/Chubb%20Limited%20office%20sign-by%20Poetra_%20RH%20via%20Shutterstock.jpg)

With a market cap of $128.1 billion, Chubb Limited (CB) is a global insurance and reinsurance company that offers a wide range of commercial and personal insurance products across six business segments. The company provides coverage solutions including property and casualty insurance, life insurance, crop insurance, reinsurance, and specialty products such as cyber, aviation, and professional liability insurance.

The insurer's shares have underperformed the broader market over the past 52 weeks. CB stock has risen 12.7% over this time frame, while the broader S&P 500 Index ($SPX) has rallied 23.2%. Moreover, shares of the company are up 6.3% on a YTD basis, compared to SPX’s 7.3% gain.

In addition, shares of Chubb have outpaced the State Street Financial Select Sector SPDR ETF’s (XLF) marginal return over the past 52 weeks.

Shares of Chubb Limited fell 1.2% following its Q1 2026 results on Apr. 21 as the company reported EPS of $5.88, which missed analyst expectations despite improving from $3.29 in the prior-year quarter. Investor sentiment was also pressured by a sharp increase in net realized losses, which rose to $407 million from $116 million a year earlier. Although Chubb posted strong underlying performance, including a 10.7% rise in net premiums written to $14.01 billion and core operating earnings of $6.82 per share, the earnings miss and higher realized losses overshadowed these positives.

For the fiscal year ending in December 2026, analysts expect CB’s core operating income to grow 8% year-over-year to $26.78 per share. The company’s earnings surprise history is promising. It beat the consensus estimates in the last four quarters.

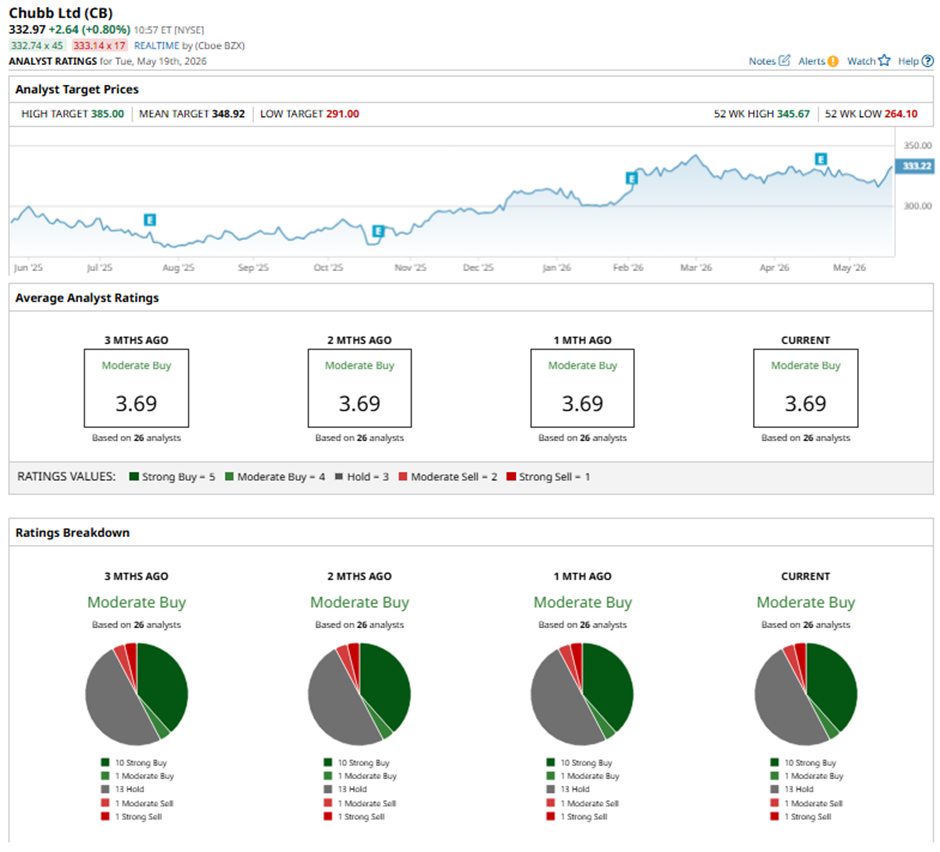

Among the 26 analysts covering the stock, the consensus rating is a “Moderate Buy.” That’s based on 10 “Strong Buy” ratings, one “Moderate Buy,” 13 “Holds,” one “Moderate Sell,” and one “Strong Sell.”

On Apr. 23, Elyse Greenspan of Wells Fargo raised the price target for Chubb Limited to $333 and maintained an “Equal Weight” rating.

The mean price target of $348.92 represents a 4.8% premium to DLTR’s current price levels. The Street-high price target of $385 suggests a 15.6% potential upside.

On the date of publication, Sohini Mondal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Nvidia%20logo%20by%20Konstantin%20Savusia%20via%20Shutterstock.jpg)

/Apple%20products%20on%20desk%20by%20Ake%20Ngiamsanguan%20via%20iStock.jpg)

/McDonald's%20Corp%20arches%20by-%20TonyBaggett%20via%20iStock.jpg)