If you own Intuit (INTU) stock, put a big circle around May 20. That’s when the TurboTax and QuickBooks parent will open its books on their third‑quarter fiscal 2026 after the closing bell, with management talking investors through the results later that day. This update comes from a company that has become a go-to name in tax software, small‑business accounting, and consumer finance. But now, it's getting picked apart more closely by the market.

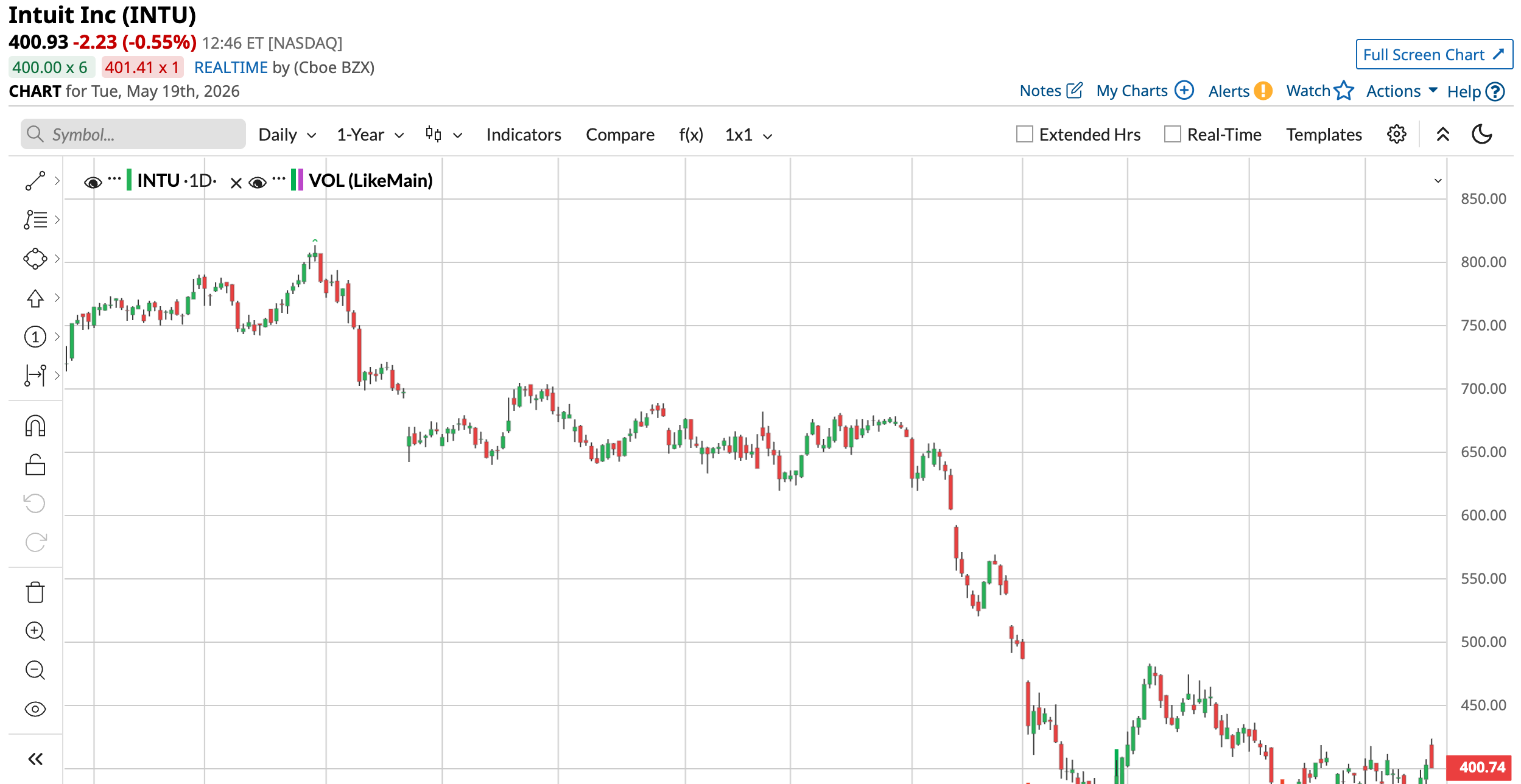

The setup is pretty straightforward. Intuit’s share price has taken a heavy hit, trading 50% below its 52-week high and leaving many long‑time holders asking hard questions. That kind of drop turns this earnings release into more than just a routine quarterly update.

So, dear Intuit stock fans, the question practically asks itself. Will May 20 bring the confirmation bulls have been hoping for or another round of doubt about whether this company can keep growing at the pace investors once expected? Let’s dive in.

Intuit’s Current Financial Snapshot

Intuit is a California‑based software company that makes tax tools, small‑business accounting software, personal finance products, and marketing solutions for both individuals and companies. Its lineup includes TurboTax, QuickBooks, Credit Karma, and other products that give it solid footing across many parts of the financial tech world.

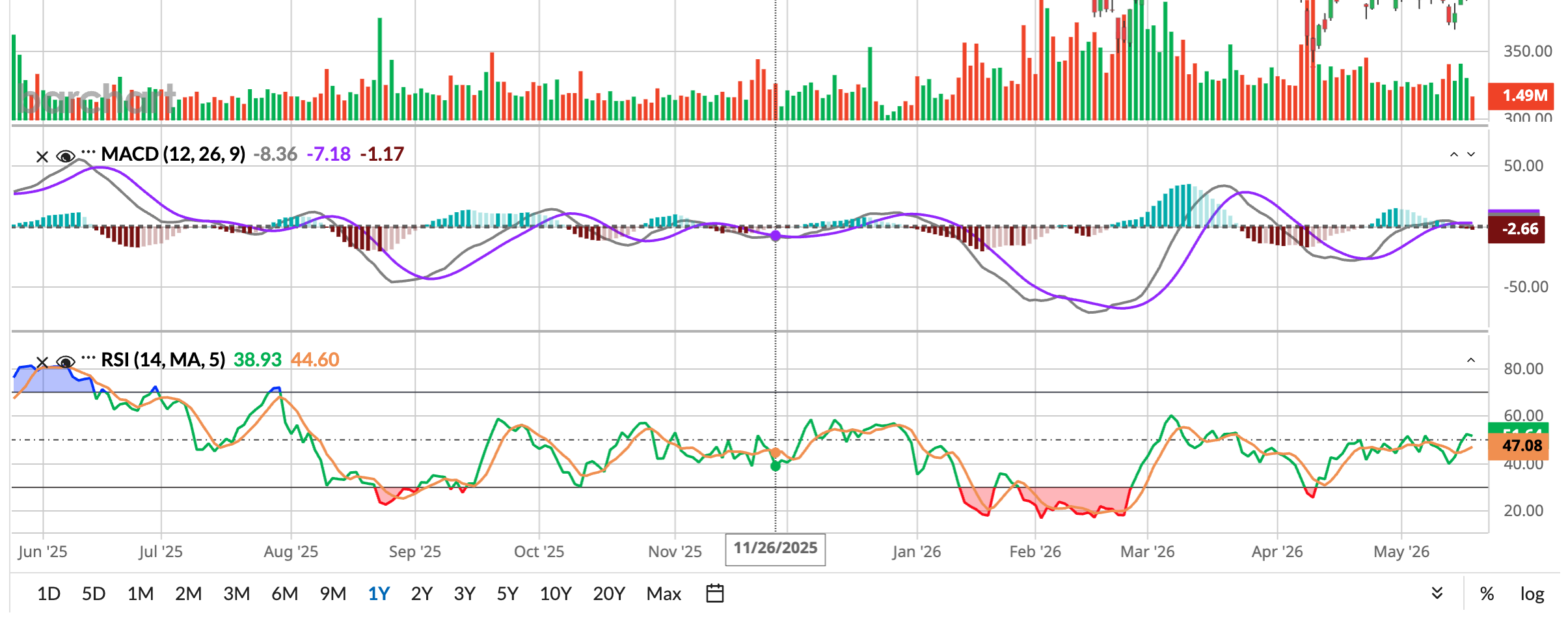

Intuit's has a year‑to‑date (YTD) return of -38.9% and a 52‑week move of -39.67%, along with a market value of $111.5 billion.

The stock trades at 26.19 times trailing earnings, below the sector median of 35.03 times, while its price-to-cash-flow ratio is 15.97 times, under the sector median of 18.17 times. Additionally, Intuit pays a forward annual dividend of $4.80 per share, which works out to a yield of about 1.27%.

The latest reported quarter, released on Feb. 26, showed total revenue of $4.7 billion, up close to 20%. For the same quarter ending in Jan. 2026, Intuit posted EPS of $2.83, which beat the $2.23 consensus estimate by 26.91%.

This update noted that Consumer revenue reached $1.5 billion, up 15%. It also showed Credit Karma revenue at $616 million, up 23%, and TurboTax revenue at $581 million, up 12%, which shows each part of the business pulling its weight.

Their GAAP operating income rose to $855 million, a 44% increase, and its non‑GAAP operating income moved to $1.5 billion, up 23%. Those results were backed by strong operating cash flow. Intuit generated about $2.21 billion in operating cash flow in January 2026, which was up 246.47%, while net cash flow came in at about -$2.70 billion, with a change of -6.30%.

Intuit’s Key Growth Initiatives

Intuit recently laid out what it sees as a new growth path in the mid-market. The idea is to combine data and AI so finance and operations teams can make faster and more profitable decisions, using tools that pull real-time information into one place and handle routine analysis. This push leans on Intuit Enterprise Suite and AI agents to turn scattered financial data into useful insights.

Further, the company is making a bigger move in payments. In early April 2026, Intuit completed the Federal Reserve’s FedNow Service certification. That gives it the ability to support instant payments across its ecosystem and help small and mid-market businesses get paid faster, access funds right away, and manage cash flow with more confidence.

AI is another part of the story, but in a practical way. Intuit has partnered with Anthropic to roll out more capable AI assistants across its products. The goal is to automate tasks like data entry, reconciliation, tax questions, and anomaly detection. If that cuts down manual work and keeps customers more engaged, it could help both revenue growth and margins.

Intuit has teamed up with Affirm (AFRM) to add a pay-over-time option to QuickBooks Online. That gives small businesses a way to offer flexible payment plans to customers without taking on the credit risk themselves.

Wall Street's Expectations

May 20 is getting close, and Intuit is set to report its quarterly earnings after the closing bell that day. For the April 2026 quarter, the average earnings estimate is $11.13 per share. That is up from $10.44 in the same quarter last year and points to expected year-over-year (YOY) growth of 6.61%.

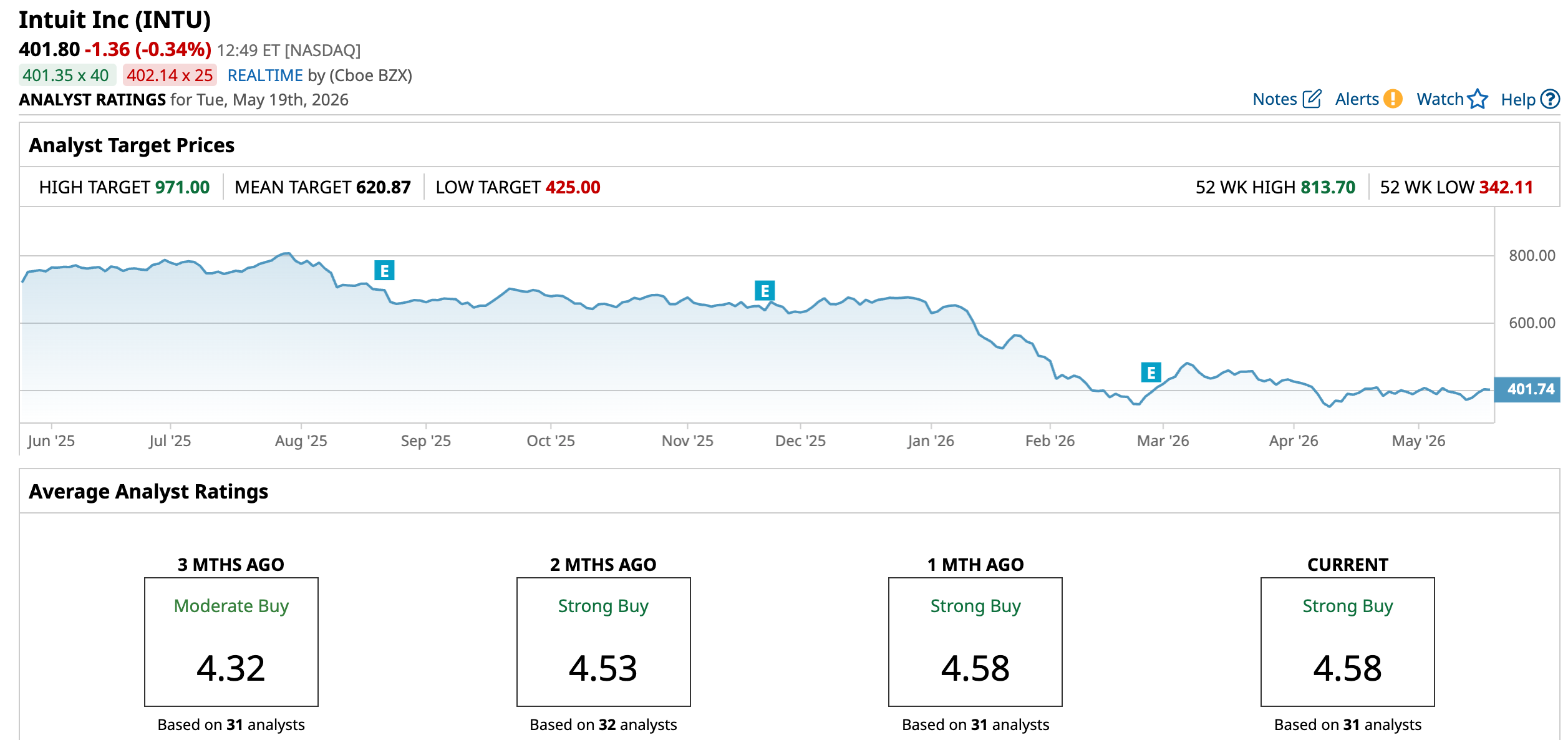

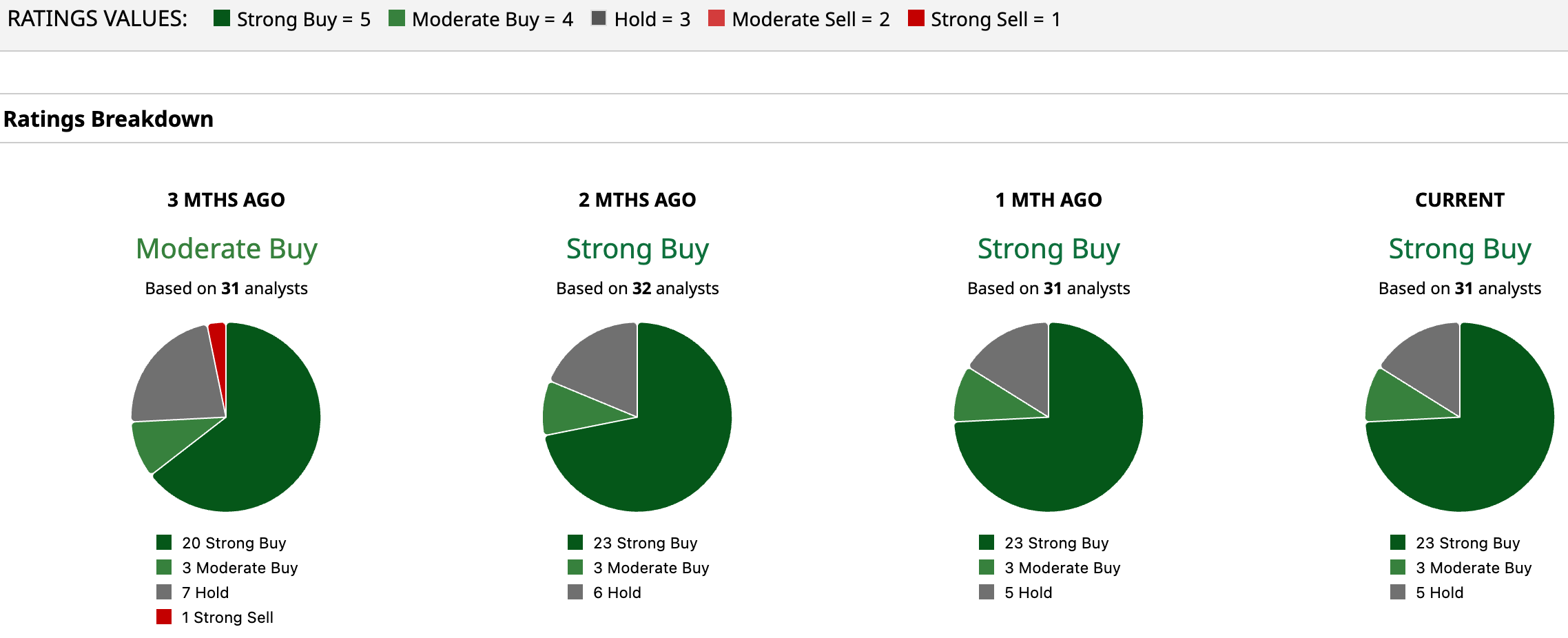

Wall Street still looks broadly positive on the stock, even though some price targets have come down. BMO Capital, for instance, cut its target on Intuit to $624 from $810. Still, it kept its “Outperform” rating, which suggests the firm has become more careful on valuation but has not turned negative on the story.

The broader analyst view is even more supportive. INTU carries a consensus “Strong Buy” rating based on 31 analyst views. Their average price target stands at $620.87, which implies about 54.5% upside from current levels.

Conclusion

In the end, May 20 looks like a real turning point for the way in which the market treats Intuit’s mix of solid fundamentals, new AI and mid‑market bets, and a beaten‑down share price. The most likely near‑term move is higher if the company delivers strong results and steady guidance, although any slip could put a real recovery on pause. Either way, this earnings report should do a lot to shape next steps for INTU.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20concept%20image%20showing%20a%20lightbulb%20with%20planet%20earth%20in%20a%20mossy%20green%20background%20by%20Capt_Pic%20via%20Shutterstock.jpg)

/The%20CrowdStrike%20logo%20on%20an%20office%20building%20by%20bluestork%20via%20Shutterstock.jpg)

/An%20image%20of%20a%20Tesla%20humanoid%20robot%20in%20front%20of%20the%20company%20logo%20Around%20the%20World%20Photos%20via%20Shutterstock.jpg)