/Technology%20by%20Alexandre%20Debieve%20via%20Unsplash.jpg)

Sandisk (SNDK) is still riding one of the hottest trades in the market. The memory and storage name has become a poster child for the AI buildout, with investors betting that data-center demand will keep NAND tight and pricing firm. That is the bigger backdrop for the stock right now: The whole storage group has been swept up in the AI boom, and Sandisk has been one of the clearest beneficiaries.

The latest wrinkle is not another earnings surprise, but a mini-tender offer from Tutanota LLC that expires on May 20, a date Sandisk has told shareholders to notice and, if they have not responded, to take no action.

Sandisk Rejects Offer

The mini-tender issue itself is relatively small, but it matters because it highlights how much investor attention Sandisk is attracting right now. Tutanota’s unsolicited offer seeks to buy up to 100,000 shares at $1,150 each, representing less than 0.07% of Sandisk’s outstanding stock. The offer expires at 5 p.m. Eastern Time on May 20 unless extended. Sandisk warned shareholders that the deal could effectively result in a below-market sale price and recommended investors reject the offer or take no action. The SEC has also previously warned investors about mini-tender offers because they avoid some disclosure protections tied to larger tender offers.

How Did Sandisk Stock Perform?

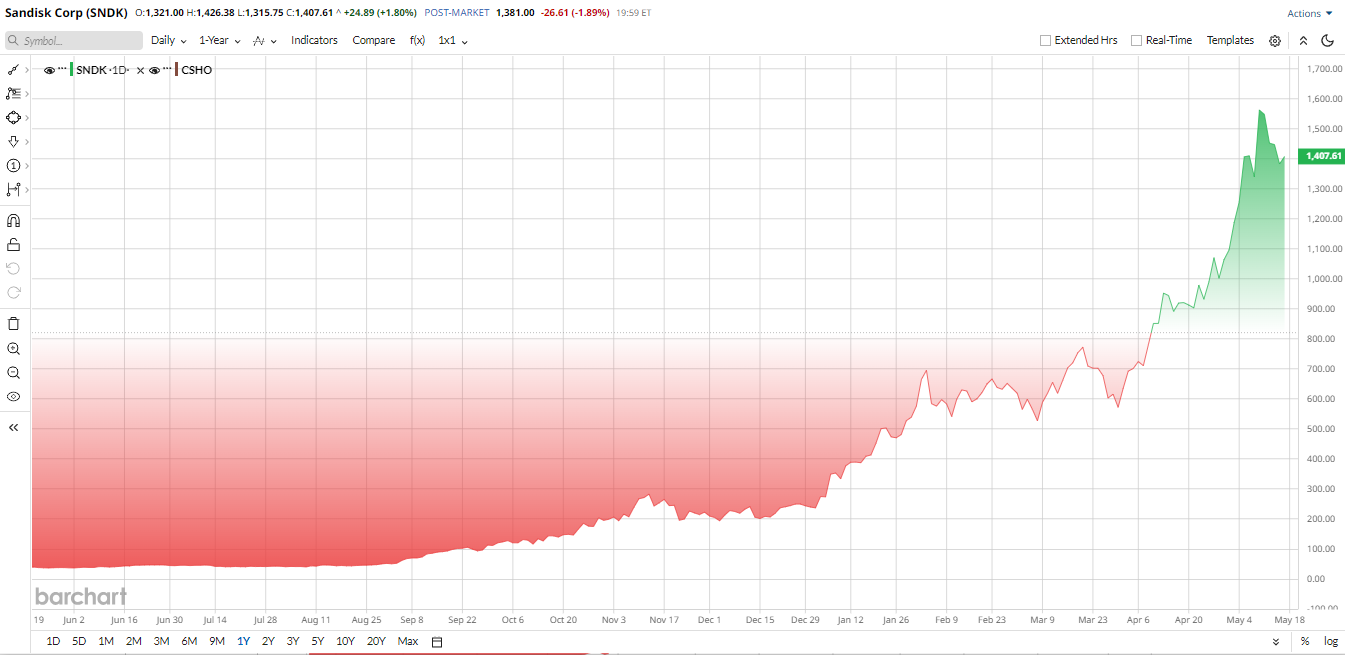

The stock has been the big story in 2026. Barchat data put it up about 493% year to date (YTD) and roughly 2,794% since its February 2025 spin-off from Western Digital (WDC), with the move driven by AI demand, tight memory supply, and the market’s willingness to pay up for companies exposed to the storage bottleneck. Even after a few sharp post-earnings swings, the trend has been hard to ignore.

Valuation is where the debate gets more interesting. Using Sandisk’s recent market value of about $208 billion and bullish revenue expectations for fiscal 2026, the stock trades near 10 times forward sales. That is below some AI-linked semiconductor peers, but still elevated for a memory business that historically has been cyclical. Investors are essentially betting that AI-driven demand can keep memory pricing stronger for much longer than in prior cycles.

Earnings Momentum Is Still Driving the Story

The real reason Sandisk remains one of the market’s hottest semiconductor names is simple: The business is booming. The company recently posted another massive quarterly beat, with revenue more than doubling year-over-year to nearly $6 billion as AI-driven storage demand accelerated. Adjusted earnings also came in well above Wall Street expectations, while data-center revenue surged 645% year-over-year.

More importantly, management’s guidance stayed aggressive. Sandisk projected current-quarter revenue of roughly $7.75 billion to $8.25 billion and adjusted EPS of $30 to $33, both ahead of analyst expectations. Investors are now watching whether the company can continue sustaining that kind of growth as hyperscalers and AI infrastructure companies keep spending heavily on storage capacity.

The company has now beaten expectations for multiple consecutive quarters, which is one reason the stock keeps attracting momentum investors despite valuation concerns. Last quarter alone, revenue growth and profitability improved sharply as NAND pricing recovered and enterprise SSD demand accelerated.

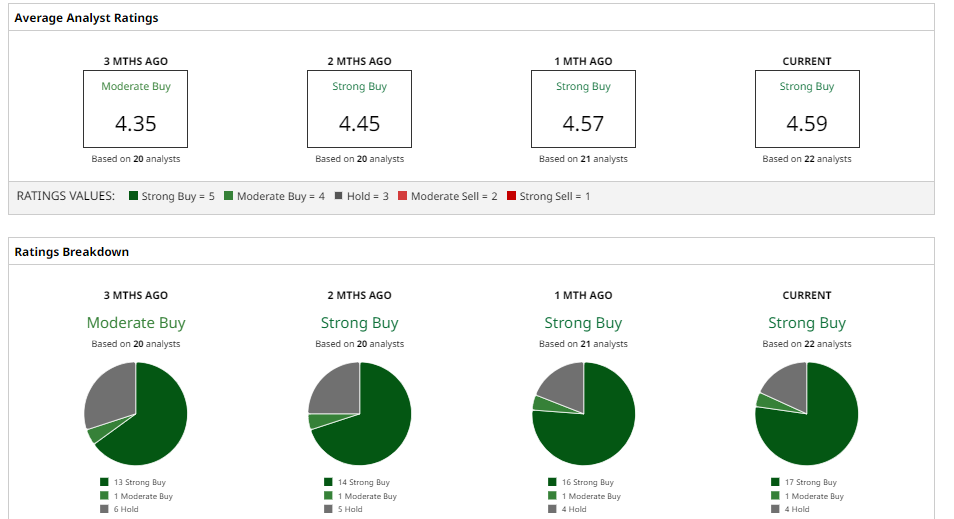

What Analysts Are Saying About Sandisk

Wall Street still largely believes the rally can continue, even if expectations are becoming harder to satisfy. Its consensus rating is “Strong Buy,” with an average price target of around $1,532, about 19% above current levels. For example, Morgan Stanley’s Joseph Moore recently raised his price target to $1,100 and emphasized that “NAND near-term strength is discounted,” he expects pricing to stay strong “as long as we remain at maximum AI investment.”

Moreover, Goldman Sachs’ James Schneider lifted his target to $1,200 after Sandisk’s blowout quarter, noting the business is supported by “strong pricing, tight supply-demand, and rising data center SSD demand.”

Bank of America echoed the excitement, boosting its target to $1,550 after Sandisk posted a “strong beat” and guided “massively above Street expectations."

The broader analyst view is that Sandisk’s biggest risk is not weak demand today, but rather how long the current AI-driven memory cycle can realistically last.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Netflix%20open%20on%20tablet%20by%20rswebsols%20via%20Pixabay.jpg)