Rising central processing unit (CPU) prices are emerging as a near-term catalyst for semiconductor stocks, with Intel (INTC) and Advanced Micro Devices (AMD) both set to benefit from improving pricing dynamics. On March 25, shares of INTC and AMD rose 7.1% and 7.3%, respectively, following a report that the two companies plan to increase prices across their CPU product lines. The move comes amid tightening supply conditions, which are strengthening the industry’s pricing environment and are likely to support these companies' margins.

Beyond short-term pricing tailwinds, structural demand for CPUs continues to strengthen. Increasing adoption of energy-efficient processors is driving a global refresh cycle, while the rapid expansion of artificial intelligence (AI) workloads is strengthening the CPU’s role in modern computing infrastructure.

Intel or AMD: Which Stock Is the Better Bet?

While both companies are positioned to benefit from these trends, Advanced Micro Devices appears more attractive. AMD continues to gain market share in both server and PC processor segments, strengthening its competitive positioning. Its execution in high-performance computing markets has translated into solid gains.

On the other hand, Intel’s long-term outlook also remains constructive, supported by ongoing turnaround initiatives and efforts to reposition the business for growth in AI-driven markets. However, the recent rally in its share price suggests that these positive expectations may already be reflected in current valuations.

At the same time, AMD’s recent operating performance and earnings outlook suggest further room for upside. During its fourth-quarter earnings call, AMD management noted that adoption of its fifth-generation EPYC processors accelerated significantly, accounting for “more than half of the total server revenue.” Sales of fourth-generation EPYC chips also remained strong, reflecting competitive advantages in performance and total cost of ownership across a broad range of workloads. As a result, AMD achieved record server CPU sales across cloud and enterprise customers, and exited 2025 with higher market share.

Looking forward, demand conditions remain supportive. Hyperscale cloud providers are continuing to scale infrastructure to accommodate AI workloads, while enterprises are upgrading data centers to handle increasingly complex computational needs. These trends are expected to sustain strong demand for high-performance CPUs and to strengthen AMD's long-term growth prospects.

How High Can AMD Stock Go?

AMD continues to show strong momentum, supported by both its core CPU segment and its rapidly expanding data-center AI business. In Q4, the company’s Instinct GPU revenue reached a record level, driven by robust shipments of the MI350 series. Adoption of these accelerators broadened during the period, reflecting growing demand across cloud and enterprise customers.

Demand across AMD’s portfolio remains robust, particularly as emerging and agentic AI workloads require increasingly powerful computing infrastructure. These workloads are driving incremental demand not only for accelerators but also for high-performance CPUs, strengthening the company’s EPYC processor lineup. The convergence of CPU and AI accelerator demand positions AMD to benefit from multiple growth vectors within the data-center market.

Looking ahead to 2026, AMD’s growth outlook is supported by several key factors. These include deeper penetration of EPYC processors in cloud and enterprise environments, broader adoption of Instinct accelerators, continued market share gains in client processors, and a recovery in the embedded segment. Together, these drivers provide a solid foundation for sustained revenue expansion and improved profitability.

AMD projects its top line to grow at a compound annual growth rate (CAGR) of more than 35% in the next three to five years. This growth is expected to be accompanied by meaningful operating margin expansion and a significant increase in EPS, with annual EPS projected to surpass $20 within that timeframe.

AMD stock trades at a forward price-to-earnings (P/E) ratio of 36.4 times, which appears attractive relative to its anticipated EPS growth trajectory. Analysts forecast earnings growth of 72% in 2026, followed by a further 60% increase in 2027.

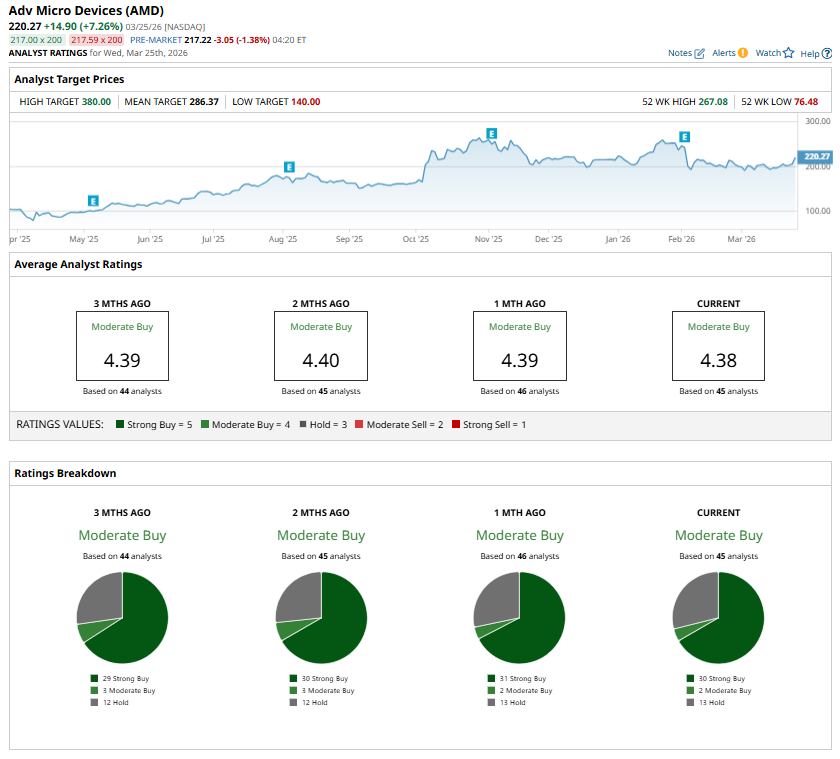

What Do Analysts Think of AMD Stock?

Market sentiment toward AMD stock remains constructive. Advanced Micro Devices holds a “Moderate Buy” consensus rating among analysts, in contrast to the consensus “Hold” rating assigned to Intel. The average analyst price target for AMD is $286.37, implying approximately 40% potential upside over the next 12 months. By comparison, INTC stock currently trades just below its average price target of $45.26, suggesting limited near-term upside based on expectations.

On the date of publication, Sneha Nahata did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20corporate%20sign%20for%20SK%20Hynix%20by%20Tada%20Images%20via%20Adobe%20Stock.jpeg)

/Server%20racks%20by%20dotshock%20via%20Shutterstock.jpg)

/2d%20illustration%20of%20Cloud%20computing%20by%20Blackboard%20via%20Shutterstock.jpg)

/Alibaba%20by%20Photo%20Agency%20via%20Shutterstock.jpg)