/MGM%20Resorts%20International%20lion%20by-%20atosan%20via%20iStock.jpg)

With a market cap of $9.2 billion, MGM Resorts International (MGM) is a global hospitality and entertainment company best known for operating luxury casino resorts, hotels, and live entertainment venues. Headquartered in Las Vegas, Nevada, MGM owns a portfolio of iconic properties concentrated on the Las Vegas Strip and in major regional and international gaming markets. Its flagship resorts include Bellagio, MGM Grand, ARIA Resort & Casino, The Cosmopolitan of Las Vegas, and Mandalay Bay Resort and Casino.

Shares of the company have lagged behind the broader market over the past 52 weeks. MGM stock has soared 21.6% over this time frame, while the broader S&P 500 Index ($SPX) has increased 31.4%. In addition, shares of the company are up 4.7% on a YTD basis, compared to SPX’s 7.6% rise.

Looking closer, shares of the casino and resort operator have outperformed the State Street Consumer Discretionary Select Sector SPDR ETF’s (XLY) 21.4% return over the past 52 weeks.

On Apr. 29, MGM Resorts reported its FY2026 Q1 earnings, and its shares declined 1.2%. It posted revenue of $4.45 billion, up 4.2% year over year, driven by strong growth in MGM China, digital operations, and BetMGM. Revenue from MGM China climbed 9%, while MGM Digital surged 43%, highlighting continued momentum in online betting and gaming. However, profitability came under pressure as adjusted EPS fell 40.8% year over year to $0.49 and adjusted EBITDA declined 8.9% to $590 million due to higher operating costs, weaker Las Vegas margins, and softer tourism demand.

For the fiscal year ending in December 2026, analysts expect MGM’s adjusted EPS to decrease 39.6% year over year to $2. The company's earnings surprise history is mixed. It beat the consensus estimates in two of the last four quarters while missing on two other occasions.

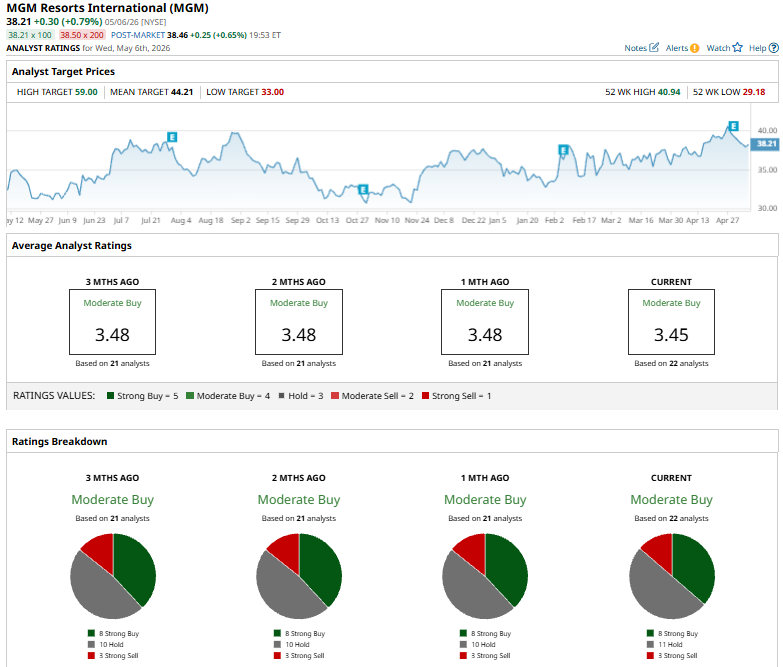

Among the 22 analysts covering the stock, the consensus rating is a “Moderate Buy.” That’s based on eight “Strong Buy” ratings, 11 “Holds,” and three “Strong Sells.”

On May 1, Jefferies downgraded MGM Resorts International from “Buy” to “Hold” and cut its price target to $44 from $50, citing concerns about the company’s business structure and limited long-term growth visibility. While the firm praised management’s execution, it flagged MGM’s operating and property company setup as a potential risk to sustainable earnings growth.

The mean price target of $44.21 represents a premium of 15.7% to MGM's current price. The Street-high price target of $59 suggests a 54.4% potential upside.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20corporate%20sign%20for%20SK%20Hynix%20by%20Tada%20Images%20via%20Adobe%20Stock.jpeg)

/Server%20racks%20by%20dotshock%20via%20Shutterstock.jpg)

/Netflix%20open%20on%20tablet%20by%20rswebsols%20via%20Pixabay.jpg)