/A%20game%20controller%20in%20front%20of%20a%20Roblox%20computer%20screen%20by%20Miguel%20Lagoa%20via%20Shutterstock.jpg)

Shares of user-generated gaming platform Roblox (RBLX) nosedived by more than 30% after the company revealed in its latest earnings call that its AI-enhanced child safety measures will lead to lower user engagement and revenues this year.

Explaining the rationale behind the move, CEO David Baszucki said, "We believe the strategic upside of everything we're doing is significant and the right thing to do for the long-term health of the platform."

Which is true, I reckon; however, there's more to the story as to why shares of Roblox are down 45% on a year-to-date (YTD) basis.

About Roblox

Founded in 2004, Roblox is like YouTube but for gaming. The company operates a user-generated gaming platform where users play and create games while monetizing their experiences. With over 100 million daily active users (DAUs), Roblox is one of the largest gaming/social platforms in the world.

Its market cap currently stands at $31.8 billion.

So, why then has Roblox been on such a downward spiral for some time now, and can it stage a turnaround? Let's find out.

Still Unprofitable

One of the issues working against Roblox is that even after more than two decades of its existence, the company has yet to report any profits. Q1 2026 was no different.

Revenues of $1.4 billion were up 39% from the previous year on the back of higher DAUs (132 million, +35% YoY) and hours engaged (31 billion, +43% YoY). Losses widened to $0.35 per share from $0.32 per share in the year-ago period. However, it came in narrower than the consensus estimate of a loss of $0.41 per share, the third consecutive quarter this has happened.

Now, if one observes some of the metrics sequentially, the weakness in the share price could be somewhat explained. While DAUs and hours engaged rose yearly, both witnessed sequential drops of 8.3% and 11.4%, respectively. Similar was the case with bookings, as they grew by 43% from the previous year to $1.7 billion, but declined by 22.1% quarterly.

Moreover, what spooked the investors more was the lowering of revenue guidance for the full year. The company now expects revenue to be in the range of $5.9 to $6.1 billion, down from its earlier outlook between $6.02 billion and $6.29 billion.

Having said that, net cash from operating activities increased by a hefty 41.7% to $629 million in Q1 2026. Overall, Roblox ended the first quarter with a cash balance of $1.2 billion, with no short-term debt on its books.

Is Roblox a Lost Cause Then?

Roblox remains immensely popular among the younger cohort. It just needs to find its path towards profitability before it scales even more. In fact, the recent slowdown in DAUs can actually be a blessing in disguise for the company to get its financial affairs in order.

Speaking of scale, what truly sets Roblox apart from conventional gaming companies is the sheer breadth of the content universe it has cultivated. A library spanning 14 million games serves a diverse and globally distributed user base, one that engages with the platform through real money purchases of Robux, the platform's internal currency. Those Robux are then spent on items within individual games, and with every transaction that flows through the system, Roblox takes its share before returning the remainder to the creators who built the experiences in the first place. Alongside this economic model, the platform carries another advantage that competitors have struggled to replicate, which is its ability to run smoothly on everyday handheld devices without demanding expensive hardware or dedicated gaming consoles.

That accessibility does not come at the expense of visual or gameplay quality, and the architecture responsible for maintaining that balance deserves recognition. Roblox developed what it calls its Scalable Lightweight Interactive Model, or SLIM, a system that generates multiple simplified and performance-optimized versions of any object or model within a developer's environment, storing them for retrieval at the moment they are needed. A user on a modest device receives a version of that object rendered to match what their hardware can handle comfortably, while someone on a more capable machine sees a fuller and more detailed representation. The result is a platform that does not force a trade between reach and experience, serving both ends of the hardware spectrum without penalizing either.

On the expansion front, Roblox entered into a collaboration with SEGA (SGAMY) that will bring the “Like a Dragon” universe into the platform as a licensed experience. This is part of a broader and more systematic approach to intellectual property partnerships, facilitated through a licensing manager that functions as a structured gateway connecting IP holders with the developers and creators who want to build within their established worlds. The infrastructure supporting this model already encompasses relationships with Lionsgate (LION), the largest independent film and television studio in the world, as well as Netflix (NFLX), with the framework in place to accommodate considerably more partnerships as interest grows.

Safety has also emerged as a genuine area of innovation rather than simply a compliance obligation. Roblox built and released as open source a tool called Sentinel, an AI-driven early warning system trained to identify subtle communication patterns associated with grooming behavior. In the first half of 2025 alone, Sentinel contributed to roughly 1,200 reports of potential child exploitation attempts filed with the National Center for Missing and Exploited Children. The company has since introduced real-time AI-powered chat rephrasing, a system that takes profanity and rewrites it to preserve the user's intended meaning rather than replacing it with a row of symbols, keeping conversations natural while maintaining moderation standards. Age verification through AI facial estimation has been made a requirement in a number of markets, with the system capable of estimating a user's age to within one or two years across the range of five to 25.

Overall, since the start of 2025, Roblox has brought more than 145 distinct safety innovations to the platform, a volume that reflects how seriously the company has chosen to treat this dimension of its operations.

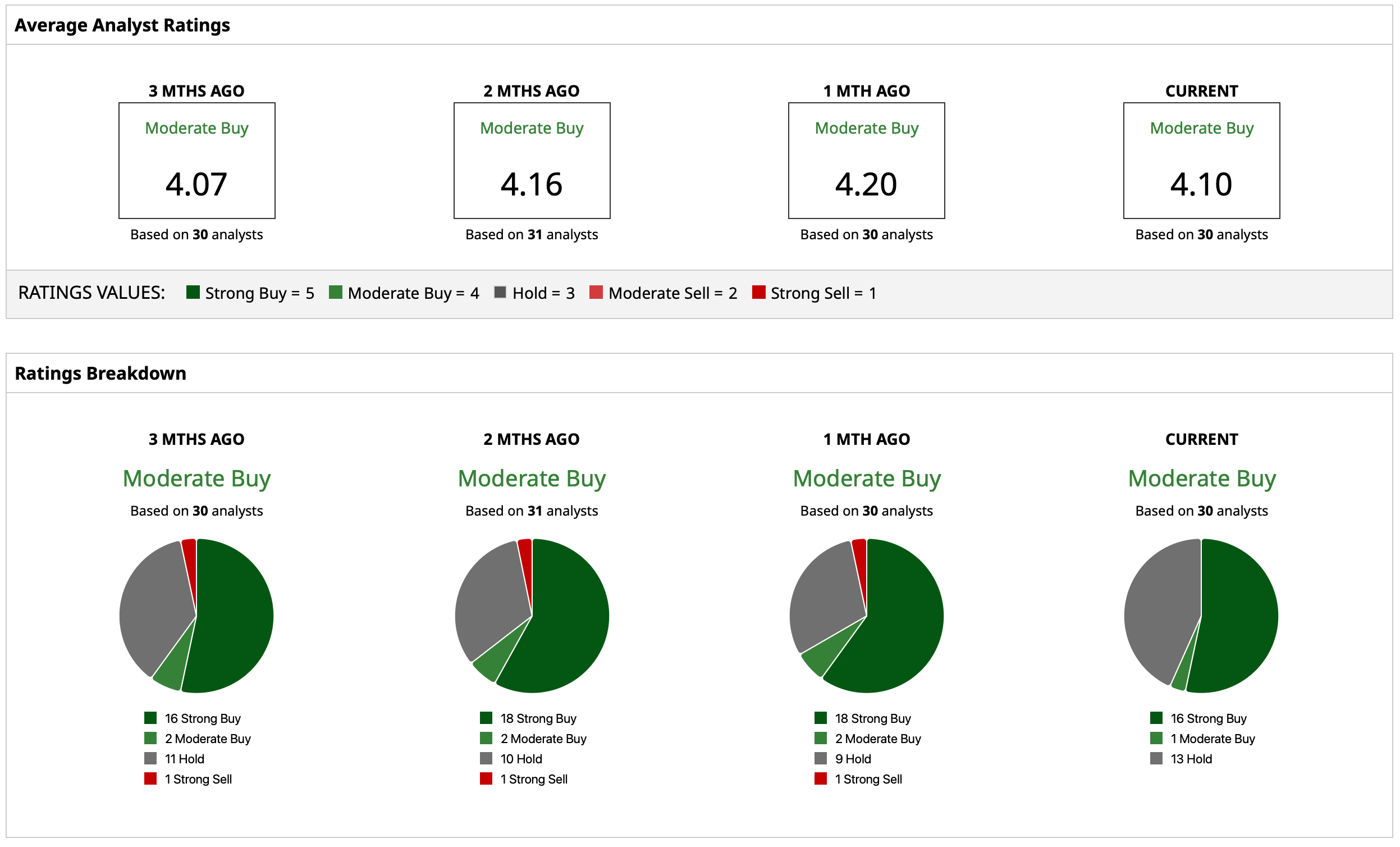

Analyst Opinion of RBLX Stock

Overall, analysts have deemed RBLX stock a “Moderate Buy,” with a mean target price of $82.58. This denotes an upside potential of about 86% from current levels. Out of 30 analysts covering the stock, 16 have a “Strong Buy” rating, one has a “Moderate Buy” rating, and 13 have a “Hold” rating.

On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Johnson%20%26%20Johnson%20location%20sign-by%20JHVEPhoto%20via%20iStock.jpg)

/AI%20(artificial%20intelligence)/AI%20technology%20-%20by%20Wanan%20Yossingkum%20via%20iStock.jpg)

/A%20close-up%20of%20an%20AMD%20office%20by%20gehapromo%20via%20Adobe%20Stock.jpeg)