/Tesla%20Inc%20logo%20by-%20baileystock%20via%20iStock(1).jpg)

Tesla (TSLA) cheerleaders are not hard to find. Some investors are enamored by maverick CEO Elon Musk, while others find the spaces that Tesla dabbles in — like energy and autonomous driving — to be exciting. However, alongside Wedbush analyst Dan Ives, Ark Invest founder Cathie Wood stands out with her optimism about the company.

In a recent interview, Wood primarily singled out SpaceX for how its initial public offering (IPO) will unlock value for shareholders as well as offer a new way to play the Musk trade. However, Wood also argued that Tesla Robotaxi will eventually come out as the winner against rival Waymo, which is backed by Alphabet (GOOGL).

What Does Cathie Wood Think About Tesla Robotaxi?

Wood's rationale goes like this: “Vertical integration for Tesla means it will have the lowest cost structure by far." According to analysts, with scale, Tesla will be able to bring its cost-per-mile to less than $0.25, compared to more than $3 for the likes of Uber (UBER).

Despite Wood and her team's assertions, though, Tesla Robotaxi is still behind at the moment. For instance, a recent analysis revealed that out of 94,348 rides, the average wait time for a Tesla Robotaxi hit 15 minutes compared to Waymo's wait of less than six minutes. Further, robotaxis from Tesla took suboptimal routes, resulting in longer trip times.

Then there is rising competition in China. While Tesla launched its robotaxis commercially in June 2025, Baidu's (BIDU) Apollo Go robotaxi had completed over 11 million rides by May 2025 — narrowly surpassing Waymo's 10 million rides — and delivered 1.4 million rides in just the first quarter of 2025 alone, a 75% year-over-year (YOY) increase. Additionally, Chinese players like WeRide (WRD) and Pony.ai (PONY) are also expanding internationally, backed by government support, sovereign wealth funds, and partnerships with global platforms like Uber. That means Tesla's competitive window in international markets may be narrower.

However, Tesla is aiming for improvements rather than staying still. During the Q1 2026 earnings call, Musk unveiled plans for an AI4 Plus self-driving upgrade that doubles RAM to 32 gigabytes, bringing total system memory to 64 gigabytes. The CEO also confirmed that Cybercab production had begun at Gigafactory Texas.

On the software side, Tesla is running two distinct development branches, with the Robotaxi fleet in Austin operating on a more advanced build than what public Full Self-Driving (FSD) customers receive. Musk has outlined plans to merge the Robotaxi and supervised FSD software stacks into a single, unified build.

Financials Looking for a Trigger

Tesla wrapped up Q1 2026 with results that cleared Wall Street's expectations on both the top and bottom lines, even as the broader set of operating metrics painted a picture of Tesla still working through a demanding period.

Total revenue for the quarter reached $22.4 billion, up 16% YOY. Automotive revenue matched that pace, coming in at $16.2 billion, up 16% YOY. On the earnings front, Tesla posted EPS of $0.41, a 52% improvement over the prior-year period and a step ahead of the $0.35 consensus estimate. That result extended Tesla's streak of consecutive earnings beats to two quarters.

The profitability picture showed meaningful improvement as well. Gross margins expanded to 21.1% from 16.3% in the comparable period a year earlier, while operating cash flow surged 83% to $3.9 billion. The company closed the quarter with a cash position of $44.7 billion, a balance that sits comfortably ahead of its short-term debt obligations.

That said, the results grew more complicated on the volume side of the business. Vehicle production for the quarter totaled 408,386 units, a 13% gain on an annual basis. Deliveries rose 6% YOY to 358,023 vehicles. However, both deliveries and production fell sequentially as softness extended from Q4, reflecting a demand environment that has been partially hollowed out by an earlier wave of purchases pulled forward ahead of the federal electric vehicle (EV) tax credit expiration.

Several pockets of the business still offered a more encouraging read. Active FSD subscriptions expanded 51% YOY to 1.28 million. While Tesla's energy division moved in the opposite direction, with revenue declining 12% YOY to $2.41 billion, the company continued to build out its charging infrastructure. The Supercharger network grew 19% to 8,463 stations in Q1 while the total connector count also rose 19% to 79,918.

Valuation remains a defining feature of the Tesla investment debate. TSLA stock trades at a forward price-to-earnings (P/E) multiple of 361 times, a figure that dwarfs the sector median by a considerable margin. The forward price-to-sales (P/S) ratio of 17.6 times and the price-to-cash flow multiple of 167 times tell a similar story when placed alongside their respective sector medians.

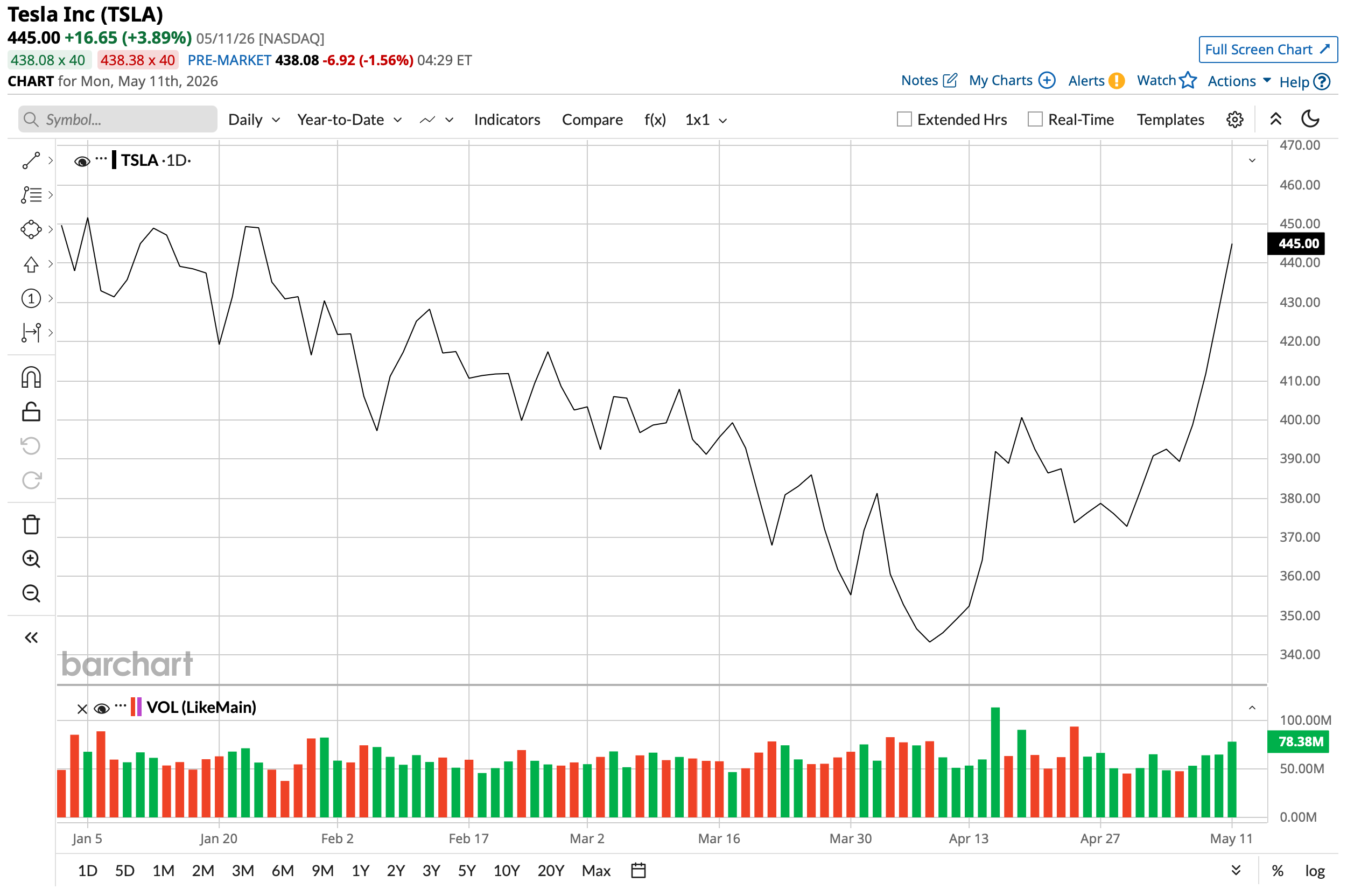

TSLA stock is down by less than 1% on a year-to-date (YTD) basis, and up 34% over the past 52 weeks.

What Do Analysts Think of TSLA Stock?

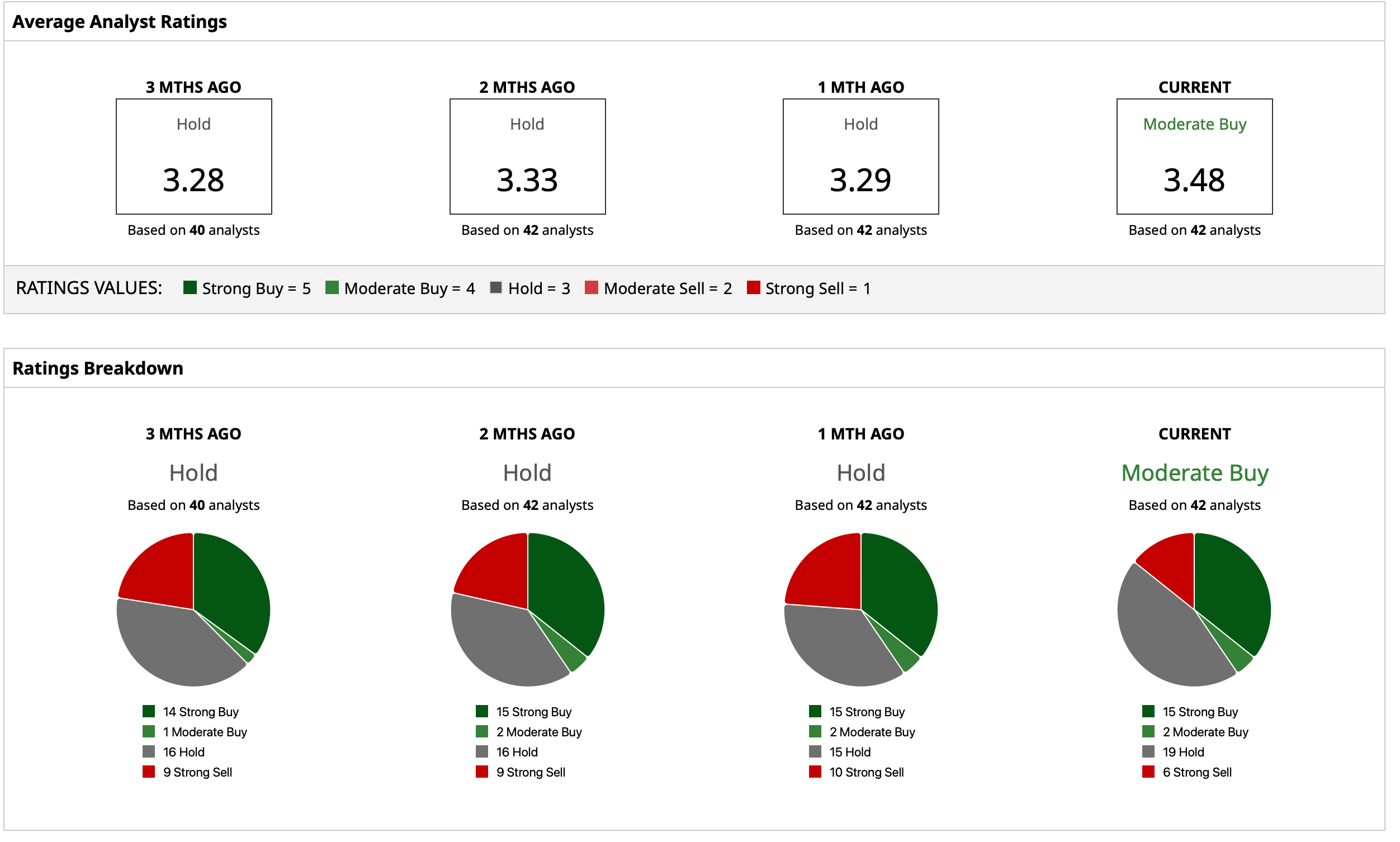

Overall, analysts rate TSLA stock as a consensus “Moderate Buy,” which is up from a consensus “Hold" rating just one month ago. The average target price of $410.94 has already been surpassed by shares, denoting potential downside of about 8% from current levels. However, the high price target of $600 suggests shares could rise as much as 34% from here. Out of 42 analysts covering TSLA stock, 15 have a “Strong Buy” rating, two have a “Moderate Buy” rating, 19 have a “Hold” rating, and six have a “Strong Sell” rating.

On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/A%20close-up%20of%20an%20AMD%20office%20by%20gehapromo%20via%20Adobe%20Stock.jpeg)