/Accenture%20plc%20logo%20on%20devices-by%20Mojahid%20Mottakin%20via%20Shutterstock.jpg)

Artificial intelligence (AI) has been the predominant investing theme pretty much across the world. Investors are chasing stocks seen as winners in the AI arms race while ditching names that are either seen as AI losers or whose business models are being threatened by AI.

The traditional consulting and IT services are among the businesses that are at risk from the technology. With AI looking to automate coding and back-office tasks, the "man-hours" model that IT services firms rely on could be at risk. The flurry of AI tools released by Anthropic particularly compounded such fears and led to a selloff in software stocks.

Specifically, Accenture (ACN) has lost nearly a third of its market capitalization this year and trades at levels we last saw during the 2020 stock market lows. In my previous article, I had noted that ACN stock looks like a buy. However, the stock has gone south from those levels, lifting its dividend yield to an even fatter 3.6%. Let's explore whether Accenture is a good dividend stock to buy given the pessimism towards the industry in which it operates.

ACN has a Dividend Yield of 3.6%

Let’s begin by looking at Accenture’s dividend history. The company started paying a semi-annual dividend in 2005 but transitioned to quarterly dividends beginning in 2019. It has increased its payouts every year since its initiation, with an impressive annualized growth of 11.1%. Last year, the company raised its quarterly dividend by 10.1% to $1.63 per share.

To be sure, the dividend growth has slightly tapered down, and since moving to a quarterly payout in 2019, the annualized growth has been 10.7%. Accenture’s dividend growth has outpaced earnings growth in recent years, but the payout ratio of around 54% does not sound alarming yet. However, going forward, investors should expect a high single-digit annual growth, which would be in line with Accenture’s earnings growth.

Accenture’s current dividend yield is near its all-time high and thrice that of the S&P 500 Index ($SPX). Usually, high dividend yields are due to denominator issues, as a fall in stock price lifts the yield. However, in Accenture’s case, it is a combination of an increase in dividends and a decline in stock price.

Accenture Stock's Forecast

Meanwhile, while Accenture commands a decent dividend yield, we also need to look at the outlook for the stock because that’s where the bulk of the returns would come from, at least for a company like Accenture.

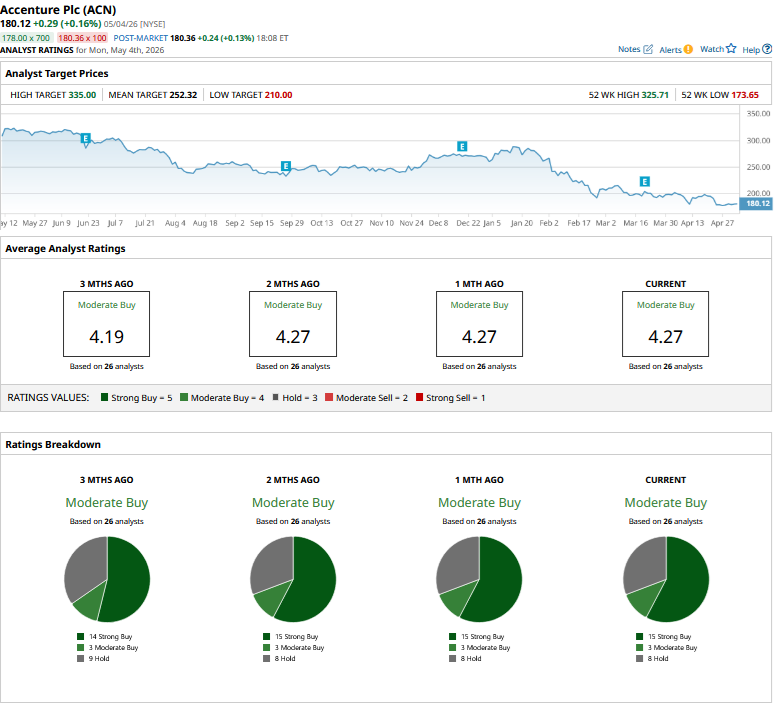

Analysts have set a mean target price of $252.32 for Accenture, which is around 40% higher than current levels. Here, it is worth noting that while ACN is rated as a consensus “Moderate Buy” by sell-side analysts, which is the same as what we had at the beginning of the year. However, many brokerages have lowered the stock’s target price this year.

Should You Buy ACN Stock?

Software and IT services companies could face some real headwinds from AI as models improve over time and put their very business model under a scanner. However, Accenture has been trying to make AI an opportunity rather than a threat. It is making acquisitions in the AI space, which help enhance its capabilities and increase its target market. Also, the company has been training its workforce in AI and has been pretty clear in its communication that those who cannot be reskilled will be laid off, while senior employees will lose out on promotion unless they use AI tools. In fiscal Q2 2026, it had 85,000 AI and data professionals, which was ahead of the 80,000 it was targeting for the entire fiscal year.

During the fiscal Q2 earnings call, CEO Julie Sweet said that Accenture plays a “critical role in the AI ecosystem.” She touted AI as a "tailwind" and said it is helping the firm increase its market share and create new growth opportunities.

Notably, companies adopting AI would also need consulting and professional services companies to implement these projects. Unlike consumer AI, where adoption can be instant and seamless, in enterprise AI, companies must consider several factors, including the safety of the massive data they handle and the long-term payoffs. This is where Accenture can fit in with its AI-trained workforce.

Finally, we need to look at the valuations. Accenture trades at a forward price-to-earnings (P/E) multiple of under 13x, which is significantly below the nearly 21x the average S&P 500 Index constituent trades at. I won’t compare ACN's multiples with historical averages, which are obviously much higher but are not truly representative given the changes in the business environment with the advent of AI.

However, I find ACN's risk-reward quite attractive here and added it to my portfolio, as I believe the worst is over for the stock, which seems to bake in a lot more pessimism than warranted.

On the date of publication, Mohit Oberoi had a position in: ACN. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Microsoft%20headquarters%20By%20Peter.jpeg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)