/American%20Express%20Co_%20logo%20on%20building-by%20BalkansCat%20via%20Shutterstock.jpg)

With a market cap of $215.6 billion, American Express Company (AXP) is a global integrated payments company that provides credit and charge cards, banking, payment, and travel-related services to consumers, small businesses, and corporations across multiple international markets. It operates through four business segments, offering solutions such as merchant processing, fraud prevention, expense management, and digital payment services.

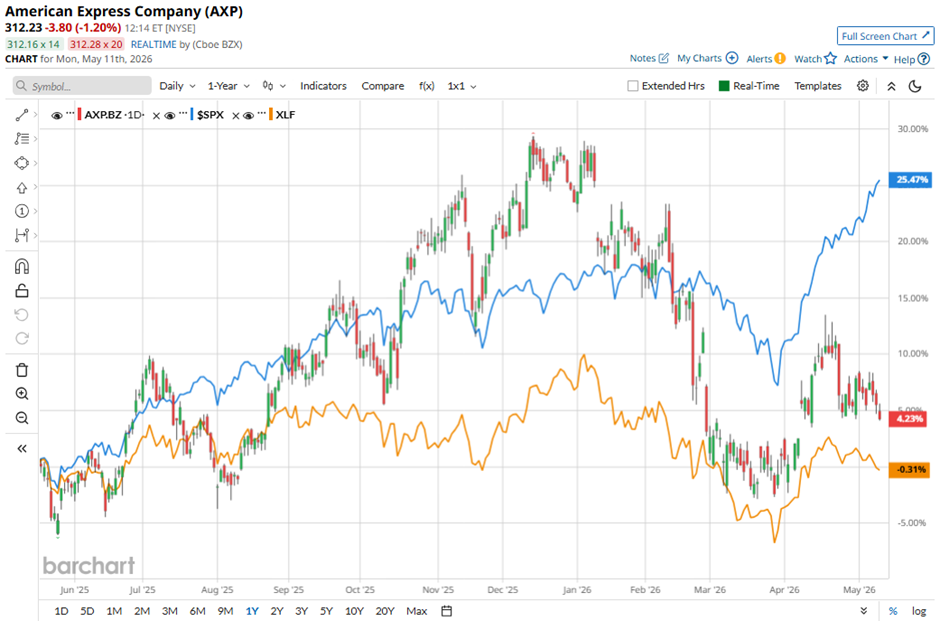

Shares of the credit card and payments company's shares have lagged behind the broader market over the past 52 weeks. AXP stock has increased 10.1% over this time frame, while the broader S&P 500 Index ($SPX) has rallied 31.2%. On a YTD basis, shares of the company are down 15.3%, compared to SPX’s 8.4% gain.

However, shares of the New York-based company have outpaced the State Street Financial Select Sector SPDR ETF’s (XLF) 2.6% return over the past 52 weeks.

Shares of American Express fell 4.3% on Apr. 23 as investors worried about rising costs despite strong Q1 2026 results, including plans for higher marketing, technology, and AI spending. Concerns also grew after U.S. consumer card additions declined to 1.3 million in Q4 2025 and Q1 2026 from about 1.5 million per quarter previously, while Card Member Service Expense surged 49% year-over-year due to expanded Platinum card benefits and higher customer usage. The decline came even though revenue rose 11% year-over-year to $18.91 billion and EPS increased 18% to $4.28, both beating analyst expectations.

For the fiscal year ending in December 2026, analysts expect AXP’s EPS to grow 14.4% year-over-year to $17.59. The company’s earnings surprise history is mixed. It beat the consensus estimates in three of the last four quarters while missing on another occasion.

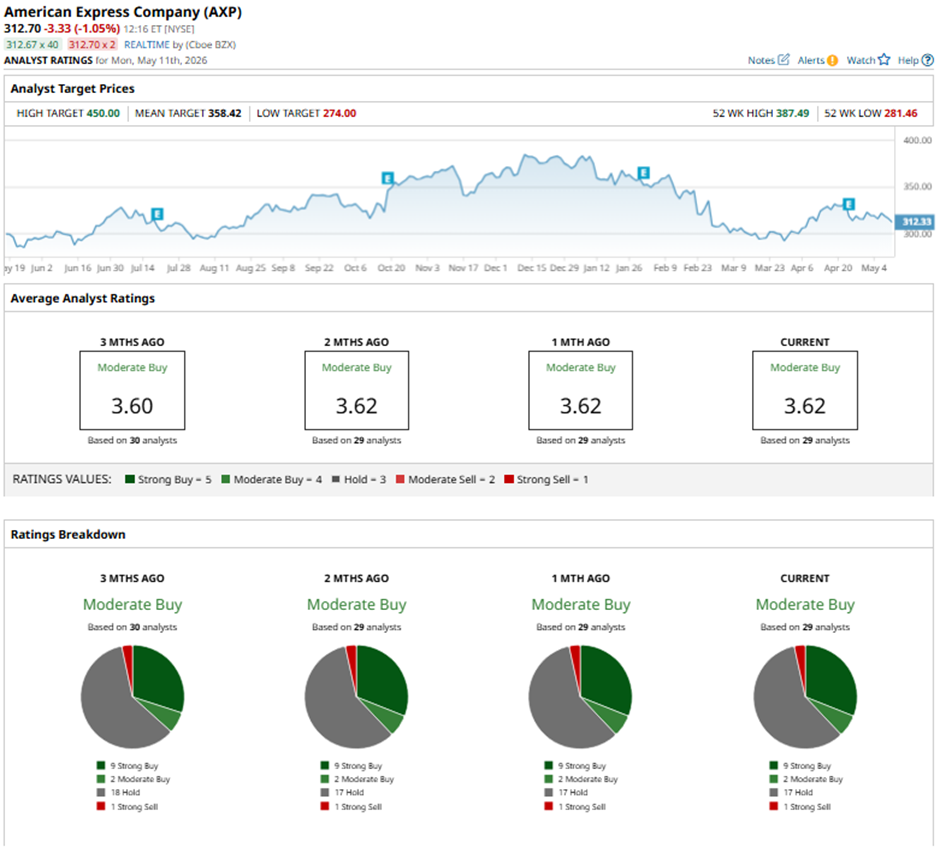

Among the 29 analysts covering the stock, the consensus rating is a “Moderate Buy.” That’s based on nine “Strong Buy” ratings, two “Moderate Buys,” 17 “Holds,” and one “Strong Sell.”

On Apr. 24, BofA raised its price target for American Express to $387 and maintained a “Buy” rating.

The mean price target of $358.42 represents a 14.6% premium to AXP’s current price levels. The Street-high price target of $450 suggests a 43.9% potential upside.

On the date of publication, Sohini Mondal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20close-up%20of%20a%20General%20Motors%20corporate%20sign%20by%20lindaparton%20via%20Adobe%20Stock.jpeg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Zoetis%20sign%20at%20their%20Canadian%20By%20JHVEPhoto.jpeg)

/Microsoft%20headquarters%20By%20Peter.jpeg)

/Space/Rocket%20takes%20off%20by%20Alones%20via%20Shutterstock.jpg)