For decades, Take-Two Interactive Software (TTWO) has lived at the center of the gaming world, building massive franchises that turn every new release into a cultural event. But nothing in its portfolio carries the weight of Grand Theft Auto VI. The GTA franchise started back in 1997 as a simple top-down PC game before evolving into a global phenomenon through Vice City, San Andreas, GTA IV, and eventually GTA V – a title that became one of the best-selling entertainment products ever made.

Now, more than a decade after GTA V launched, investors are once again hanging on every rumor, trailer tease, and preorder update surrounding GTA 6. Excitement surged recently after reports suggested Rockstar Games could release the game’s third trailer on May 18, alongside opening preorders ahead of the holiday shopping season. That optimism gave Take-Two Interactive stock a much-needed boost after months of frustration.

The excitement matters because investors badly needed good news. Multiple delays pushed the game from its original 2025 window to a November launch target, and the latest postponement hammered the stock hard. Shares are still down sharply from those levels and haven’t fully recovered this year.

With all eyes now on Take-Two’s Q4 earnings report this week, Wall Street is waiting for one thing above all else – fresh updates on Grand Theft Auto VI during the earnings call. After months of delays, excitement, and market swings, investors are now asking whether GTA 6 can finally reignite momentum for TTWO stock.

About Take-Two Interactive Stock

Take-Two Interactive is one of the biggest names in gaming, building blockbuster franchises that span consoles, PCs, and mobile devices worldwide. Founded in 1993 and headquartered in New York City, the company sits behind powerhouse titles like Grand Theft Auto V, Red Dead Redemption, NBA 2K, Borderlands, BioShock, Mafia, Civilization, and WWE 2K.

Through Rockstar Games, 2K, and Zynga, Take-Two covers everything from cinematic open-world adventures to sports simulations and hit mobile games like FarmVille, Toon Blast, and Zynga Poker. Its games reach players through retail stores, digital downloads, online platforms, and cloud streaming, making Take-Two a major force across the global entertainment industry. Its market cap currently stands at $44.9 billion.

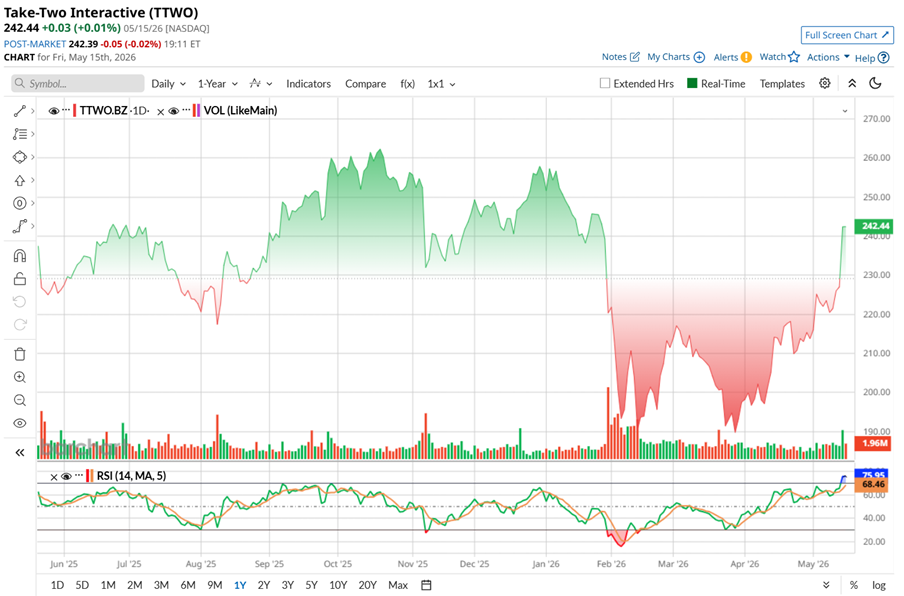

Still, owning the shares of the video game publisher over the past year has hardly been a smooth ride. Shares climbed to a high of $264.79 last October but tumbled to a low of $187.63 by March 2026.

But lately, the mood has started shifting again. TTWO stock has bounced 28.8% from its March lows, climbed 13.47% over the past month, and is up 8.64% over the past five days alone. The upward momentum recently is because investors have regained confidence that GTA VI is finally on track for its planned November launch. That matters because many see the game as more than just another release. It is expected to become Take-Two’s next major cash machine for years through game sales, online content, and future monetization opportunities.

Optimism is also building ahead of the company’s May 21 earnings report, where investors hope management will reinforce the launch schedule and provide a clearer growth outlook. Adding fuel to the rally, UBS recently named Take-Two its top pick in the U.S. gaming sector, another sign Wall Street is warming up to the story again.

Technically, though, the stock’s 14-day RSI has climbed into overbought territory, suggesting the recent rally may be running a little too hot in the short term.

A Snapshot of Take-Two Interactive’s Q3 Numbers

Take-Two Interactive released its Q3 figures in February, and the company raked in revenue of $1.7 billion, marking a growth of 25% year-over-year (YOY), exceeding not just the company’s forecast but also Wall Street’s projections. It shows that demand across its gaming portfolio remained strong even before the launch of Grand Theft Auto VI.

In addition, losses improved during the quarter. Take-Two posted a net loss of $92.9 million or -$0.50 per share, compared to a loss of $125.2 million or $0.71 per share, in the same period last year, another result that came in better than analysts expected.

Game revenues, which accounted for more than 92% of total revenue, climbed 26.3% YOY to $1.57 billion. Advertising revenue, while much smaller at 7.6% of total sales, still rose 10.3% annually to $128.7 million.

Net Bookings, one of the company’s most closely watched metrics, jumped 28% annually to $1.76 billion. The U.S. remained the largest market, generating $1.05 billion in bookings and accounting for nearly 60% of the total, while international bookings surged 33.6% to $710.1 million.

The growth came from a broad mix of franchises, including NBA 2K26, GTA Online, GTA V, Red Dead Redemption 2, Red Dead Online, WWE 2K25, Toon Blast, Toy Blast, Empires & Puzzles, Match Factory!, Words With Friends, and several mobile hits. Meanwhile, recurrent consumer spending – the steady stream of in-game purchases and live-service revenue that keeps publishers hooked on engagement – rose 23% YOY and made up 76% of total bookings.

Financially, the company still looks well-positioned heading into its biggest game launch. As of Dec. 31, 2025, Take-Two had $2.16 billion in cash and cash equivalents. Over the first nine months of fiscal 2026, operating cash flow reached $388.9 million, while capital expenditures totaled $126 million, giving the company solid financial flexibility as the GTA VI countdown continues.

The company is set to report its fiscal fourth-quarter and full-year 2026 results after the market closes on Thursday, May 21, and investors will be listening closely for any fresh clues surrounding GTA 6 and the company’s broader growth outlook.

For fiscal 2026, Take-Two now expects revenue between $6.55 billion and $6.6 billion, while net bookings are projected between $6.65 billion and $6.7 billion, representing roughly 18% annual growth. The stronger forecast reflects better-than-expected Q3 performance and rising momentum across several major franchises heading into the final quarter.

Once again, the business is not leaning on just one title. Management expects the biggest booking contributions to come from NBA 2K, the GTA franchise, Borderlands, Red Dead Redemption, Toon Blast, Match Factory!, Empires & Puzzles, Color Block Jam, and Words With Friends. Recurrent consumer spending is expected to rise around 17% and account for nearly 78% of total bookings, a meaningful jump from prior forecasts.

Operating cash flow is now projected at around $450 million, almost double the company’s earlier estimate of $250 million, highlighting how much momentum the business has regained over the past few quarters. CapEx is expected to remain near $180 million as the company continues investing in future growth.

In Q4, revenue is expected between $1.57 billion and $1.62 billion, while losses are projected in the range of $0.70 to $0.54 per share. Even with those expected losses, management continues sounding highly confident about the road ahead, arguing that GTA VI and the company’s broader release pipeline could significantly expand Take-Two’s earnings power, strengthen the balance sheet, and drive long-term shareholder returns over the next several years.

Analysts monitoring Take-Two Interactive predict the company’s revenue for fiscal 2026 to be about $6.7 billion, while EPS is anticipated to be around $2.44. EPS is expected to rise by 175% YOY to $6.70 in fiscal 2027.

What Do Analysts Expect for Take-Two Interactive Stock?

Wedbush Securities also stayed bullish on Take-Two Interactive, maintaining its “Outperform” rating and $300 price target ahead of earnings. The brokerage firm believes the upcoming earnings call could become a major “go or no-go” moment for Grand Theft Auto VI. Wedbush noted Rockstar Games typically announces delays about six months before launch, meaning silence on another postponement during the upcoming earnings call would strongly reinforce confidence in the planned November release. The firm also pointed to leaked Best Buy preorder marketing emails as another sign that Take-Two likely feels confident about the timeline.

Beyond GTA VI hype, Wedbush expects strong Q4 results driven by mobile hits like Match Factory!, Toon Blast, and Color Block Jam, while Zynga’s newer direct-pay system could help margins. For Q4, Wedbush expects the company’s net bookings and EPS to be around $1.56 billion and $0.56, respectively. Looking ahead, the brokerage firm forecasts fiscal 2027 bookings of $9.4 billion and EPS of $6.40, arguing that GTA Online, subscriptions, and recurring digital revenue could make this gaming cycle even more profitable than previous ones.

Also, UBS remains firmly bullish on Take-Two Interactive, recently reiterating its “Buy” rating and $300 price target while naming the company its top pick in the U.S. gaming sector. Analyst Christopher Schoell believes investor fears around AI disruption and competition for player attention have become overblown.

Instead, UBS sees upcoming Grand Theft Auto VI trailers, gameplay reveals, and launch updates as major sentiment catalysts for the stock. The firm highlighted Take-Two’s strategic value as one of the last major publicly traded AAA game developers in the U.S., especially as consolidation continues across the gaming industry.

UBS expects GTA VI’s launch, combined with growing recurrent consumer spending and in-game monetization, to drive stronger and more stable long-term returns. The brokerage firm pointed to Take-Two’s transformation during the GTA Online and NBA 2K era in the mid-2010s, when recurring digital revenue helped shift the company from highly volatile cash flows to steadier, higher-margin economics. Take-Two’s strong execution history supports further expansion in profitability and cash-flow returns in the years ahead, as per UBS.

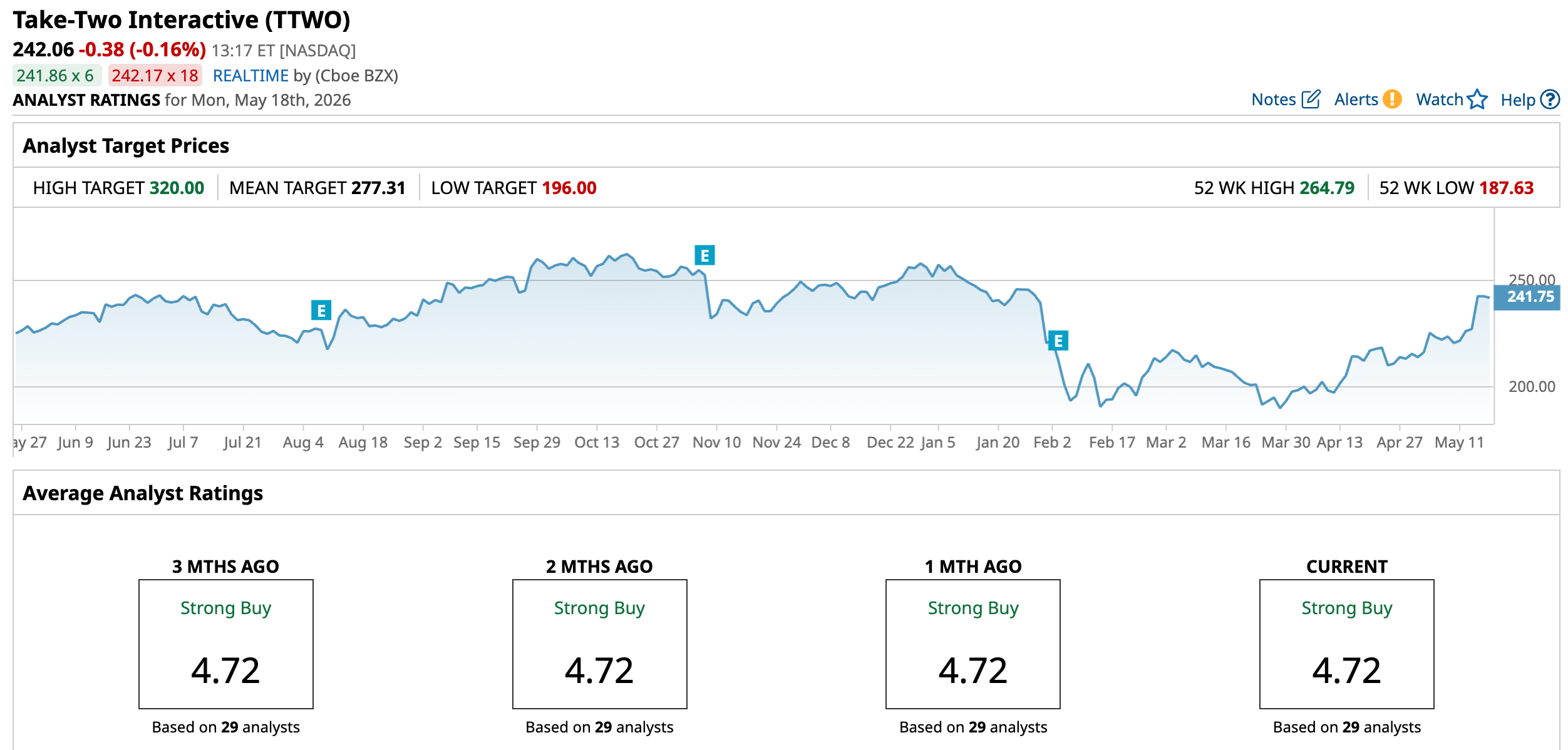

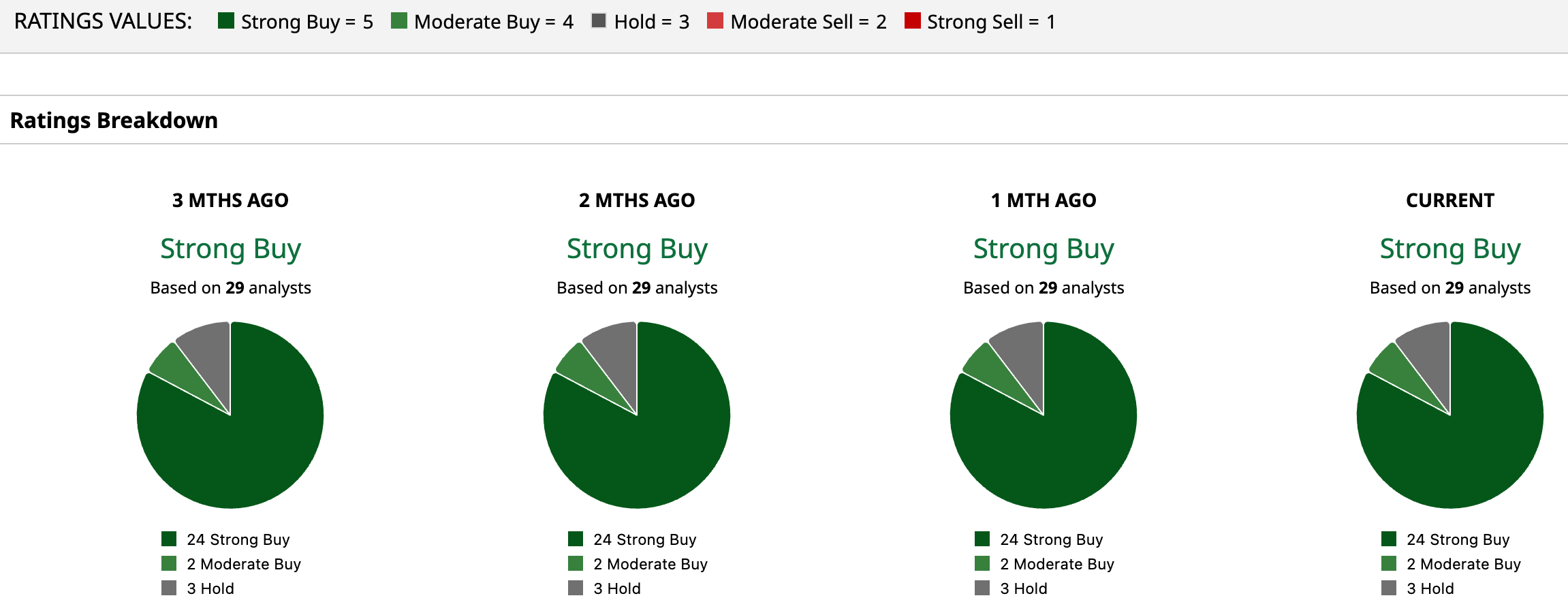

Wall Street analysts overall are upbeat on TTWO stock. The stock has a consensus “Strong Buy” rating. Among the 29 analysts covering the stock, 24 suggest a “Strong Buy,” two recommend a “Moderate Buy,” while three remain on the sidelines with “Hold” ratings. The average price target of $277.31 implies potential gains of 14.6% from current levels, while the Street-high target of $320 suggests shares could soar as much as 32.2% from here.

On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/AI%20(artificial%20intelligence)/AI%20engineer%20working%20on%20laptop%20by%20ART%20STOCK%20CREATIVE%20via%20Shutterstock.jpg)