Under-the-radar insurance distributor The Baldwin Insurance Group (BWIN) is starting to turn heads on Wall Street, and artificial intelligence (AI) is the reason why. The company recently deepened its partnership with Anthropic to roll out its advanced AI assistant, Claude AI, across the entire organization. Baldwin is taking a company-wide approach, embedding Claude into multiple business segments and functions. The goal is to make teams faster, smarter, and more efficient.

From advisors to client experience teams and operational leaders, employees will now have access to AI tools designed to streamline workflows, speed up decision-making, and handle complex, end-to-end tasks with greater ease. The first phase focuses on frontline impact. Advisors and client teams will be able to analyze risk more efficiently, pull together client insights faster, and deliver more personalized insurance solutions.

At the same time, leadership teams will use AI-driven insights to improve operations and automate key processes. Importantly, this isn’t new territory for Baldwin. The company had already tested Claude in select parts of the business and saw noticeable improvements in productivity, workflow efficiency, and the quality of client insights. Now, with a full-scale rollout underway, Baldwin is taking things a step further, laying the groundwork for more advanced, end-to-end AI-driven workflows over time.

With AI becoming a bigger part of its strategy, Baldwin is quietly emerging as a stock that could be worth a closer look.

About Baldwin Stock

For those unaware of what the company does, The Baldwin Insurance Group, operating under the brand name The Baldwin Group, along with its affiliates, is an independent insurance distribution firm that provides expertise and insights designed to give clients the confidence to pursue their purpose, passion, and long-term goals.

Built by a team of entrepreneurs and insurance professionals, the Florida-based firm focuses on helping clients protect what’s possible. It does this by delivering bespoke client solutions, services, and innovation through a comprehensive and tailored approach spanning risk management, insurance, and employee benefits.

Beyond its core offerings, Baldwin supports clients, colleagues, insurance company partners, and communities by deploying forward-looking resources and capital to drive both organic and inorganic growth. Founded in 2011, the company today represents more than three million clients across the United States and international markets. The company’s market capitalization currently stands at about $3.14 billion.

However, shares of Baldwin Insurance Group haven’t exactly impressed on Wall Street, even with its big AI push. The stock has been under pressure, weighed down by concerns around high debt, integration challenges, and a broader shift in how investors are valuing insurance brokers. The stock’s performance has been notably underwhelming.

Over the past year, shares have tumbled 45.92%, with an additional 8.39% decline so far in 2026. In comparison, the broader S&P 500 Index ($SPX) has delivered strong gains, rising 28.42% over the same 12-month period and adding 6% year-to-date (YTD). From its peak of $45.16 last June, Baldwin stock is now down roughly 52.4%, underscoring the sharp pullback investors have faced.

Inside Baldwin’s Q1 Earnings Report

Baldwin Insurance Group kicked off fiscal 2026 with a headline-grabbing first-quarter earnings report on May 4, delivering powerful top line growth driven by acquisitions, even as its core organic momentum showed some near-term softness. The company posted total revenue of $532.2 million, up an impressive 29% year-over-year (YOY) and comfortably ahead of analyst expectations of $515.8 million.

Much of this surge came from the integration of CAC Group, a major partnership finalized in January that is already scaling faster than Wall Street had anticipated. That said, organic revenue growth, which strips out acquisitions, came in at a more modest 2%. Management was quick to add context, noting that when factoring in the new partnerships as part of the base, organic growth would rise to around 9%, offering a clearer picture of underlying momentum.

On the profitability side, Baldwin reported adjusted EPS of $0.63, in line with consensus estimates but down 3% from a year ago. Margins also felt some pressure, with adjusted EBITDA margin slipping to 25.8% from 27.5% last year, reflecting the costs tied to integrating large-scale acquisitions. Even so, adjusted EBITDA itself climbed 21% YOY to $137.2 million, highlighting solid earnings expansion despite integration headwinds.

A standout takeaway from the quarter was the pace of CAC Group integration. CEO Trevor Baldwin noted that the company has already executed 80% of its planned three-year expense synergies, while revenue cross-sell opportunities are materializing faster than expected and at meaningful scale.

Investors remain closely focused on the balance sheet, especially after long-term debt climbed above $2 billion following the January acquisition wave. Still, Baldwin appears well-positioned from a liquidity standpoint, ending March 31 with $146 million in cash and nearly $393 million in available credit.

Looking ahead, management remains confident in the trajectory, expecting organic growth to accelerate through the year and exit 2026 at a double-digit run rate, while continuing to push forward its ambitious $3B/30 Catalyst Transformation program.

How Are Analysts Viewing Baldwin Stock?

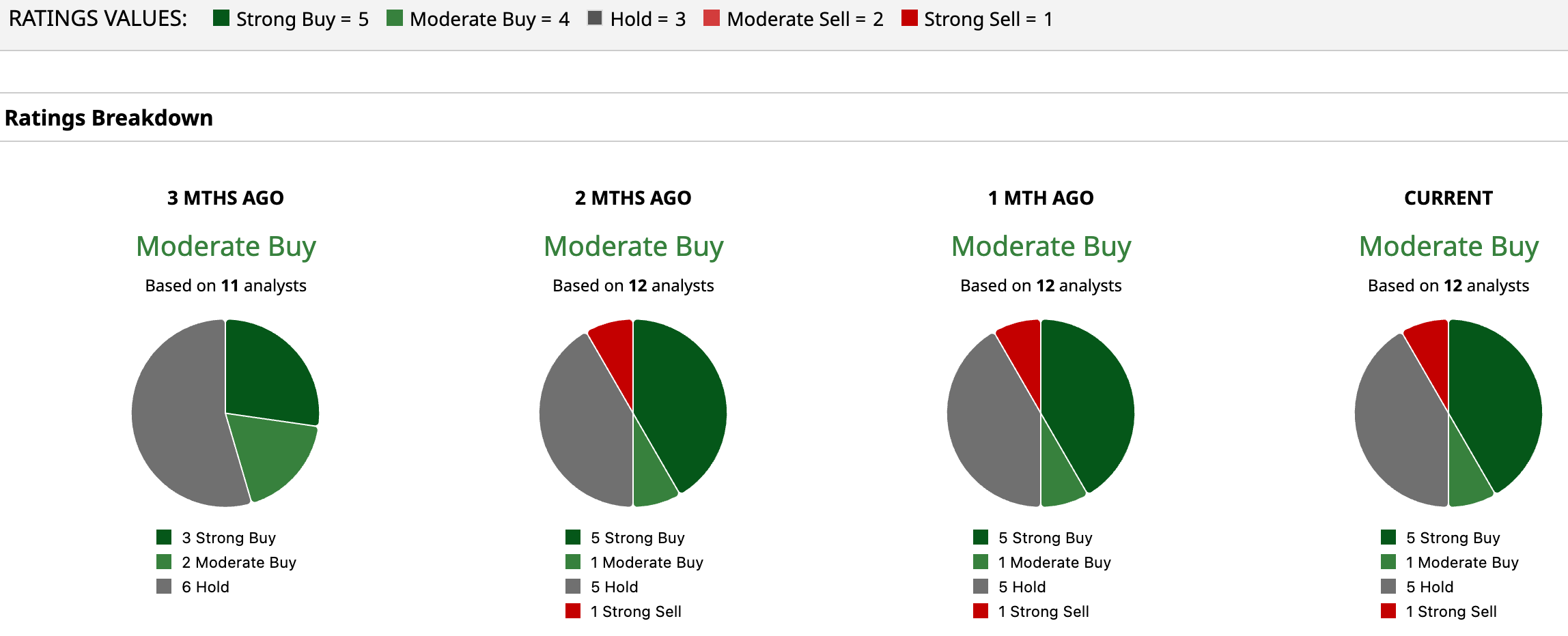

Even with a heavy pullback over the past year, Wall Street hasn’t given up on Baldwin just yet. The stock still holds a consensus “Moderate Buy” rating, with sentiment tilted toward the bulls. Of the 12 analysts covering the name, five analysts call it a “Strong Buy,” one backs a “Moderate Buy,” five prefer to stay on the sidelines with “Hold,” and only one remains firmly bearish with a “Strong Sell.”

And the upside case is hard to ignore. The average price target of $29.33 implies a healthy 36.6% rebound is on the cards, while the most optimistic forecast of $40 suggests the stock could rally as much as 86.3%, if things fall into place.

On the date of publication, Anushka Mukherji did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/Ai%20chip%20by%20Quality%20Stock%20Arts%20via%20Shutterstock.jpg)

/A%20Palantir%20office%20building%20in%20Tokyo_%20Image%20by%20Hiroshi-Mori-Stock%20via%20Shutterstock_.jpg)