/McDonald's%20Corp%20arches%20by-%20TonyBaggett%20via%20iStock.jpg)

Burger chain Shake Shack (SHAK) endured a brutal week on Wall Street, as investors rushed for the exits following a disappointing fiscal 2026 first-quarter earnings report. Shares of the upscale burger chain cratered almost 28.3% on May 7 after the company missed Wall Street expectations on both revenue and earnings, sparking fresh concerns about slowing traffic, rising costs, and the broader health of the restaurant industry.

The quarter painted a troubling picture. Shake Shack swung to a loss of $290,000, a sharp deterioration from the $4.25 million profit it posted a year earlier. According to CEO Rob Lynch, the company faced a perfect storm of challenges during the quarter, including severe winter weather, elevated beef prices, and weaker tourism activity in key metropolitan markets like New York City, where many of its high-traffic locations rely heavily on visitors.

Meanwhile, ongoing tensions in the Middle East further pressured sales at the company’s licensed restaurants across the region. The ugly report sent shockwaves through the stock, but it also shifted investor attention toward industry leader McDonald's Corporation (MCD), which recently delivered stronger-than-expected first-quarter earnings despite operating in the same challenging environment. Against that backdrop, here’s a closer look at McDonald’s stock.

About McDonald's Stock

McDonald's Corporation is the world’s largest foodservice retailer, operating more than 40,000 restaurants across more than 100 countries. The company serves millions of customers with a menu centered around burgers, fries, and breakfast offerings, while iconic products such as the Big Mac and Happy Meal have become deeply associated with the brand worldwide.

Founded in 1940 by brothers Richard McDonald and Maurice McDonald, the business took on a much larger global presence after Ray Kroc joined the company in 1955 and spearheaded its international expansion. What started as a small drive-in restaurant in San Bernardino eventually evolved into one of America’s most recognizable consumer brands, now serving roughly 63 million customers every day around the world.

Although the company has transformed significantly over the past six decades, Ray Kroc’s original principles of Quality, Service, Cleanliness, and Value have remained central to McDonald’s operations and helped shape its reputation for more than 65 years. However, despite its massive global footprint, shares of McDonald's Corporation have struggled to gain momentum on Wall Street as the fast-food giant grapples with shifting consumer preferences toward healthier dining options, rising beef costs, and geopolitical pressures weighing on international sales, many of the same challenges currently impacting Shake Shack as well.

With a market capitalization of roughly $196 billion, McDonald's remains one of the biggest names in global fast food, but its stock performance has recently fallen far short of the broader market. Over the past 52 weeks, shares of the burger giant have tumbled 13.24%, sharply underperforming the broader S&P 500 Index ($SPX), which has surged an impressive 30.9% during the same period. The weakness has continued into 2026, with MCD stock down nearly 10.95% year-to-date (YTD), while the broader market has climbed 8.24% over the same stretch.

Although McDonald's stock has recently struggled to keep pace with the broader market, the fast-food chain continues to reinforce its reputation as one of Wall Street’s most reliable shareholder-friendly companies. As of early 2026, the fast-food giant is on the verge of earning the coveted Dividend King title, having raised its annual dividend for 49 consecutive years and already securing its place among the market’s elite Dividend Aristocrats. The company currently pays an annualized dividend of $7.26 per share, giving investors a solid yield of 2.63%.

Inside McDonald's Q1 Earnings Report

McDonald's reported its first quarter 2026 earnings on May 7, the same day as Shake Shack, but the results told two very different stories. While Shake Shack struggled under mounting industry pressure, McDonald’s delivered a quarter that largely topped Wall Street expectations, proving that its global scale and operational strength continue to set it apart in a challenging environment.

The fast-food giant generated consolidated revenue of $6.52 billion during the quarter, marking a 9.4% increase from the prior year and narrowly surpassing analyst expectations of $6.49 billion. The growth was supported by a 3.8% increase in global comparable sales, signaling that McDonald’s digital ecosystem, brand recognition, and massive international footprint continue to provide stability even as macroeconomic conditions remain uncertain. McDonald’s also impressed with its profitability.

Adjusted earnings came in at $2.83 per share, up 6% year-over-year (YOY) and ahead of the Street’s consensus estimate of $2.74 per share. Net income climbed 6% to $1.98 billion despite the company absorbing restructuring costs tied to its “Accelerating the Organization” initiative. Even more notably, McDonald’s maintained an adjusted operating margin of 46%, one of the strongest margins in the fast-food industry, despite continued pressure from rising labor and beef costs. The company generated more than $3.6 billion in restaurant margins during the quarter, reinforcing the durability and efficiency of its business model.

The company’s U.S. operations remained a key pillar of strength, with comparable sales rising 3.9% during the quarter. At the same time, McDonald’s digital and loyalty ecosystem continued to gain momentum, with sales from loyalty members surpassing $9 billion across 70 international markets. And, international operations delivered steady momentum, with the International Operated Markets segment matching the U.S. comparable sales growth rate of 3.9%.

Management noted that results were primarily driven by particularly strong performances in the U.K., Germany, and Australia. In the International Developmental Licensed Markets segment, comparable sales increased 3.4%, supported by continued strength in Japan, which management credited to strong local execution and sustained brand relevance. Looking further ahead, McDonald’s acknowledged that risks tied to higher cost inflation remain elevated due to ongoing global supply chain disruptions.

Still, the company emphasized that it plans to navigate the challenging environment by focusing on controllable factors, including consistent execution across value offerings, menu innovation, and marketing, while also leveraging the financial strength and scale of its global system. Management reiterated confidence in McDonald’s long-term expansion strategy, noting that the company still expects to reach roughly 50,000 restaurants globally by the end of 2027.

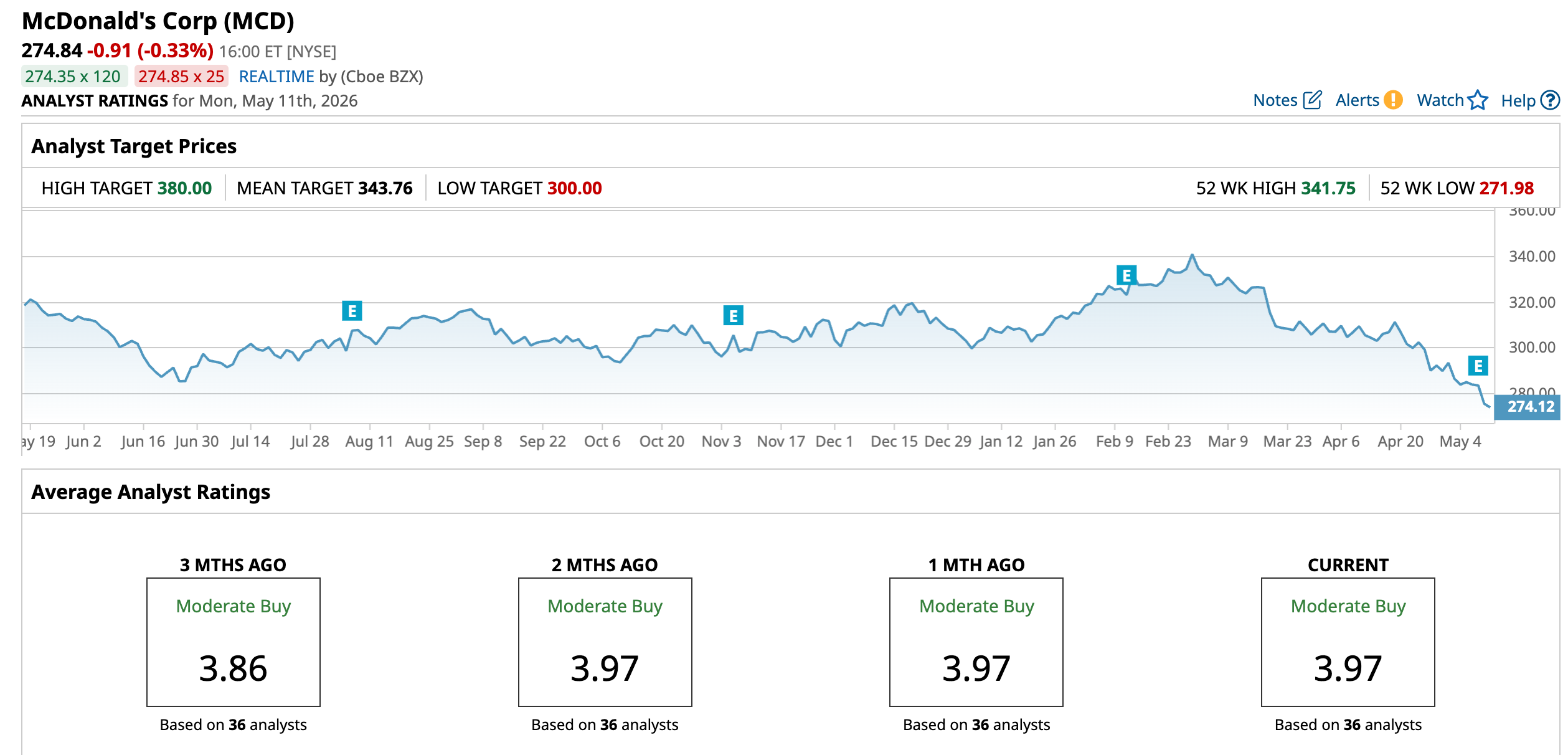

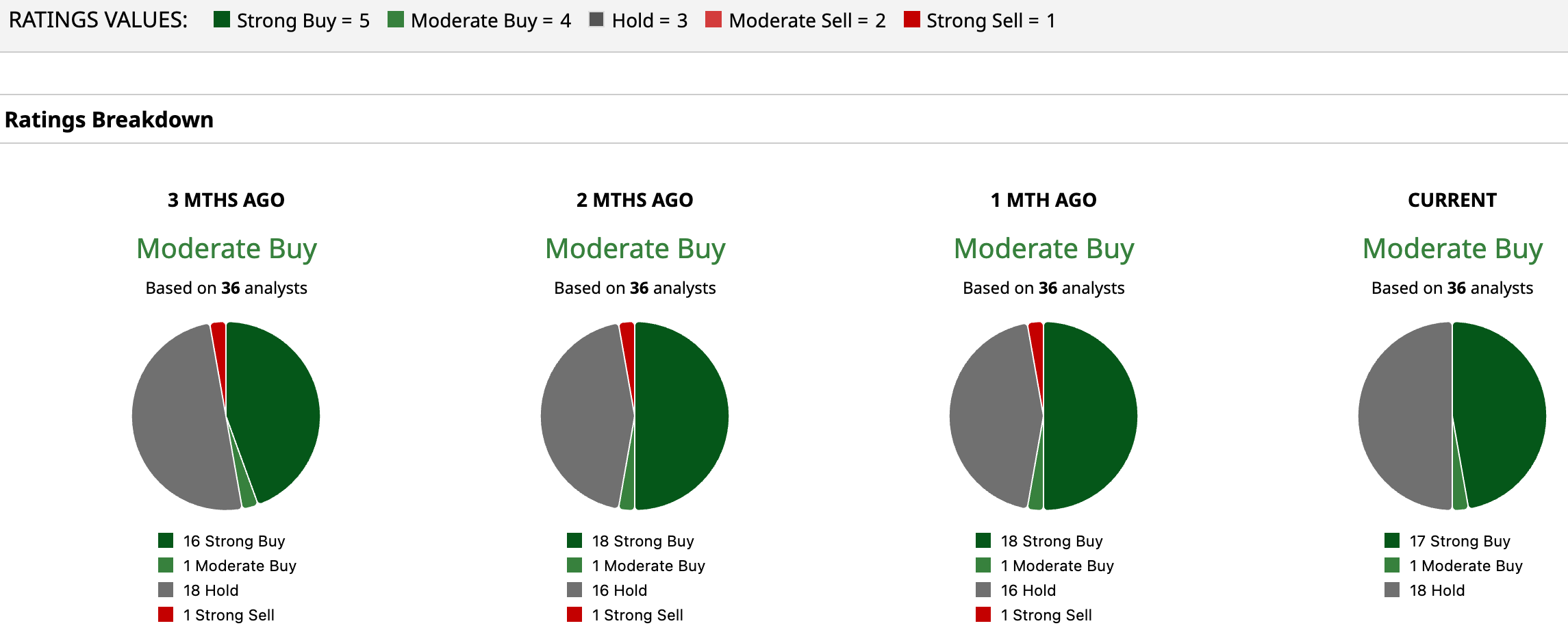

How Are Analysts Viewing McDonald's Stock?

Despite ongoing volatility across the restaurant industry, Wall Street continues to view McDonald's favorably, with the stock currently carrying a consensus “Moderate Buy” rating. Among the 36 analysts covering the fast-food giant, 17 recommend “Strong Buy,” one suggests “Moderate Buy,” while 18 remain on the sidelines with “Hold” ratings.

Analysts also see meaningful upside ahead. The average price target of $343.76 implies potential gains of roughly 25.1% from current levels, while the Street-high target of $380 suggests McDonald’s stock could rally as much as 38.3% in the months ahead.

On the date of publication, Anushka Mukherji did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/International%20Business%20Machines%20Corp_%20logo%20on%20phone-by%20rafapress%20via%20Shutterstock.jpg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)