With a market cap of $56.5 billion, Targa Resources Corp. (TRGP) is one of the largest independent midstream energy infrastructure companies in the United States, focused primarily on gathering, processing, transporting, storing, and exporting natural gas and natural gas liquids (NGLs). The Houston, Texas-based company plays a critical role in the North American energy value chain by moving hydrocarbons from production basins to industrial, petrochemical, export, and end-market customers.

Shares of the company have outpaced the broader market over the past 52 weeks. TRGP stock has climbed 58.7% over this time frame, while the broader S&P 500 Index ($SPX) has rallied 27.3%. However, shares of the company are up 45% on a YTD basis, outpacing SPX's 9.6% gain.

Looking closer, TRGP stock has also outperformed the State Street Energy Select Sector SPDR ETF's (XLE) 36.2% returns over the past 52 weeks and 29.8% YTD rally.

On May 7, Targa Resources shares soared 1.2% after the company released its Q1 2026 earnings. While its total revenue dipped 10.2% year over year to $4.09 billion, net income attributable to common shareholders rose 139.8% to $479.60 million. Its adjusted EBITDA surged 19% year over year to $1.40 billion. The company continued benefiting from resilient producer activity in the Permian despite temporary disruptions from severe winter weather and weak Waha natural gas prices earlier in the quarter.

Following the strong quarter, Targa raised its full-year FY2026 adjusted EBITDA guidance to a range of $5.7 billion to $5.9 billion, up from its prior outlook of $5.4 billion to $5.6 billion.

For the fiscal year ending in December 2026, analysts expect TRGP's EPS to surge 25.6% year over year to $10.66. The company's earnings surprise history is mixed. It beat the consensus estimates in two of the last four quarters while missing on two other occasions.

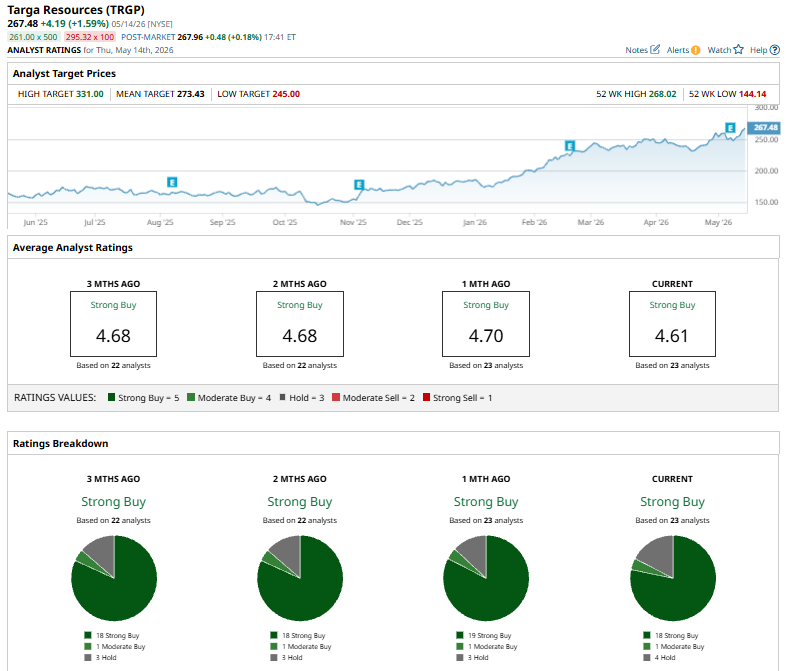

Among the 23 analysts covering the stock, the consensus rating is a “Strong Buy.” That’s based on 18 “Strong Buy” ratings, one “Moderate Buy,” and four “Holds.”

The configuration is bearish than a month ago, when the stock had 19 “Strong Buy” suggestions.

On May 14, Barclays analyst Theresa Chen reiterated an “Overweight” rating on Targa Resources and raised the price target to $262 from $255.

The mean price target of $273.43 implies an upswing potential of 2.2% from the current market prices. The Street-high price target of $331 implies a potential upside of 23.7% from the current price levels.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/An%20image%20of%20the%20Snowflake%20logo%20on%20a%20corporate%20office_%20Image%20by%20Grand%20Warszawski%20via%20Shutterstock_.jpg)

/Netflix%20on%20tv%20with%20remote%20by%20freestocks%20via%20Unsplash.jpg)