Seagate Technology’s (STX) stellar Q3 earnings on April 29 prompted Rosenblatt analysts to double their price target on the data storage firm to $1,000, signaling more than 50% upside from here.

The Nasdaq-listed firm saw its revenue climb an exciting 44% in the third quarter on $4.10 in earnings per share (EPS) that topped Street estimates by a whopping 17%.

STX’s current-quarter guidance for $3.45 billion in revenue and $5 of per-share earnings also came in handily above Street estimates. Note that Seagate stock is already up about 90% year-to-date.

Why Is Rosenblatt Super Bullish on Seagate Stock?

Rosenblatt’s bullish view on STX shares rests on three pillars that now appear increasingly durable.

First, nearline HDD capacity is fully allocated through calendar 2027, with hyperscale customers already engaging in supply discussions for 2028.

Second, the company’s HAMR-based Mozaic platform has been qualified with five of the world’s largest cloud customers, delivering huge cost-per-bit advantages that underwrite margin expansion.

Third, the HDD industry operates as a functional oligopoly with only Seagate and Western Digital (WDC) controlling the vast majority of supply, creating sustained pricing power.

A small 0.46% dividend yield makes Seagate even more attractive to own for the long term.

Why Else Are STX Shares Attractive in 2026?

Seagate’s margin profile transformation on the back of artificial intelligence-driven data storage demand cycle has also been “extraordinary.”

In Q3, operating margin soared a remarkable 1,400 bps to 37.5%, reinforcing that the company is now operating with a structurally higher profitability baseline.

Meanwhile, STX reduced debt by $641 million, earning a Fitch investment-grade credit upgrade as well.

Rosenblatt sees massive upside in Seagate shares also because CEO Dave Mosley characterized the current environment as “a new era of structural growth," raising the longer-term annual sales growth target to a minimum of 20%.

Note that STX is currently trading firmly above its key moving averages (MAs), further signaling a strong uptrend.

Seagate May Attract Upward Revisions After Q3 Earnings

At about 49x forward earnings, other Wall Street analysts also don’t find STX stock as particularly expensive given its explosive AI-driven growth.

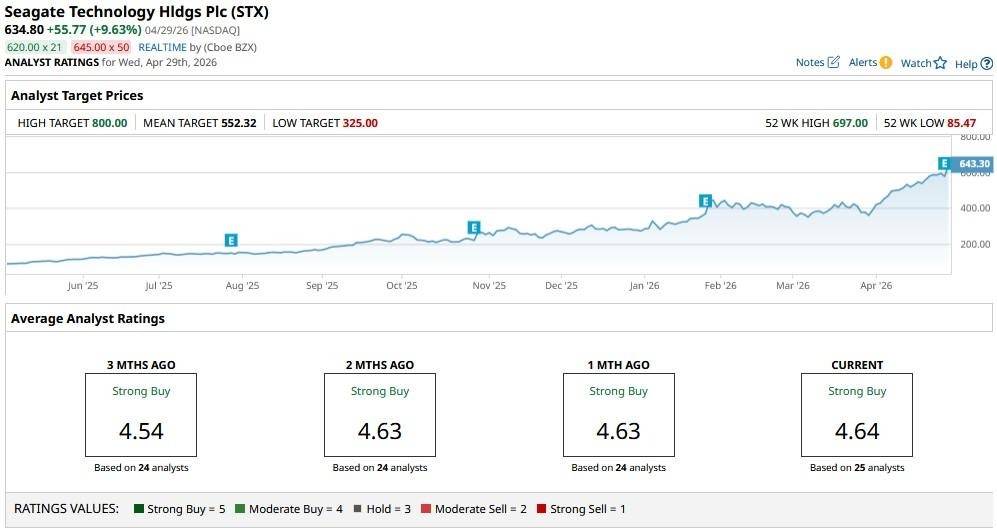

The consensus rating on Seagate Technology sits at “Strong Buy” currently, and while the mean price target of $552 suggests downside, it’s reasonable to assume that upward revisions, much like Rosenblatt’s, will follow after the firm’s standout Q3 release on April 29.

This article was created with the support of automated content tools from our partners at Sigma.AI. Together, our financial data and AI solutions help us to deliver more informed market headline analysis to readers faster than ever.

On the date of publication, Wajeeh Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20headquarters%20By%20Peter.jpeg)

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)