With a market capitalization of $18.7 billion, General Mills, Inc. (GIS) is one of the world’s largest packaged food companies, known for producing a wide range of cereals, snacks, baking products, yogurt, pet food, and frozen meals. The Minnesota-based company owns a portfolio of globally recognized brands, including Cheerios, Häagen-Dazs, Nature Valley, Pillsbury, Betty Crocker, and Blue Buffalo.

Shares of the company have lagged behind the broader market over the past year, declining 34.4% and 23.2% on a YTD basis. In comparison, the S&P 500 Index ($SPX) has returned 30.3% over the past year and risen 7.2% in 2026.

Narrowing the focus, GIS has underperformed the State Street Consumer Staples Select Sector SPDR ETF’s (XLP) 3.1% rise over the past 52 weeks and its 8.1% increase this year.

GIS has trailed the broader market over the past year due to weakening consumer demand, declining sales volumes, and margin pressure across its packaged food business. Inflation and tighter household budgets pushed many consumers toward cheaper private-label alternatives, hurting demand for branded cereals, snacks, and baking products. At the same time, shifting preferences toward fresher, higher-protein foods created additional headwinds for traditional packaged food companies.

For the fiscal year ending in May 2026, analysts expect GIS to report a 18.3% year-over-year decline in adjusted EPS to $3.44. The company has a mixed earnings surprise history. It has surpassed the Street’s bottom-line estimates in three of the past four quarters, while missing on another occasion.

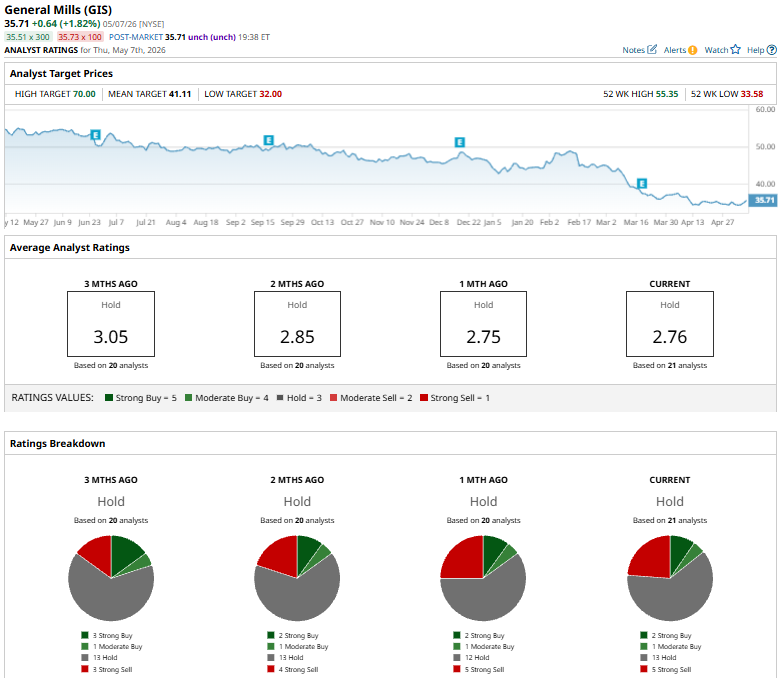

GIS has a consensus “Hold” rating overall. Of the 21 analysts covering the stock, opinions include two “Strong Buys,” one “Moderate Buy,” 13 “Holds,” and five “Strong Sells.”

The configuration is bearish than three months ago when the stock had three “Strong Buy” suggestions.

On Apr. 21, Stifel lowered its price target on GIS to $40 from $44 while maintaining a “Buy” rating. The firm cited weak sales volumes across key product categories and expectations for limited earnings growth in fiscal 2027. Stifel noted that despite the reduced target, General Mills trades at a significant discount to historical valuation levels, with relatively low EV/EBITDA and P/E multiples.

GIS’ mean price target of $41.11 indicates a 15.1% premium to the current market prices. Its Street-high target of $70 suggests a robust 96% upside potential from current price levels.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20close-up%20of%20a%20SpaceX%20sign%20by%20Sundry%20Photography%20via%20Adobe%20Stock.jpeg)

/Green%20hydrogen%20by%20Scharfsinn%20via%20Shutterstock.jpg)

/Abbvie%20Inc%20HQ%20photo-by%20vzphotos%20via%20iStock.jpg)