZ), selling 95% of STZ stock.

And Abel completely exited stakes in more than a dozen companies, including some longtime Buffett holdings. At least some of those, according to the Wall Street Journal, were stocks managed by former Berkshire manager Todd Combs, who now is working at JPMorgan (JPM).

Here are five major companies that Berkshire Hathaway sold. Should you do the same?

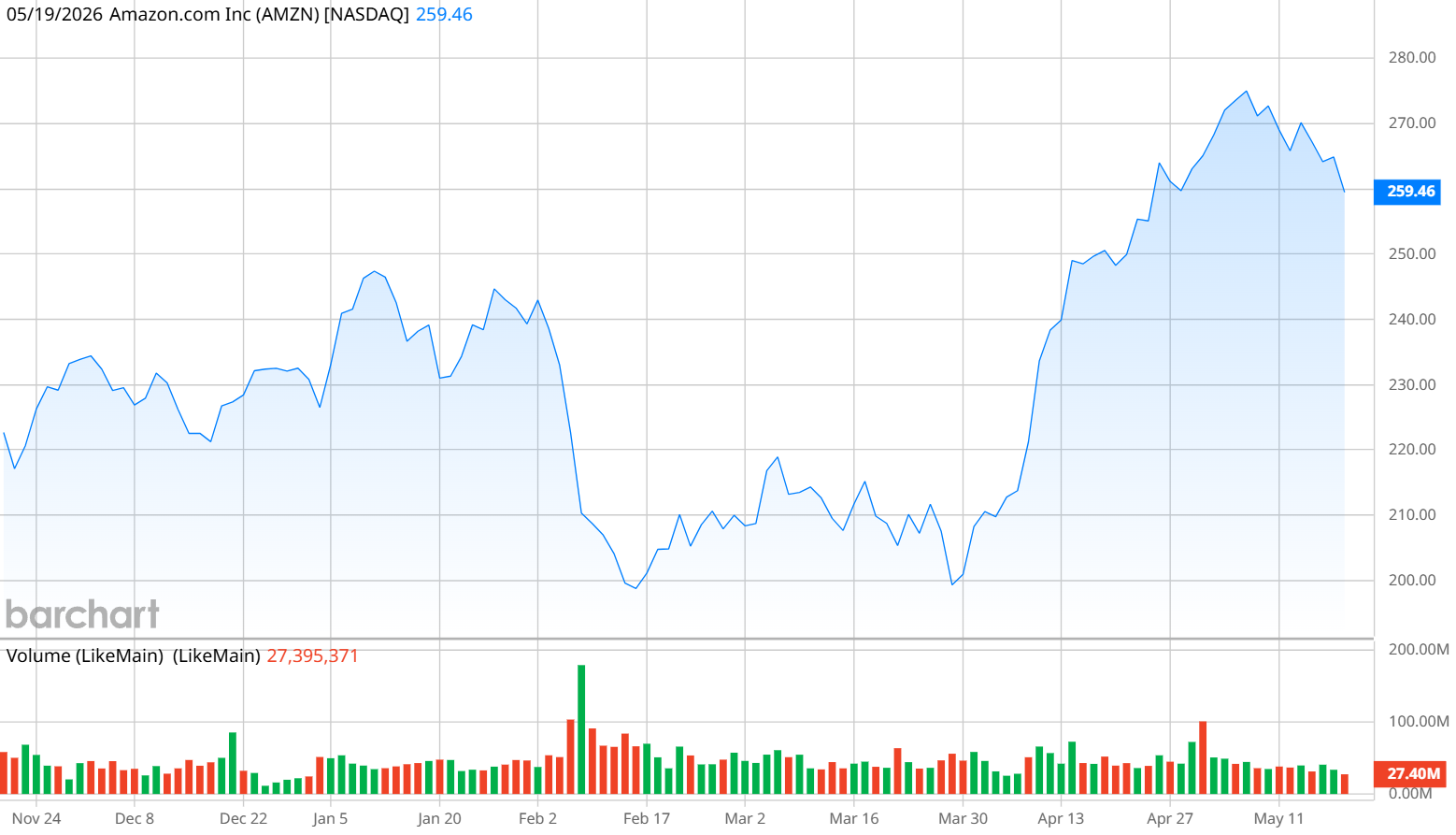

Amazon

Amazon (AMZN) is one of the biggest companies in the world by market capitalization, and a member of the Magnificent Seven grouping of stocks dominating the S&P 500. The company has a mammoth retail business that generated more than $180 billion in the first quarter. And its Amazon Web Services has the biggest market share in the cloud computing space (28%), giving Amazon another $37.6 billion in Q1 revenue.

Shares are up 28% in the last 12 months, roughly mirroring the return of the S&P 500, and have come on lately as Amazon reported strong growth in both its e-commerce and cloud businesses.

Shares are also affordable compared to their historical norm. The forward price-to-earnings ratio of 30x looks cheap when you consider the five-year mean is nearly 70x.

However, be warned that Amazon missed analysts' expectations for the last two quarters, and posted earnings of $1.56 per share in Q1 when analysts were looking for $1.60.

Amazon is an important company, and its $200 billion investment in AI infrastructure will likely pay off for it in the long run. But in the meantime, Amazon will have a hard time staying cash positive as it invests in AI and also manages the e-commerce business that historically has a low profit margin.

Domino’s Pizza

Under Buffett, Berkshire Hathaway embraced investing in brands with a loyal following, strong returns, and solid management. Domino’s Pizza (DPZ) is arguably the most well-known pizza chain in the U.S., but they are no longer a Berkshire holding.

Domino’s stock has been a laggard in the last year, dropping more than 35%. Revenue in the first quarter of $1.15 billion was up 3.2% from a year ago. But net income was down 6.6% to $139.8 million, and Domino’s missed analysts’ expectations of $4.29 per share by posting EPS of $4.13.

Thirty analysts who cover the stock rate it a “Moderate Buy” with a price target of $407 that represents 30% upside. Domino’s also offers a dividend that yields 2.6%.

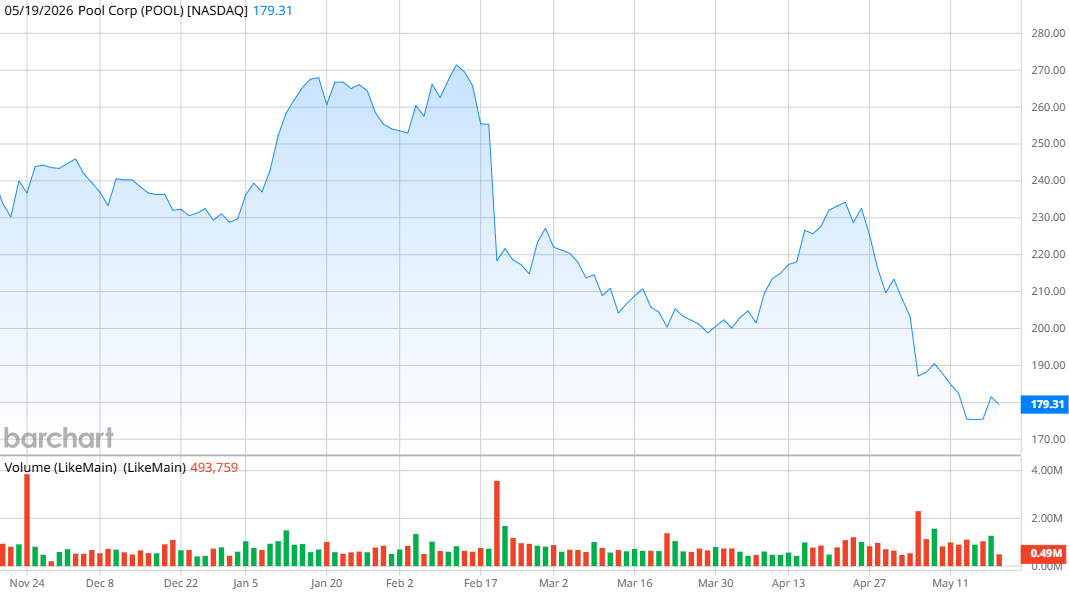

Pool Corp.

I’ve always thought about Pool Corp. (POOL) as a quintessential Buffett stock. The company sells and distributes outdoor equipment, as well as replacement parts and equipment for swimming pools. It has more than 2,200 suppliers around the world, with 80% of its business coming from builders or service professionals.

The brilliance of Pool Corp., in my eyes, was that there are countless home swimming pools that need frequent maintenance. Nearly two-thirds of Pool’s business comes from maintenance and repair product sales, which means that Pool doesn’t have to rely on new construction to make money.

Revenue in the first quarter was $1.14 billion, up from $1.07 billion a year ago, and earnings of $1.45 per share beat analysts’ expectations of $1.34 per share. Shares are down 44% in the year, but the 2.9% dividend yield can help ease the sting of that loss.

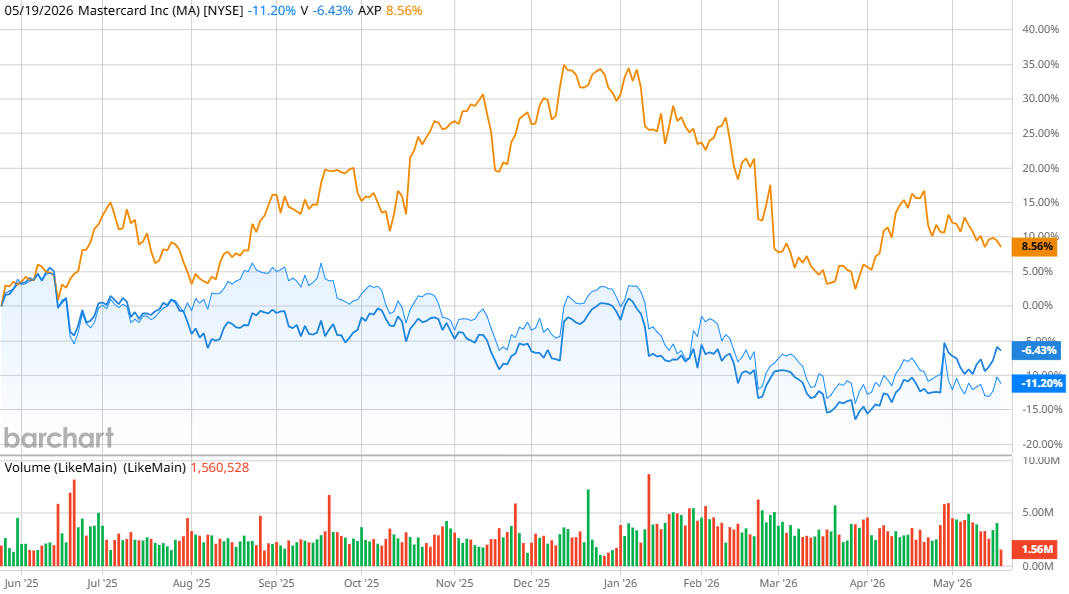

Mastercard

Berkshire Hathaway sold off its stake in both Visa (V) and Mastercard (MA) — while keeping its stake in American Express (AXP). But we’ll take a closer look at Mastercard here. The credit card company operates in 220 countries, with growth stronger internationally than in the U.S. In the first quarter, Mastercard saw its gross dollar volume increase by 4% in the U.S. to $795 billion, while it jumped 9% in the rest of the world to $1.90 trillion.

Net revenue in the quarter was $8.39 billion, up 12% on a currency-neutral basis. Net income was $4.10 billion, up 15%, and earnings of $4.60 per share topped analysts’ expectations of $4.40.

However, shares have been down nearly 11% in the last year, and the stock has been punished by the company’s agreement earlier this year to purchase a stablecoin infrastructure firm, BVNK. The $1.8 billion deal was expected to expand Mastercard’s reach in digital assets and crypto technology, but the crypto segment has been underperforming for several months. In comparison, American Express is up 8% over the last 12 months (and Berkshire has a 22% stake in AXP stock).

Mastercard offers a dividend with a small yield of 0.7%.

On the date of publication, Patrick Sanders did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Nvidia%20logo%20by%20Konstantin%20Savusia%20via%20Shutterstock.jpg)

/Apple%20products%20on%20desk%20by%20Ake%20Ngiamsanguan%20via%20iStock.jpg)