Valued at a market cap of $63 billion, Baker Hughes Company (BKR) provides a portfolio of technologies and services to the energy and industrial value chain. The Houston, Texas-based company focuses on high-growth areas such as carbon capture, hydrogen production, and specialized power solutions for AI data centers, while simultaneously streamlining its operations through major divestitures.

This energy company has considerably outperformed the broader market over the past 52 weeks. Shares of BKR have rallied 76.6% over this time frame, while the broader S&P 500 Index ($SPX) has gained 30.4%. Moreover, on a YTD basis, the stock is up 40.6%, compared to SPX’s 7.9% rise.

Looking closer, BKR has also outpaced the State Street Energy Select Sector SPDR ETF's (XLE) 36.8% return over the past 52 weeks and 24.9% uptick on a YTD basis.

On Apr. 23, BKR posted stronger-than-expected Q1 results, and its shares surged 6.9% in the subsequent trading session. The company’s revenue grew 2.5% year-over-year to $6.6 billion, topping analyst expectations by 3.9%. Moreover, its adjusted EPS of $0.58 surpassed consensus estimates of $0.50. Management attributed the solid performance to strong operational execution despite ongoing disruptions in the Middle East, with robust momentum in the Industrial & Energy Technology (IET) segment offsetting regional headwinds.

For the current fiscal year, ending in December, analysts expect BKR’s EPS to decline 10.8% year over year to $2.32. The company’s earnings surprise history is promising. It topped the consensus estimates in each of the last four quarters.

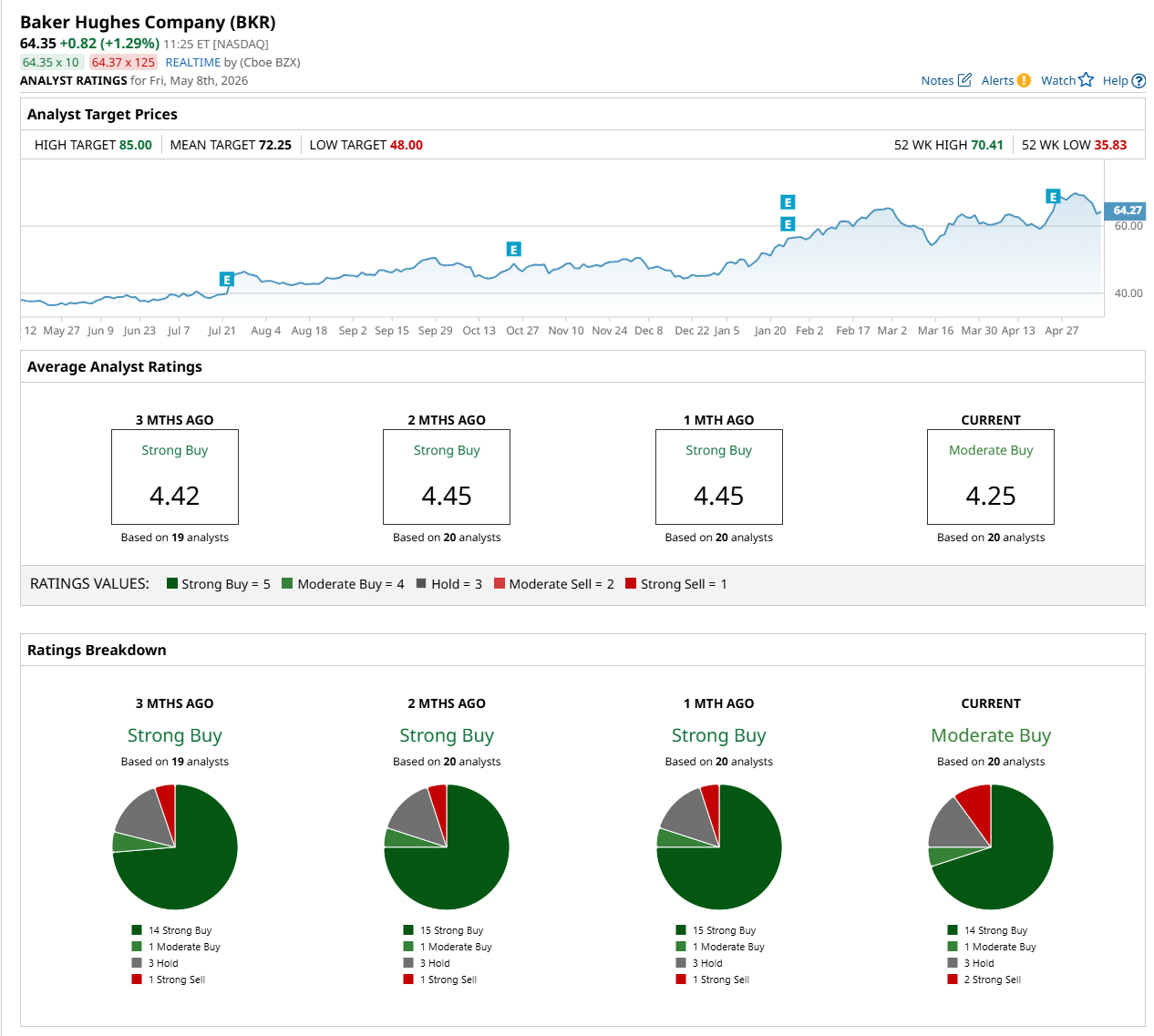

Among the 20 analysts covering the stock, the consensus rating is a "Moderate Buy,” which is based on 14 “Strong Buy,” one “Moderate Buy,” three "Hold,” and two “Strong Sell” ratings.

The configuration is less bullish than a month ago, with an overall “Strong Buy” rating, consisting of 15 analysts suggesting a “Strong Buy” and one recommending “Strong Sell.”

On Apr. 30, Argus Research analyst maintained a “Buy” rating on BKR and set a price target of $79, indicating a 22.8% potential upside from the current levels.

The mean price target of $72.25 suggests a 12.3% premium to its current levels, while its Street-high price target of $85 implies a 32.1% potential upside from the current price levels.

On the date of publication, Neharika Jain did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Semiconductor%20chip%20by%20Mykola%20Pokhodzhay%20via%20iStock.jpg)

/Lululemon%20Athletica%20inc_%20storefront%20by-%20Robert%20Way%20via%20iStock.jpg)