/Green%20hydrogen%20by%20Scharfsinn%20via%20Shutterstock.jpg)

Plug Power (PLUG) is staging a grand recovery, which has made investors optimistic about its prospects. The stock has been up 101% this year, as top-line expansion and margin recovery have become central to its story. This has been a remarkable turnaround for a company that faces multiple class-action lawsuits over Department of Energy loan funding and major hydrogen facility projects.

After recording solid results in Q1, Plug Power is now focusing on the expansion of its electrolyzer projects. It is launching a 25-megawatt project with Iberdrola and BP in Spain and completing installation work on a 100-megawatt project with Galp in Portugal. However, large electrolyzer projects are expected to be complex endeavors, with the risk of delays in approvals.

Company’s CFO Paul Middleton essentially stated that there’s more growth to come. He believes that Plug Power has reached an “inflection point” on margins. Middleton also holds that second-quarter revenue is expected to increase sequentially from the first quarter. However, the growth might be modest. And gross margin rates are expected to improve quarter-over-quarter.

The company is eyeing full-year sales growth of 13% to 15%, with the first half accounting for roughly 40% of full-year revenue. The target is to remain disciplined, with projections of positive operating income in 2027 and full profitability in 2028.

We take a deeper look at Plug Power at this juncture.

About Plug Power Stock

Headquartered in Slingerlands, New York, Plug Power leads the green hydrogen revolution by building an end-to-end ecosystem for hydrogen production, storage, delivery, and energy generation. The company develops hydrogen fuel cell and electrolyzer systems that power material handling equipment, e-mobility, power generation, and industrial applications, replacing traditional batteries with zero-carbon solutions. It has a market capitalization of $5.52 billion.

Plug Power’s earnings beat and margin improvements have led to its stock surging. Moreover, rising AI-driven data center energy demands position PLUG's hydrogen solutions for backup and primary power, sparking optimism.

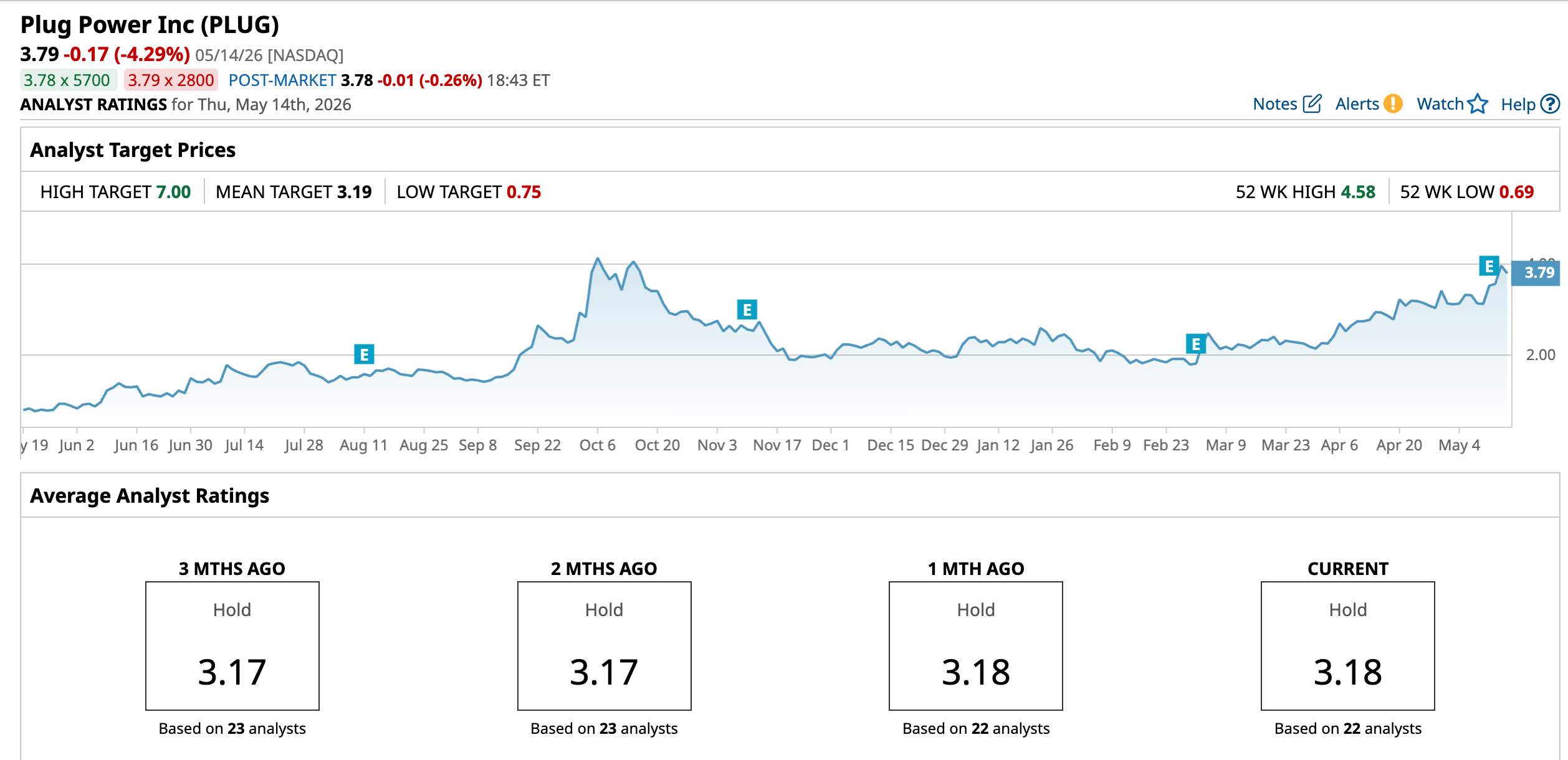

Over the past 52 weeks, PLUG’s stock has gained 382.62%, while it has been up 92.39% year-to-date (YTD). Just for comparison, the broader S&P 500 Index ($SPX) has increased 27.3% over the past 52 weeks and 9.58% YTD. It reached a 52-week high of $4.58 in October 2025, but is down 17.25% from that level.

Plug Power’s 14-day RSI of 67 indicates that the stock is in the overbought territory. Its forward-adjusted price-to-sales ratio of 6.80 times is significantly higher than the industry average of 1.83 times.

Plug Power Delivers Q1 Earnings Beat with Solid Margin Gains

On the backs of a solid commercial execution, Plug Power showed steady signs of improvement in the first quarter of fiscal 2026. The company’s net revenue increased 22.3% year-over-year (YOY) to $163.51 million, exceeding the $142.50 million that Wall Street analysts had expected. The top line was increased by sales of equipment, related infrastructure, and other items, which rose 24.4% YOY to $79.02 million.

The gains in the quarter were largely driven by growth across material handling and electrolyzer businesses. Plug Power’s hydrogen fuel sales increased by 22% YOY, while the hydrogen fuel margin rate improved by 54 percentage points due to greater leverage on Plug’s hydrogen network with higher volumes, reduced third-party sourcing costs, and efforts to improve network efficiency.

The big story during the quarter has obviously been the margin expansion. Plug Power still posted a loss, but it was significantly reduced. Its adjusted net loss per share decreased from $0.17 in Q1 2025 to $0.08 in Q1 2026. Plug Power exited the quarter with $802.01 million in cash, cash equivalents, and restricted cash, down from the $1.08 billion recorded a year earlier.

Wall Street analysts are optimistic about Plug Power’s ability to reduce its bottom-line losses. For the current year, the company is expected to reduce its loss by 48.4% YOY to $0.32 per diluted share, and improve further 53.1% to $0.15 in the next fiscal year. Analysts expect it to report a loss per share of $0.08 for the current quarter, down 50% YOY.

Here’s What Analysts Think About Plug Power’s Stock

Post Plug Power’s Q1 results, Wall Street analysts have reiterated their stances on the stock. Canaccord Genuity analysts raised the stock’s price target from $2.50 to $4, while maintaining a “Hold” rating. Analysts cited operational progress at PLUG, driven by restructuring under its Project Quantum Leap, which includes cutting operating costs, using less labor for servicing due to durable products, and improving fuel margins by optimizing distribution of its own and third-party hydrogen.

BMO Capital maintained an “Underperform,” while raising the price target from $1 to $1.20. While the firm’s analysts acknowledged the company’s improved topline growth and margin recovery, they also noted that its cash burn was steeper than expected in Q1. The analyst also noted Plug Power's unrestricted cash balance leaves minimal margin for error. On the other hand, B.Riley kept a “Buy” rating and raised the price target from $3 to $5. Analysts at the firm also raised its 2026 and 2027 revenue and EBITDA estimates.

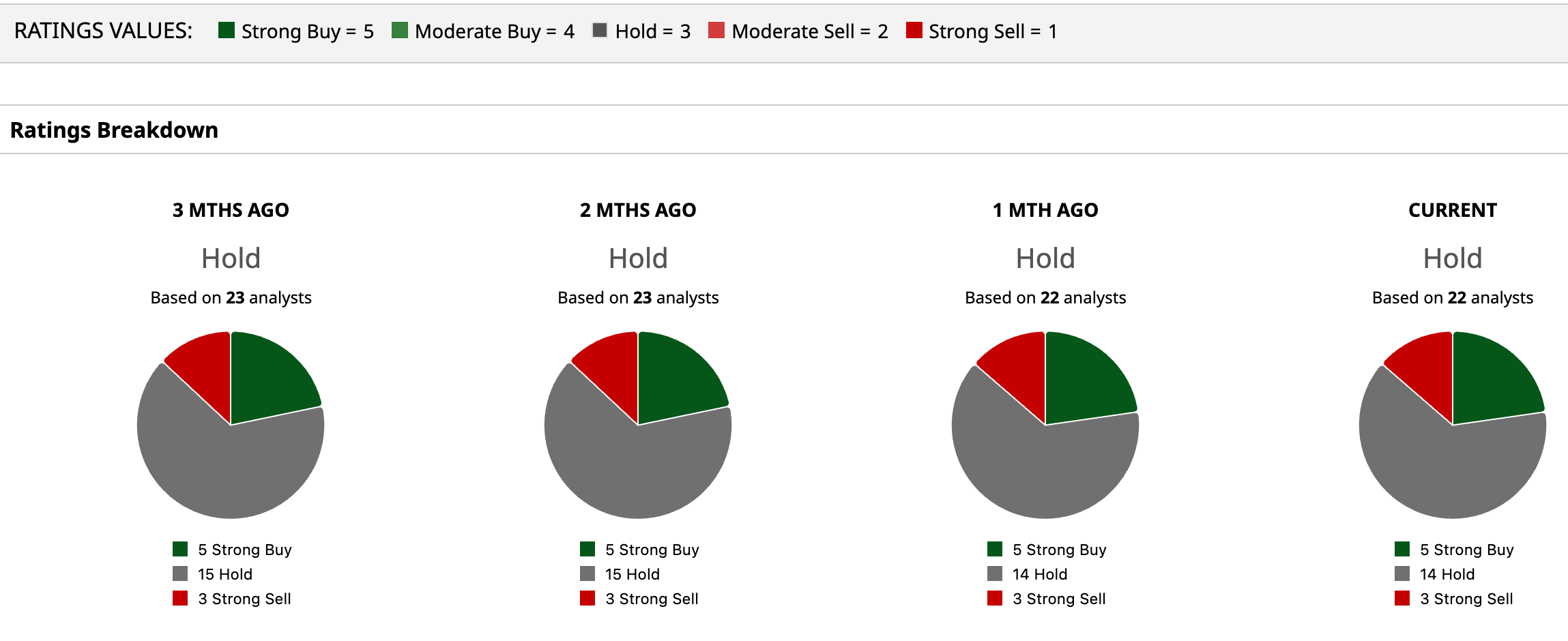

Wall Street analysts are taking a cautious stance on Plug Power’s stock, with a consensus “Hold” rating. Of the 22 analysts rating the stock, five analysts gave a “Strong Buy,” 14 a “Hold,” and three a “Strong Sell.” The consensus price target of $3.19 represents a 15.8% downside from current levels. However, the Street-high price target of $7 indicates a 84.7% upside from current levels.

On the date of publication, Anushka Dutta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/An%20image%20of%20the%20Snowflake%20logo%20on%20a%20corporate%20office_%20Image%20by%20Grand%20Warszawski%20via%20Shutterstock_.jpg)

/Netflix%20on%20tv%20with%20remote%20by%20freestocks%20via%20Unsplash.jpg)