/AI%20(artificial%20intelligence)/Businessman%20touching%20the%20brain%20working%20of%20Artificial%20Intelligence%20(AI)%20Automation%20by%20Suttiphong%20Chandaeng%20via%20Shutterstock.jpg)

This earnings season has marked a turning point for artificial intelligence (AI) stocks. It is not just the big tech companies driving the market rally anymore. Even the smaller and lesser-known companies tied to the AI infrastructure are also reporting solid earnings and revenue growth. One company benefiting from this trend is Vertiv Holdings (VRT), which recently reported a strong start to fiscal 2026. VRT stock is now trading around its all-time high today and has surged an impressive 115% year-to-date (YTD). This sharp move isn’t just AI hype anymore but is backed by strong business performance and growing demand for the kind of infrastructure needed to support AI.

Should you join the rally?

The AI Buildout Is Accelerating Faster Than Expected

As AI workloads grow and data centers become more complex, they require better power, cooling, and infrastructure solutions. Vertiv provides these backup power systems, thermal (cooling) systems, and integrated setups to ensure that servers, particularly those used for AI, operate smoothly without overheating or shutting down. This has created immense demand for its products. In the Q1 earnings call, Vertiv’s leadership made it clear that something fundamental has changed in recent months. Customers are no longer experimenting with AI infrastructure; they are, in fact, adapting it at scale.

Organic growth stood at 23% year-over-year (YoY) in the first quarter of fiscal 2026, while total revenue increased by 30% to $2.6 billion. Usually, high growth comes at the expense of profitability, but that is not the case with Vertiv. Adjusted EPS increased 83% to $1.17, with an adjusted operating margin of 20.8%, reflecting how the company is balancing expansion and discipline. The company is investing aggressively in expanding manufacturing capacity, scaling service operations, and improving its engineering capabilities. These investments span everything from power systems to advanced cooling technologies, particularly liquid cooling, which is becoming essential for high-density AI workloads. Despite the expenditures, Vertiv managed to generate $653 million in free cash flow in the quarter.

Management is making sure that when supply becomes constrained, the company doesn’t become a bottleneck in a rapidly scaling market. Based on its expansion capacity and the high demand, Vertiv reinforced its full-year outlook. The company expects 51% YoY in adjusted EPS driven by a 34% increase in sales. The adjusted operating margin could be around 53%. It also projects generating free cash flow totaling $2.2 billion. Analysts expect Vertiv's earnings to increase by another 33.5% in 2027.

VRT Stock: Buy Now or Too Late?

Vertiv’s inclusion in the S&P 500 Index ($SPX) this year has also garnered a lot of attention by automatically putting the company on the radar of large institutional and passive investors. Being part of the index also signals to the market that Vertiv has reached a meaningful level of size, consistency, and financial strength expected of large-cap leaders. This also helps justify its premium valuation over time as the stock currently trades at 51x forward 2026 earnings. VRT is an excellent AI infrastructure stock to grab now. But risk-averse investors may prefer to wait for a more attractive entry point.

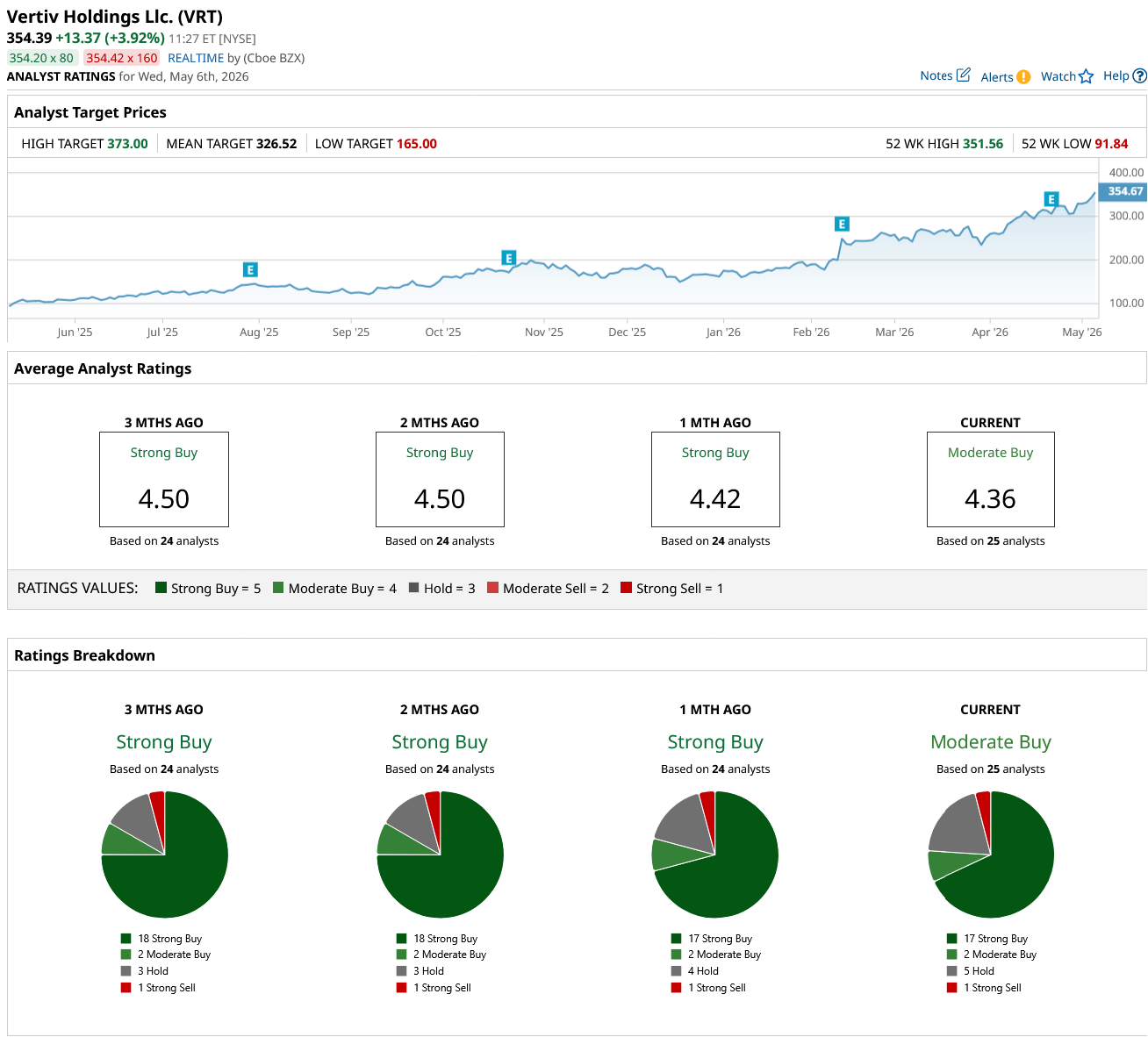

On Wall Street, VRT stock is an overall “Moderate Buy.” Of the 25 analysts covering the stock, 17 rate it as a "Strong Buy," two call it a "Moderate Buy," five recommend a “Hold,” and one has a “Strong Sell” rating. It currently sits above its average price target of $326.52. However, its high price estimate of $373 indicates a possible 5% rally over the next 12 months.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/Ai%20chip%20by%20Quality%20Stock%20Arts%20via%20Shutterstock.jpg)

/A%20hand%20holding%20a%20phone%20with%20the%20Reddit%20logo_%20Mamun_Sheikh%20via%20Shutterstock_.jpg)

/Seagate%20sign%20on%20the%20building%20atits%20operational%20headquarters%20By%20JHVEPhoto.jpeg)

/Apple%20logo%20on%20store%20front%20by%20frantic00%20via%20iStock.jpg)