/Intel%20Corp_%20badge%20holder-by%20hasrul_rais%20via%20Shutterstock.jpg)

After a long time, Intel (INTC) stole the limelight from Advanced Micro Devices (AMD), reminding old-timers of the good old days, when everything Intel did was considered the gold standard of computing. The company’s Q1 2026 earnings beat and impressive guidance have allowed investors to entertain the thought of the firm gaining back its lost glory. Just like in the past, AMD finds itself operating in the shadows of its main competitor, and it is quite likely the old pattern will repeat, giving Intel the advantage.

Since Intel’s earnings report, AMD and Intel stocks have both rallied. The unprecedented CPU demand has forced investors to buy first and ask questions later. This approach has worked for Intel shareholders but might backfire for AMD backers. HSBC just came out with its earnings preview and believes AMD’s 2026 server CPU upside, where it held an advantage over Intel, is capped due to capacity constraints. This could continue in 2027 as well. The firm therefore expects no earnings surprise and guidance in line with previous expectations on May 5.

Intel also announced today that it was bringing in two new experts to its management team. Alex Katouzian will join the company as vice president and GM of Client Computing & Physical AI. Pushkar Ranade is coming in as the Chief Technology Officer.

All this means investors might continue to favor Intel, backing the giant to regain its past glory and bring investors handsome rewards along the way.

About Intel Stock

Intel Corporation is a semiconductor company operating across the United States, Israel, Ireland, and other global markets. It is involved in the manufacturing, development, designing, marketing, and sale of computing and related end products and services. The company operates through the DCAI, CCG, and Intel Foundry segments. Its product portfolio consists of computing and semiconductor solutions, including GPUs, CPUs, data center, and AI products.

INTC stock has been on a tear lately, with gains of almost 200% so far this year alone. The stock’s incredible performance has helped spur a rally in the wider semiconductor sector, helping the iShares Semiconductor ETF (SOXX) register a 61% gain year-to-date (YTD).

Buying Intel at this stage isn’t a question of valuation. The company is on a recovery path, and every investor wants a piece of it. There are more pressing issues right now, including improving process yields and gaining customers. After all, just because there is CPU demand doesn’t automatically mean that every company will benefit. Intel will have to improve its wafer yield for the 18A (1.8nm) process, as it might be challenging to gain customers otherwise. It also has to improve its advanced packaging expertise, but investors would hope the new management already has a plan in place to achieve all of this. The stock doesn’t currently pay a dividend, but if things normalize, the old payouts could return.

Intel Starts 2026 Strong

Intel posted its Q1 fiscal 2026 results on April 23, beating both revenue and earnings estimates. Revenue for the quarter came in at $13.58 billion, exceeding analyst estimates by $1.15 billion. The company reported Non-GAAP earnings of $0.29 per share, surpassing market expectations by $0.28. Non-GAAP gross margin was 41%, supported by improved Intel 18A yields and inventory benefits.

Looking ahead, Intel forecasts second-quarter revenue to range between $13.8 billion and $14.8 billion compared to the consensus estimate of $13.06 billion. Non-GAAP EPS is projected at $0.20 compared to a consensus estimate of $0.08. At the midpoint of $14.3 billion, the company expects a non-GAAP gross margin of 39%. The company expects lower gross margins in the second quarter due to a higher mix of early-node producers.

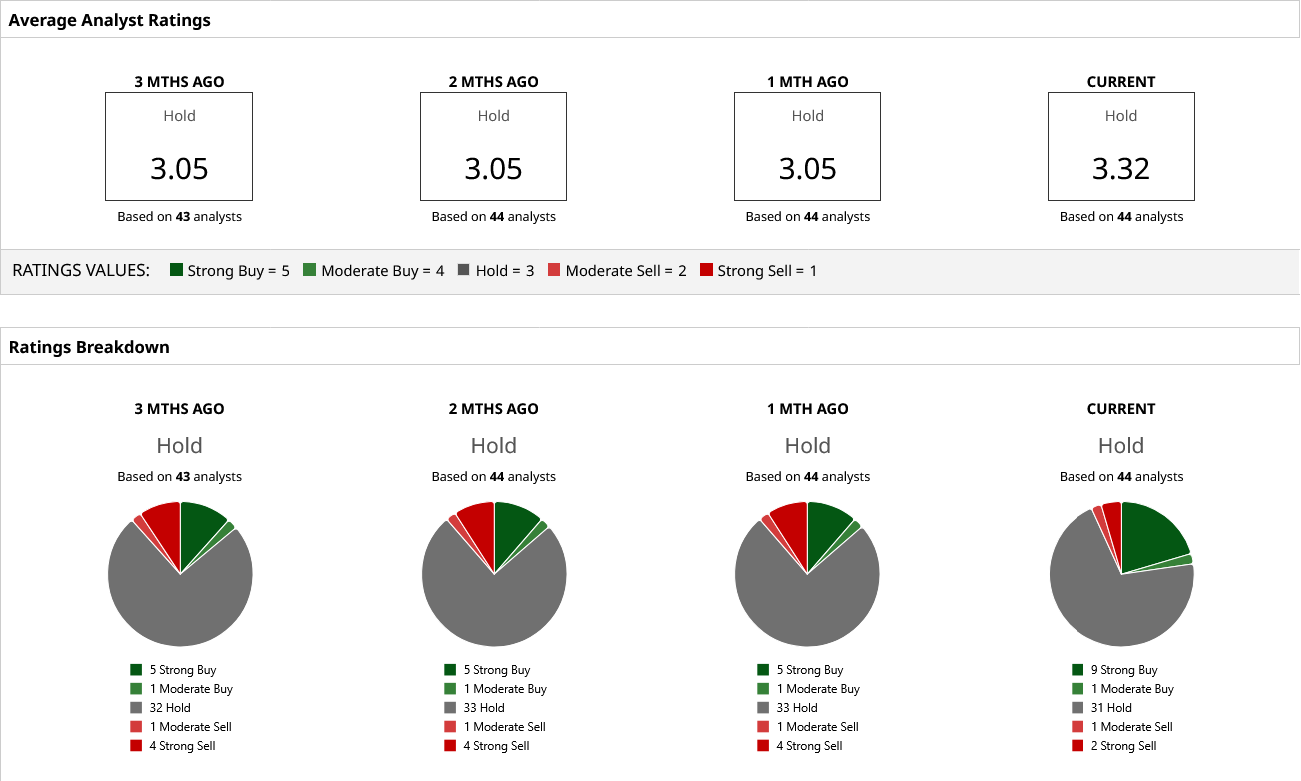

What Are Analysts Saying About INTC Stock?

After delivering better-than-expected first-quarter results, INTC stock received an upgrade from Roth MKM analyst Sujeeva De Silva. He upgraded the stock to “Buy” and doubled the firm’s price target on the shares, from $50 to $100. The significant price target revision reflects strong analyst support and highlights that the firm sees growth potential.

According to 44 Wall Street analysts covering the stock, Intel currently holds a consensus “Hold” rating. Although the stock has already surpassed its mean price target, the highest price target of $111 still offers 3% upside from the current levels.

On the date of publication, Jabran Kundi did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/AI%20technology%20concept%20by%20NMStudio789%20via%20Shutterstock.jpg)