/A%20concept%20image%20of%20a%20self-driving%20car%20image%20by%20Gorodenkoff%20via%20Shutterstock.jpg)

Chinese autonomous vehicle technology player Pony AI (PONY) turned heads last week after rolling out a next-generation autonomous driving domain controller, built on Nvidia’s (NVDA) Drive Hyperion platform and powered by Drive AGX Thor with NVLink, technology purpose-built for L4 robotaxis and the next wave of autonomous mobility. The system is designed to unlock meaningful gains in artificial intelligence (AI) computing power and energy efficiency, while also supporting the latest AI models.

Importantly, it ticks all the boxes for L4 autonomy, including multi-sensor fusion, full-scenario perception, and the ability to interpret highly complex driving scenarios, the company noted. Pony AI expects the platform to scale across a range of compute tiers and cooling solutions, enabling deployment across a broad spectrum of autonomous applications. Notably, the company’s deep-rooted collaboration with Nvidia, dating back to 2017, continues to strengthen its position in the rapidly evolving self-driving ecosystem.

With this latest technological leap now in focus, does this momentum make PONY stock a buy, a sell, or a hold?

About Pony AI Stock

Founded in 2016, Pony AI has emerged as a key player in the push toward large-scale production and commercialization of autonomous driving technology. The company focuses on developing safe, advanced, and reliable self-driving solutions, anchored by its proprietary “PonyWorld” world model and Virtual Driver technology.

Together, these systems support the rollout and expansion of its Robotaxi and Robotruck services, as well as its broader licensing and applications businesses. With a presence across China, Europe, East Asia, the Middle East, and other regions, Pony AI is among a relatively small group of companies worldwide to achieve fully driverless commercial operations.

In addition, the company has built a wide network of partnerships across the autonomous-driving value chain, a strategy aimed at accelerating commercialization while working toward its long-term vision of “Autonomous Mobility Everywhere.”

Currently valued at $4.1 billion by market capitalization, Pony AI made its Nasdaq debut in 2024, and while the stock has slipped marginally over the past year, it has stumbled 29.28% in 2026 so far, pressured by mixed quarterly results, lingering profitability concerns, and ongoing U.S.-China tensions.

Pony AI’s Q4 Earnings Snapshot

Pony AI reported its fourth-quarter fiscal 2025 results on March 26, marking a pivotal moment for the company. Most notably, it delivered its first-ever quarterly GAAP net profit, posting earnings of $0.06 per share, a sharp turnaround from a loss of $0.99 per share in the same period last year. On a non-GAAP basis, loss per share came in at $0.12, significantly ahead of Wall Street’s projected loss of $0.15.

However, revenue painted a mixed picture. Total revenue came in at $29.1 million, down 18% from $35.5 million in the prior-year quarter, largely due to the timing of project-based revenue recognition in the Licensing and Applications segment. Nevertheless, strength in Robotaxi and Robotruck revenues helped cushion the decline, and the overall figure still topped analyst forecasts of $23.9 million.

Robotaxi revenue surged an explosive 160% year-over-year (YOY) to $6.7 million, while fare-charging revenue, generated directly from paid rides, skyrocketed by more than 500% YOY. This momentum was driven by the scaled rollout of its “Gen-7” vehicles, pushing the total fleet beyond 1,400 units. Gross margin came in at 12.7%, down from 21% a year ago, primarily reflecting a growing contribution from lower-margin Robotruck services.

The balance sheet also saw a major boost. Cash and cash equivalents, along with short-term investments, restricted cash, and long-term wealth management instruments, totaled approximately $1.51 billion as of December 31, 2025, up from $587.7 million as of September 30, 2025, driven largely by proceeds from its Hong Kong IPO in November 2025.

Capital expenditures rose to $6.6 million in the quarter, compared to $5.7 million a year earlier, mainly tied to investments in Gen-7 mass production and deployment. Looking ahead, management outlined aggressive plans for fiscal 2026, targeting a robotaxi fleet of more than 3,000 vehicles and expansion into over 20 cities globally.

How Are Analysts Viewing Pony AI Stock?

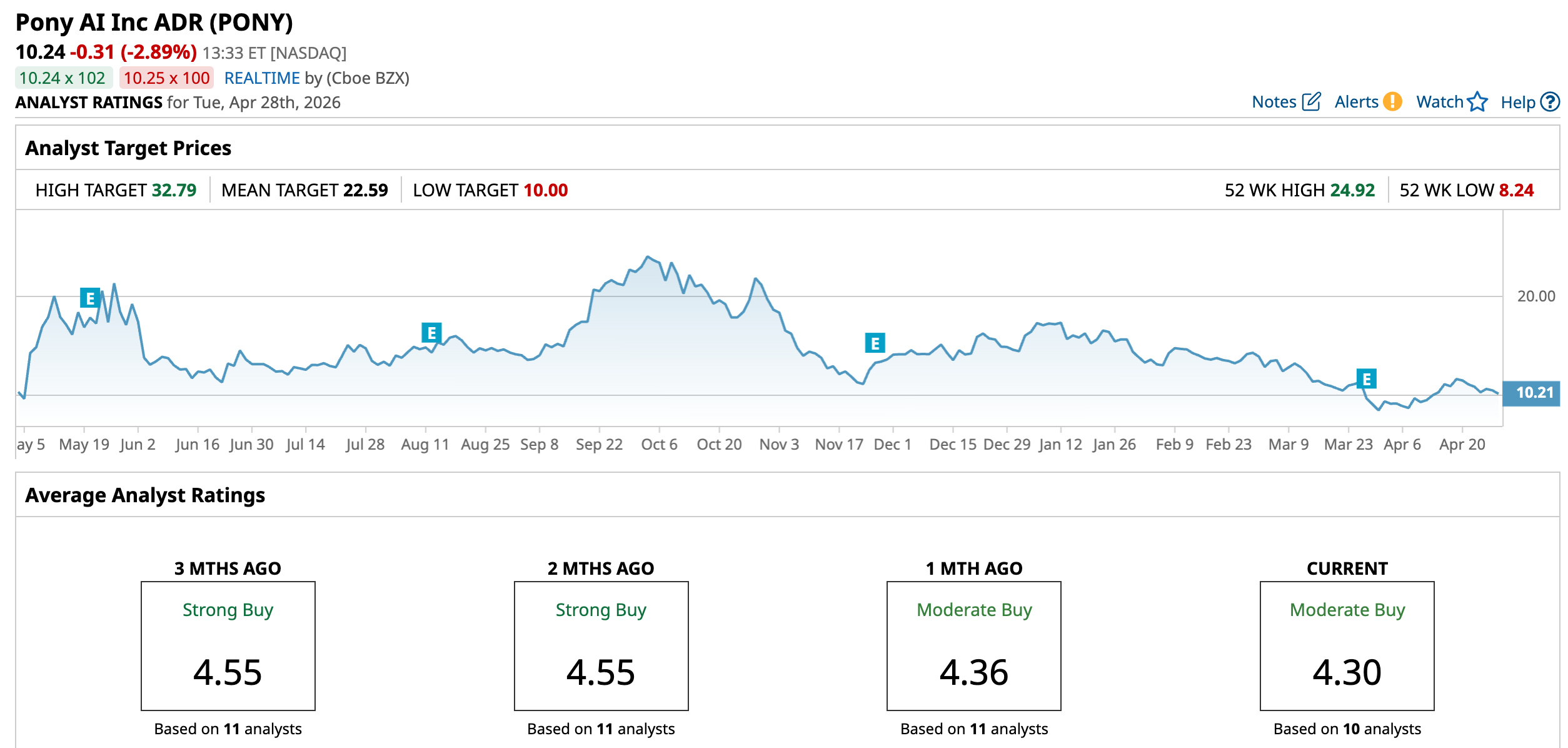

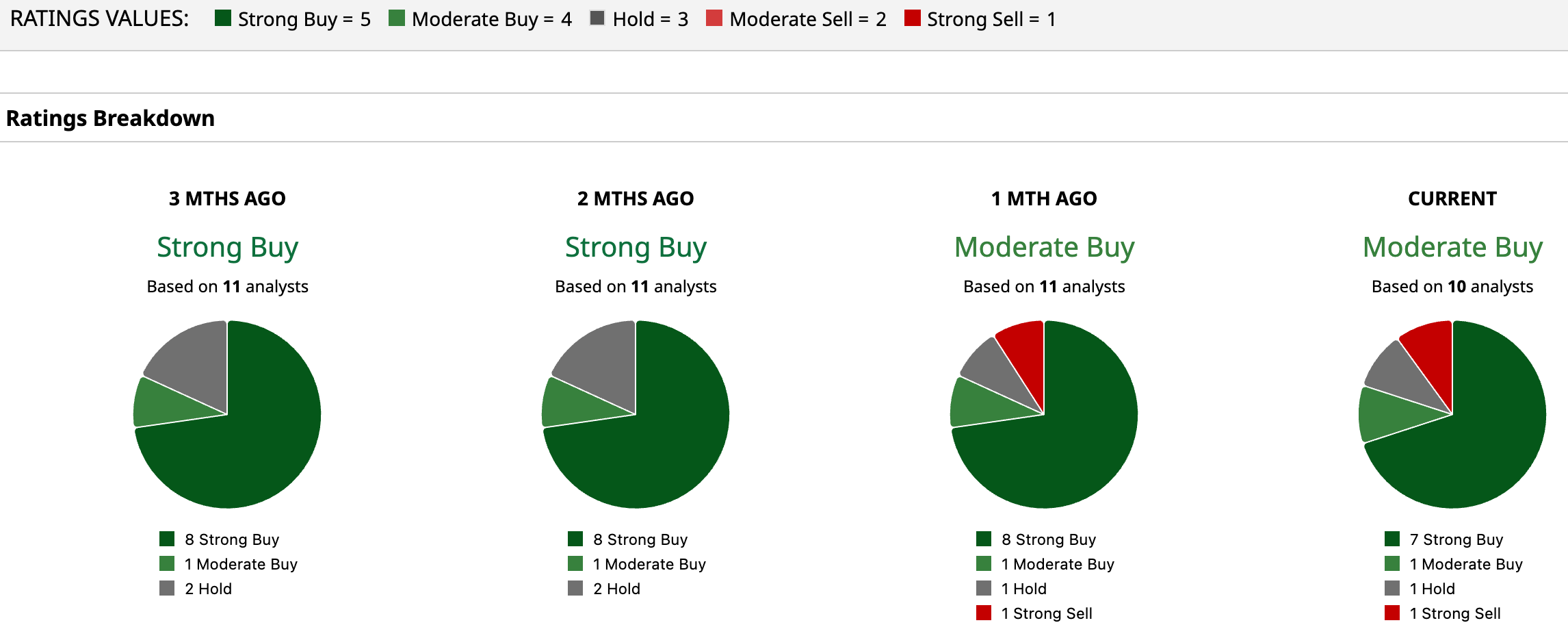

Overall, Wall Street’s stance on PONY remains notably bullish, with the stock earning a consensus “Moderate Buy” rating that leans heavily toward optimism. Of the 10 analysts covering the name, seven are firmly in the “Strong Buy” camp, one backs it with a “Moderate Buy,” one sits on the sidelines with a “Hold,” and just one takes a bearish “Strong Sell” view, highlighting a clear tilt toward confidence in the company’s long-term story.

The upside narrative is equally striking. The average price target of $22.59 points to a potential surge of 120.6% from current levels, while the Street-high target of $32.79 suggests an eye-catching rally of as much as 220.2% could be on the table.

On the date of publication, Anushka Mukherji did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Data%20codes%20through%20eyeglasses%20by%20Kevin%20Ku%20via%20Pexels.jpg)

/Space/Rocket%20launch%20streak%20by%20Alones%20via%20Shutterstock.jpg)

/Corning%20Incorporated%20on%20screen%20in%20front%20of%20website%20By%20Timon.jpeg)