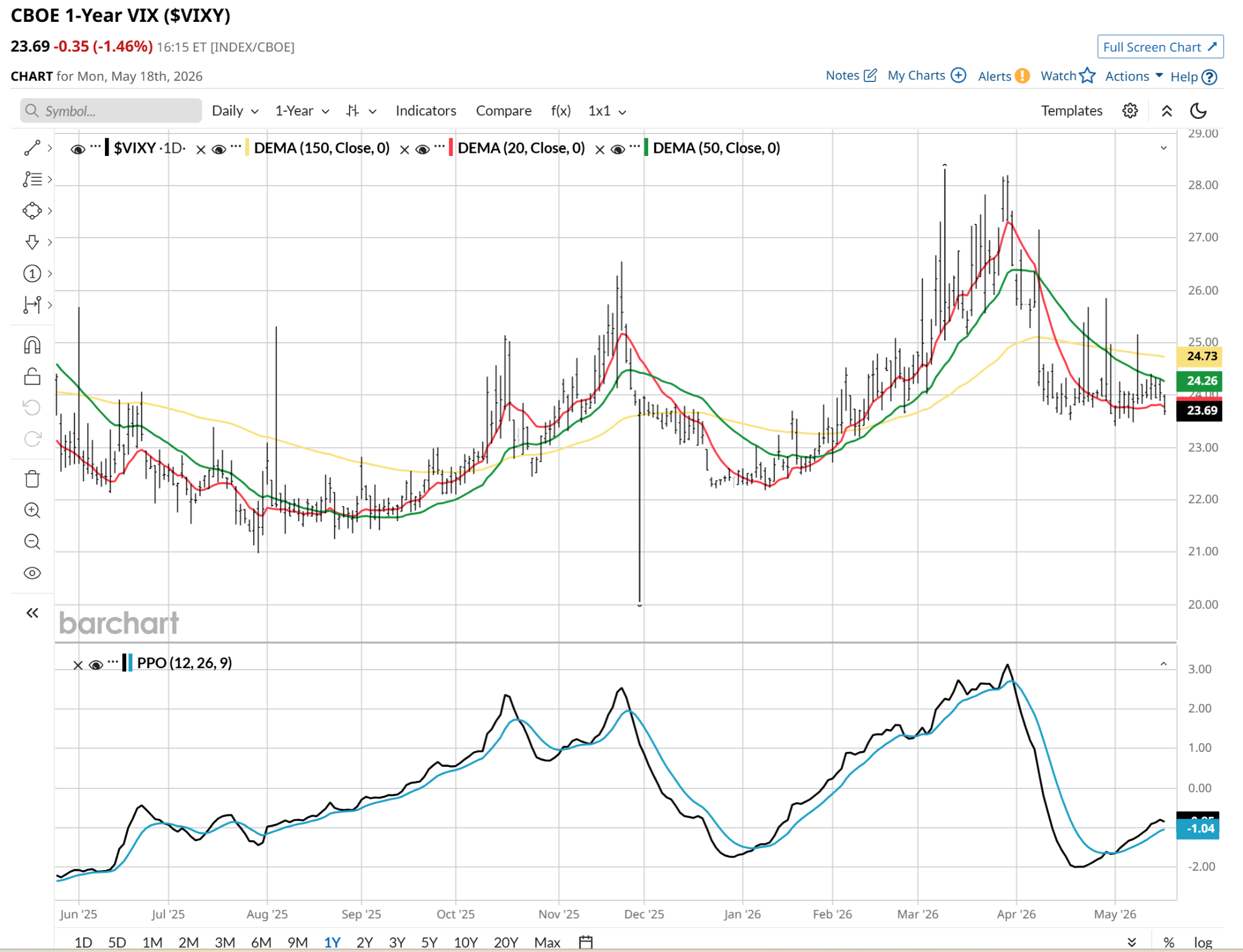

Something incredibly counterintuitive is underway: The major equity indexes are sliding, red screens are multiplying, yet the CBOE Volatility Index ($VIX), and by extension, long-volatility ETFs like VXX and VIXY, are actually flat or falling.

Under classic market logic, when stocks go down, the VIX is supposed to go up. When that relationship breaks, it flashes a bright red flag.

What Is the VIX Warning Us About?

It is only a short-term phenomenon so far, but it bears watching. VIX dipped with the S&P 500 Index ($SPX) over the past couple of days. That’s not an enduring trend, but it is more than a single isolated incident. And since VIXY is one of the 10 ETFs in my ROAR 10 ETF model portfolio, I am on alert with even a modest event like that. And I’m certain I’m not the only one.

Part of the explanation is that the VIX does not measure actual stock market movement. It measures the demand for insurance over the next 30 days. It is anticipatory.

When the market experiences a slow, orderly grind lower rather than an impulsive panic, institutional traders do not rush to buy protective put options. They have already adjusted their positions. Because the VIX is calculated from S&P 500 option premiums, a lack of panic-buying keeps the VIX artificially suppressed.

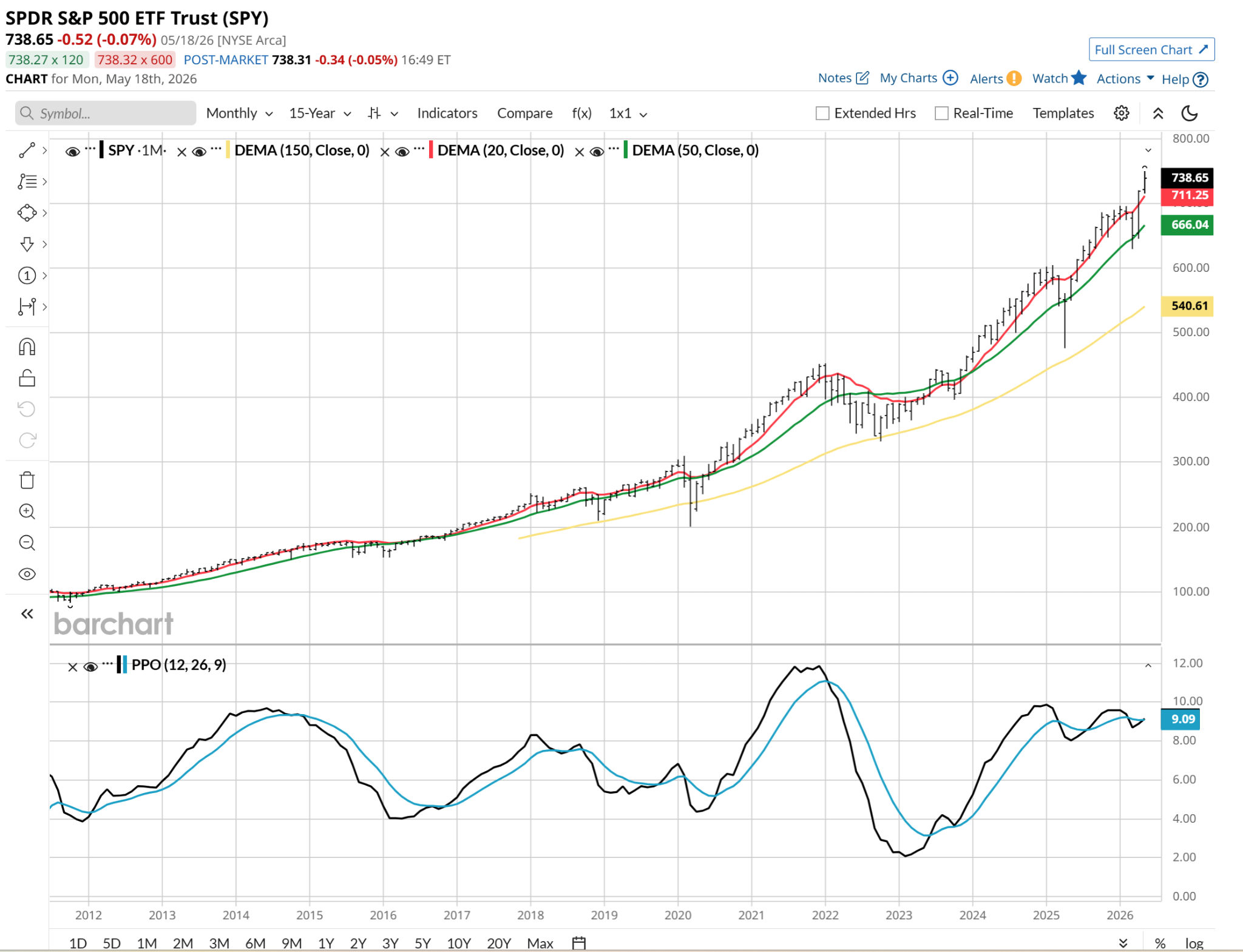

This could be as simple as evidence that institutional trading and hedging activity is a bit complacent. When the market drops and the VIX declines, it means market participants are treating the selloff as a temporary, non-threatening event. And with this chart in mind, showing SPY going back 15 years, who can blame them for being complacent?

This creates a blind spot, where investors assume the coast is clear purely because the fear gauge isn’t spiking.

The Structural Red Flag: Is There a New ‘0DTE Effect?’

The deeper, more systemic warning is what this tells us about market structure.

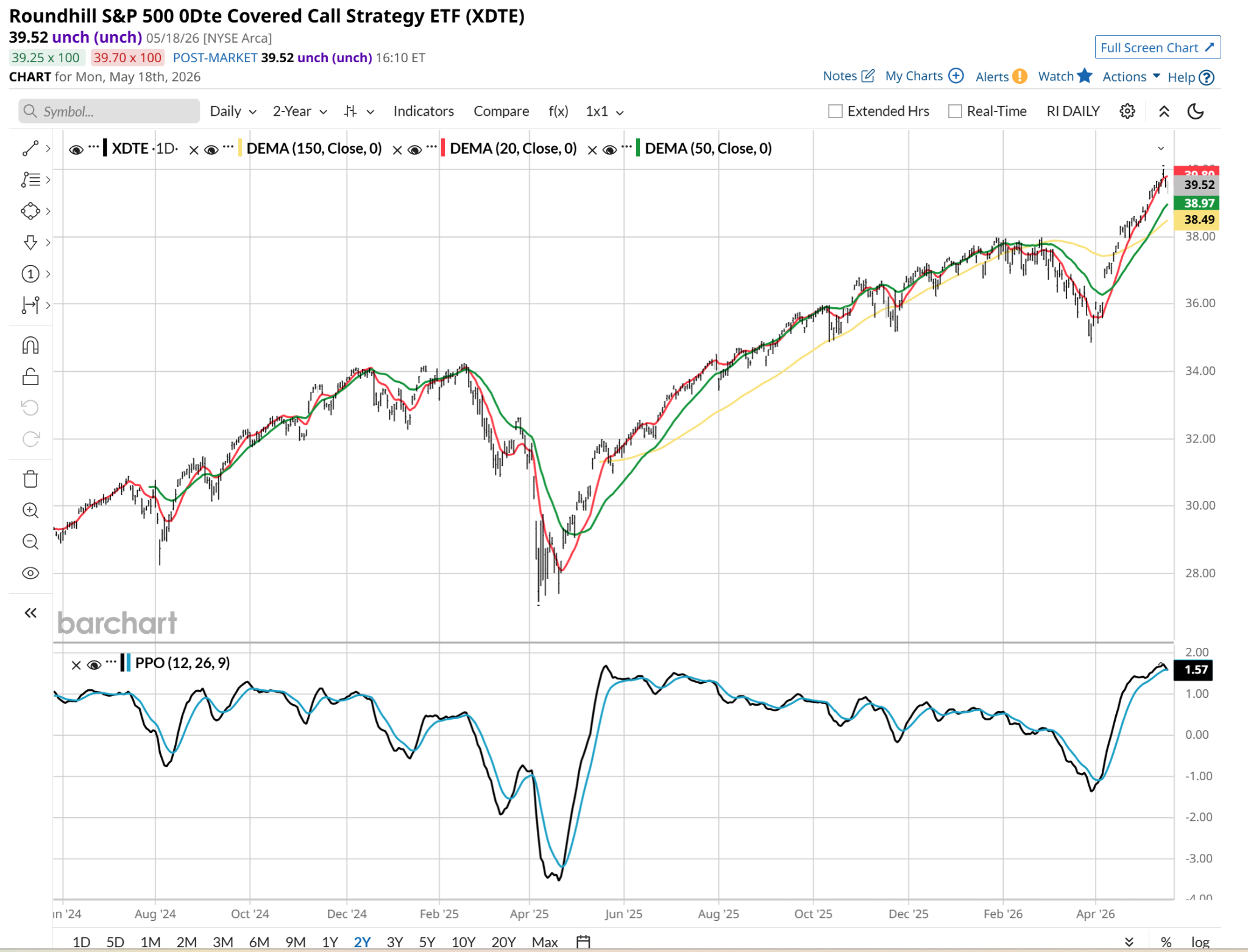

In recent years, the explosion of short-term options trading — specifically zero-days-to-expiration (0DTE) contracts — has fundamentally altered how volatility behaves. We even have ETFs that are devoted to daily covered call writing on the S&P 500, such as the Roundhill S&P 500 0DTE Covered Call Strategy ETF (XDTE).

Big Wall Street firms and a massive wave of popular new funds (like covered call ETFs) are making money by constantly selling “market insurance” to other investors. Think of it like a bunch of companies flooding the market to sell smartphone insurance because the payouts are high. This massive supply of insurance has created a feeding frenzy that will eventually backfire.

When these big firms sell this insurance, they have to protect themselves by constantly buying and selling the actual stocks in the index. This robotic, non-stop trading acts like a giant shock absorber. It squashes any normal daily ups and downs, which tricks the VIX (the market’s “fear gauge”) into staying low and looking calm.

To make things worse, everyone is now trading ultra-fast options that expire on the exact same day. Because the VIX only looks at the next 30 days, these same-day options are completely invisible to it. The danger hasn’t vanished; it’s just hiding where the fear gauge can’t see it.

Furthermore, if you buy a VIX ETF hoping to profit when the market drops, you might be set up to lose. These ETFs don’t actually own the VIX itself; they buy VIX futures contracts.

When the market slowly grinds lower without panicking, next month’s contracts are more expensive than this month’s contracts. To stay open, the ETF is forced to sell low and buy high every single day. This constant losing trade burns through cash, meaning your ETF will lose money even while the stock market is falling.

We’re not there yet, but this is a threat to my own “way of life” as an ETF portfolio creator. Sure, I can swap out VIXY for an ETF that shorts an index (maybe even with leverage). But VIX-based ETFs get more of that leveraged effect without requiring much capital outlay.

Still, the gauntlet has been thrown. Historically, when the market pretends everything is perfectly predictable like this, it is highly unstable. It almost always ends with the financial version of a sudden, violent earthquake. A stagnant VIX in a falling market would be a warning that the eventual breakdown will be a gap-down event, not a slow slide.

Why? Because when volatility is artificially suppressed by systematic selling and structural option positioning, the market looks deceptively stable. Protection is underpriced relative to actual market risk, so the moment a catalyst forces these short-volatility managers to unwind their positions, the rebalancing loop reverses.

The red flag isn’t that the market is falling, it’s that the spring is being wound tighter and tighter. When the release happens, the vol spike will be sudden, violent, and highly disruptive to anyone relying on a low VIX as a sign of safety.

I know I’m watching this carefully, daily, as a trader. But the long-term investor in me (yes, I’m both) is equally concerned, since a systemic market “event” that has a VIX-induced helper in the way described above has a very 1987 vibe to it. As with so much in today’s markets, it is a real risk. Not realized, and may not be. But a risk nonetheless.

Rob Isbitts created the ROAR Score, based on his 40+ years of technical analysis experience. ROAR helps DIY investors manage risk and create their own portfolios. For Rob’s written research, check out ETFYourself.com.

On the date of publication, Rob Isbitts did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Netflix%20on%20tv%20with%20remote%20by%20freestocks%20via%20Unsplash.jpg)