/Aflac%20Inc_%20sign-%20by%20yu_photo%20via%20Shutterstock.jpg)

Aflac Incorporated (AFL), headquartered in Columbus, Georgia, provides supplemental health and life insurance products. Valued at $58.8 billion by market cap, the company’s products include accident and disability, cancer expense, short-term disability, sickness and hospital indemnity, hospital intensive care, and fixed-benefit dental plans.

Shares of this largest provider of supplemental insurance have underperformed the broader market over the past year. AFL has gained 9% over this time frame, while the broader S&P 500 Index ($SPX) has rallied nearly 31%. In 2026, AFL stock is up 4.7%, compared to the SPX’s 8.3% rise on a YTD basis.

Narrowing the focus, AFL’s outperformance is apparent compared to iShares U.S. Insurance ETF (IAK). The exchange-traded fund has declined about 3.2% over the past year. Moreover, AFL’s gains on a YTD basis outshine the ETF’s 4.1% losses over the same time frame.

Aflac’s underperformance came from weak earned premiums in Japan, where 25.5% sales growth in new medical/cancer products was offset by higher lapses and reinsurance headwinds. Management sees Japan’s new reinsurance deal as a long-term growth platform, but near-term results hinge on converting strong sales into premium growth while managing persistency.

On Apr. 29, AFL shares closed down slightly after reporting its Q1 results. Its adjusted EPS of $1.75 fell short of Wall Street expectations of $1.80. The company’s revenue was $4.2 billion, missing analyst estimates of $4.3 billion.

For the current fiscal year, ending in December, analysts expect AFL’s EPS to decline 4.9% to $7.12 on a diluted basis. The company’s earnings surprise history is mixed. It beat the consensus estimate in two of the last four quarters while missing the forecast on two other occasions.

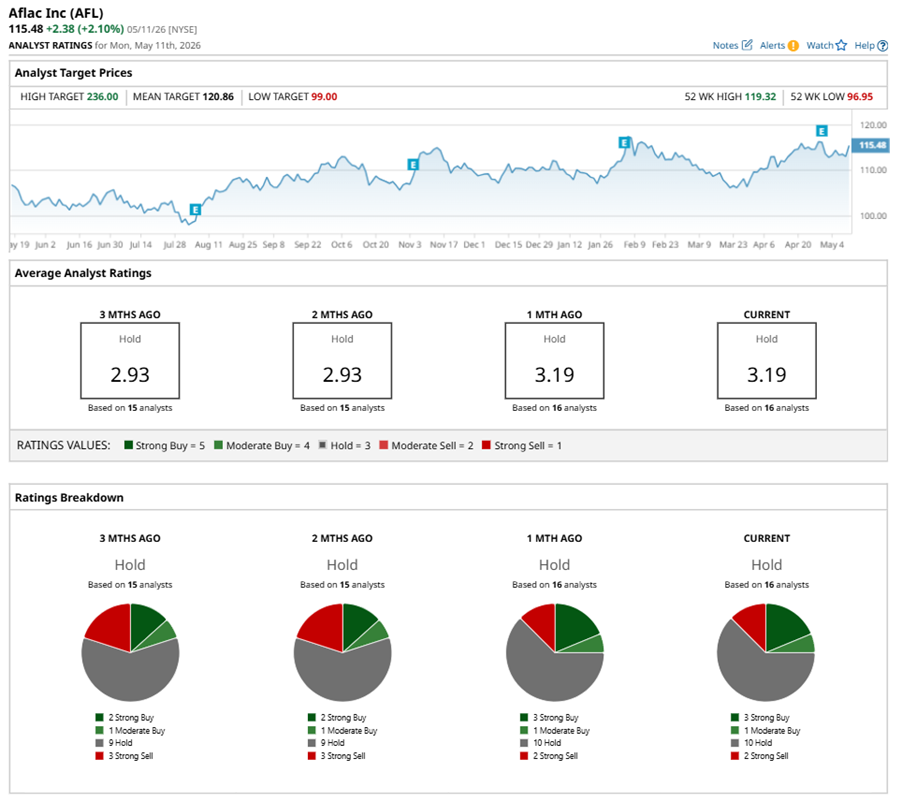

Among the 16 analysts covering AFL stock, the consensus is a “Hold.” That’s based on three “Strong Buy” ratings, one “Moderate Buy,” 10 “Holds,” and two “Strong Sells.”

This configuration is more bullish than two months ago, with two analysts suggesting a “Strong Buy,” and three analysts recommending a “Strong Sell.”

On May 4, Wells Fargo & Company (WFC) analyst Wesley Carmichael maintained a “Hold” rating on AFL and set a price target of $111.

The mean price target of $120.86 represents a 4.7% premium to AFL’s current price levels. The Street-high price target of $236 suggests an ambitious upside potential of 104.4%.

On the date of publication, Neha Panjwani did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/Ai%20chip%20by%20Quality%20Stock%20Arts%20via%20Shutterstock.jpg)

/A%20hand%20holding%20a%20phone%20with%20the%20Reddit%20logo_%20Mamun_Sheikh%20via%20Shutterstock_.jpg)

/Seagate%20sign%20on%20the%20building%20atits%20operational%20headquarters%20By%20JHVEPhoto.jpeg)

/Apple%20logo%20on%20store%20front%20by%20frantic00%20via%20iStock.jpg)