With a market cap of $65.3 billion, Simon Property Group, Inc. (SPG) is a self-managed REIT that owns, develops, and operates large-scale shopping, dining, entertainment, and mixed-use destinations across North America, Asia, and Europe. Through its operating partnership and strategic stakes in companies like Taubman Realty Group and Klépierre, it manages a vast portfolio of retail properties totaling over 183 million square feet globally.

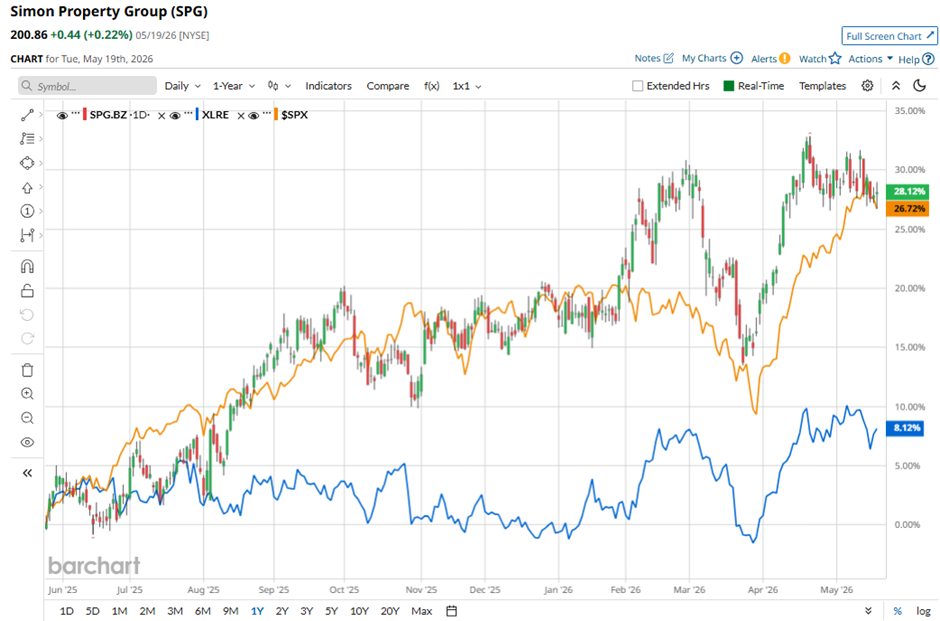

Shares of the Indiana-based company have slightly underperformed the broader market over the past 52 weeks. SPG stock has increased 22.1% over this time frame, while the broader S&P 500 Index ($SPX) has rallied 23.3%. However, shares of the company are up 8.5% on a YTD basis, slightly outpacing SPX’s 7.4% gain.

Zooming in further, shares of Simon Property Group have exceeded the State Street Real Estate Select Sector SPDR ETF’s (XLRE) 5.2% return over the past 52 weeks.

Shares of Simon Property Group rose 2.3% following its Q1 2026 results on May 11, with net income increasing to $479.6 million ($1.48 per share) from $413.7 million ($1.27 per share) a year earlier, while Real Estate FFO climbed 7.5% year-over-year to $1.21 billion, or $3.17 per share. Investors were also encouraged by solid operating metrics, including a 6.7% rise in domestic and portfolio NOI, occupancy improving to 96%, base minimum rent per square foot increasing 5.2% to $61.99, and retailer sales per square foot surging 11.8% to $819.

The stock additionally benefited from management raising its full-year 2026 Real Estate FFO guidance to $13.10 per share - $13.25 per share.

For the fiscal year ending in December 2026, analysts expect SPG’s Real Estate FFO to rise 3.7% year-over-year to $13.20 per share. The company’s earnings surprise history is promising. It beat the consensus estimates in the last four quarters.

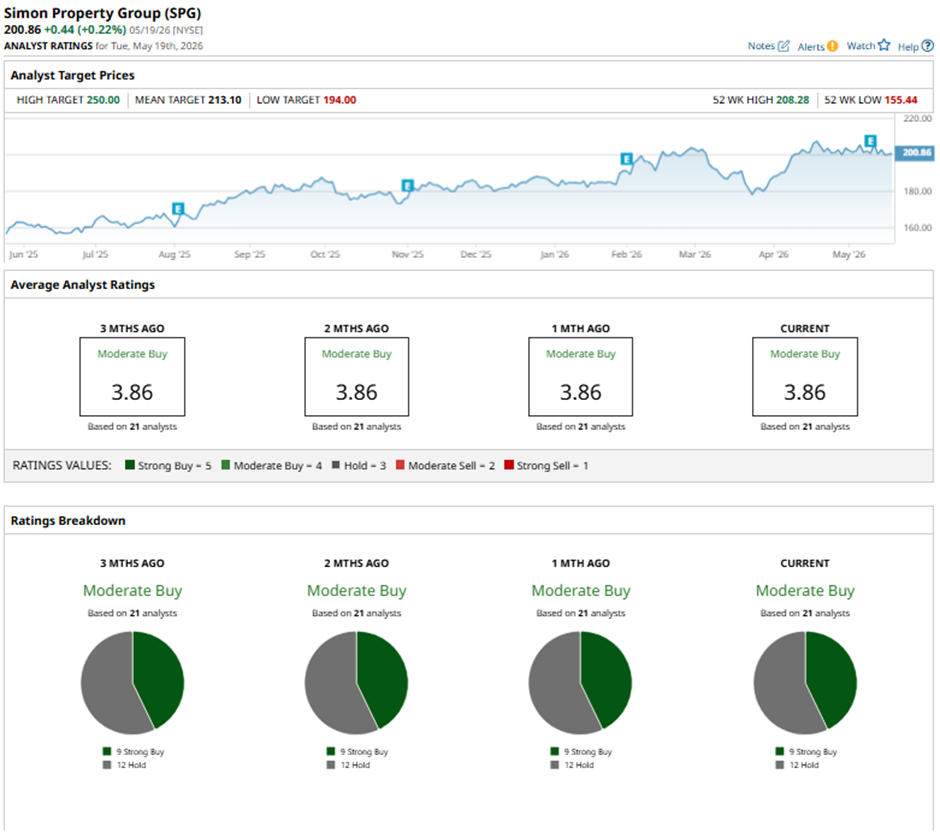

Among the 21 analysts covering the stock, the consensus rating is a “Moderate Buy.” That’s based on nine “Strong Buy” ratings and 12 “Holds.”

On May 15, Marie Ferguson of Argus Research reiterated a “Buy" rating on Simon Property Group and maintained a price target of $210.

The mean price target of $213.10 represents a 6.1% premium to SPG’s current price levels. The Street-high price target of $250 suggests a 24.5% potential upside.

On the date of publication, Sohini Mondal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20headquarters%20By%20Peter.jpeg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)

/Robot%20arm%20industrial%20automation%20manufacturing%20by%20Eakrin%20via%20Adobe%20Stock.jpeg)