/Oracle%20Corp_%20logo%20on%20phone%20and%20stock%20data-by%20Rokas%20Tenys%20via%20Shutterstock.jpg)

When the faster-growing tech titans like Amazon (AMZN), Apple (AAPL), Microsoft (MSFT), and Alphabet (GOOGL) (GOOG) moved into AI, Oracle (ORCL) got overshadowed as a slow-moving enterprise software company built for a different era. But, Oracle didn’t just sit back and watch the tech giants get ahead in the AI race. It was reshaping itself and now is one of the leading AI infrastructure companies in the market.

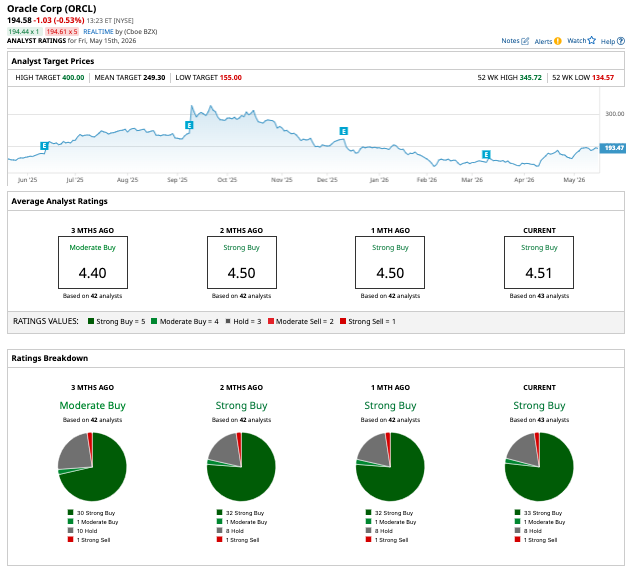

Its turnaround has surprised Wall Street, which upgraded the stock to a “Strong Buy” from a “Moderate Buy” three months ago. Furthermore, its massive backlog in Q3 has impressed investors. While ORCL stock is down 0.6% year to date, underperforming the broader market, it has surged 21% over the last three months.

Here’s why this legacy player remains an excellent addition to your portfolio.

Oracle’s Secret Weapon Was Its Age

Just when critics thought Oracle had become outdated with no focus on innovation, the company posted off-the-charts AI-related revenue in the third quarter of fiscal 2026. Its AI infrastructure revenue, in particular, soared 243% year-over-year, while the multi-cloud database revenue grew 531% YOY. Total revenue climbed 22% to $17.2 billion, while the company reported 21% increase in adjusted earnings to $1.79 per share.

However, the most striking achievement in the quarter was the backlog of $553 billion, which surged 325% from the prior-year quarter. This RPO (remaining performance obligation) is tied largely to AI contracts. This kind of growth is rare for a mature enterprise software company. In fact, Oracle’s long history is its biggest advantage.

Legacy players like Oracle have spent years building relationships with enterprises, governments, banks, telecom operators, retailers, and multinational corporations. Its databases store some of the most valuable and sensitive data. Oracle simply had to integrate AI directly into the software these companies already use. CEO Mike Sicilia emphasized that Oracle’s Fusion systems now act as keepers of mission-critical enterprise data, making them the perfect foundations for AI agents and enterprise automation. Notably, in Q3, Fusion ERP revenue rose 14%, Fusion SCM climbed 15%, Fusion HCM increased 15%, Fusion CX grew 6%, and NetSuite advanced 11%.

Multi-Cloud Partnerships Became a Growth Machine

Instead of competing directly with the cloud giants, Oracle’s multi-cloud partnerships has become its most important growth driver. The company specified that it now has 33 database services or “regions” live with Microsoft and 14 with Google. Additionally, it expects AWS regions to grow from eight at the end of Q3 to 22 by the end of Q4. This strategy reduces complexity, data transfer delays, and higher costs. As a result, this expansion has sparked massive enterprise demand from customers seeking Oracle databases within their preferred cloud environments. And this is one reason why Oracle’s multi-cloud database revenue surged triple-digit in the quarter.

Oracle’s AI transformation is so aggressive that it is planning a massive funding push, where in it plans to raise between $45 billion to $50 billion in 2026. This funding will be a mix of equity and debt financing and will mainly focus on meeting additional AI cloud infrastructure demand from major customers including Meta (META), Nvidia (NVDA), Advanced Micro Devices (AMD), OpenAI, TikTok, and xAI. It has already signed more than $29 billion in contracts using new financing models involving customer-funded infrastructure and bring-your-own-hardware arrangements. This strategy reduces the capital burden on the company while it is scaling rapidly. The company ended the quarter with $38.5 billion in cash, cash equivalents and marketable securities.

From Legacy Giant to AI Contender

Oracle, once considered as a “tech dinosaur,” is now climbing to the top of the list of AI infrastructure plays. With nearly 50 years in the business, Oracle holds deep enterprise trust, massive data expertise, and relationships that span the global economy. In the AI era, these traits are incredibly powerful. Oracle’s transformation shows how quickly the tech industry changes and the ones who adapt to these changes, thrive here longer. Wall Street and investors seem to have picked up on that.

On Wall Street, of the 43 analysts covering the stock, 33 rate it a “Strong Buy,” one says it is a “Moderate Buy,” eight rate it a “Hold,” and one says it is a “Strong Sell.” The average target price for Oracle stock is $249.30, representing potential upside of 28% from its current levels. Many analysts have given the stock a high price estimate of $400, which suggests it has an upside potential of 106% over the next year.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Alphabet%20Inc_%20and%20Google%20logos%20by%20IgorGolovinov%20via%20Shutterstock.jpg)

/Technological%20process%20of%20soldering%20chip%20components%20on%20PCB%20board%20by%20I%20Viewfinder%20via%20Adobe%20Stock.jpeg)