/A%20Tesla%20Cybertruck%20with%20visible%20bullet%20impacts_%20Image%20by%20Karolis%20Kavolelis%20via%20Shutterstock_.jpg)

As Tesla (TSLA) CEO Elon Musk gets ready for a legal battle with OpenAI co-founder Sam Altman, the world's richest man recently revealed in a post on social media platform X (formerly Twitter) that its fully autonomous electric vehicle (EV) Cybercab is ready for production. Sounding cautiously optimistic about the pace, Musk said, "Whenever you have a new product with a completely new supply chain... you should expect that initial production of Cybercab and Semi will be very slow, but then ramping up... towards the end of the year and certainly next year."

After an uncharacteristic lull in terms of news flow, Tesla is back in the headlines. And it has mainly been for constructive reasons, barring the recent altercation with Altman, as Tesla recently expanded its robotaxi service to two new cities in Texas. Notably, the additional news of the Cybercab going into production will only add to the good vibes.

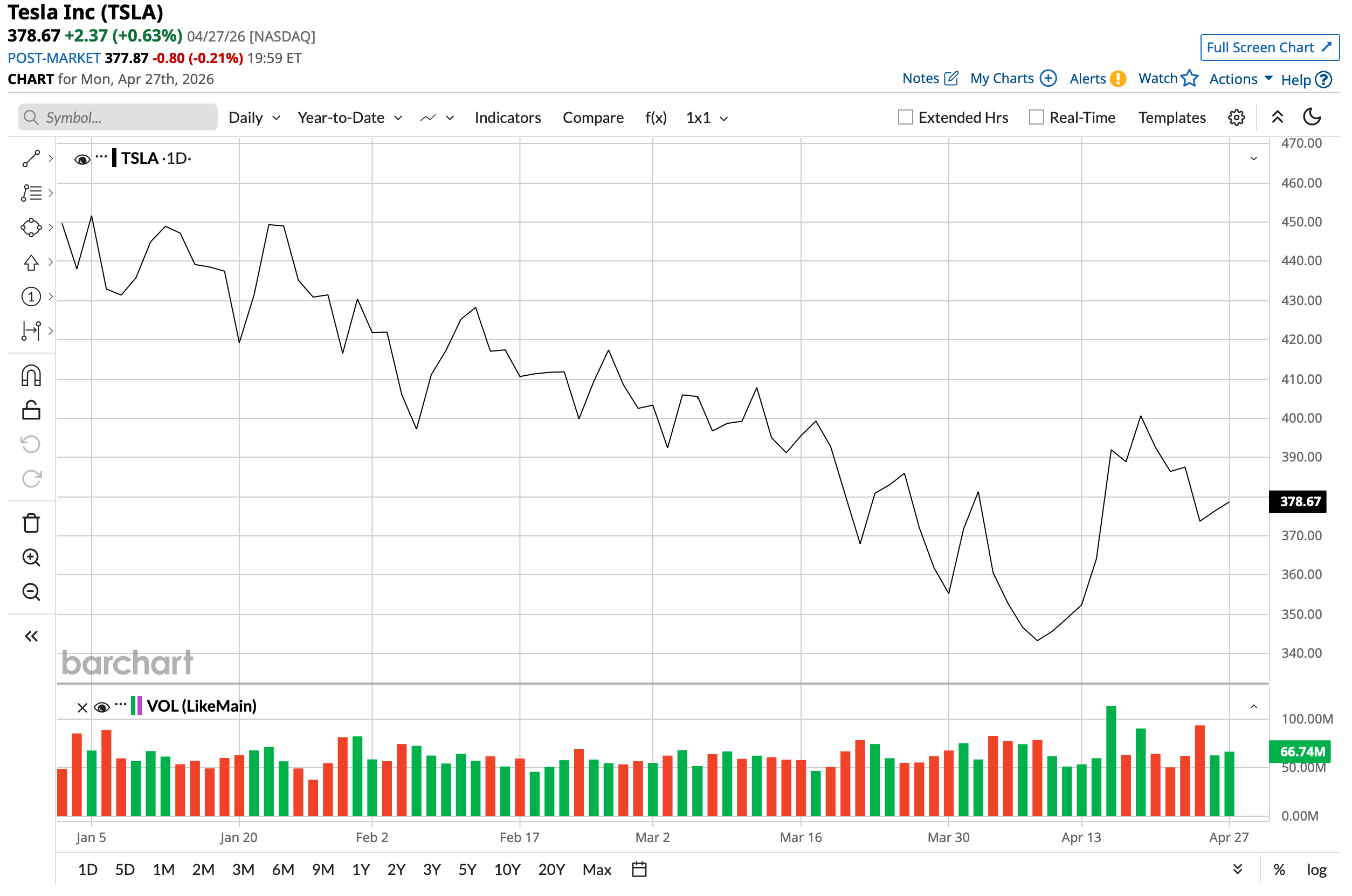

Yet, shares of the $1.5 trillion market cap company are still down 16% on a year-to-date (YTD) basis. So, can the start of production of Cybercabs lead to a reversal in the stock's fortunes? Let's find out.

Cybercab Potential

Many Tesla observers (and optimists) are betting that most of Tesla's future value will accrue from AI and robotics. Which is not off the mark at all. However, Tesla still remains a car company, and its growing capabilities in AI have and will continue to find applications in its vehicles. Especially the Cybercab.

Before the Cybercab, it would be appropriate to have a fair idea about the market potential of autonomous driving. Expected to reach a market size of $214.3 billion by 2030, Tesla, by virtue of being one of the leaders (with a global fleet of over 9 million vehicles) and the most recognizable name in the space, is surely going to be one of the biggest beneficiaries of this expanding market.

With the aim to sell under $30,000, it is expected that a ride in the Cybercab will cost less per mile than a human cab ($0.20 per mile vs. $2.80 per mile) by 2030. That is a 93% cost reduction for the end consumer. Beyond price, Tesla benefits from an existing FSD software stack trained on billions of real-world miles, which competing entrants would need years to replicate, making cost and data scale the two structural advantages Cybercab carries into a rapidly growing market.

And for the future, Tesla's playbook here combines fleet ownership with a peer-to-peer model. Musk has noted that Cybercab owners will be able to add their vehicles to the Tesla robotaxi network when not in personal use, potentially generating income to offset the vehicle's purchase cost, making the Cybercab something closer to an income-generating asset than a depreciating one. On the geographic front, Tesla confirmed plans to expand the Robotaxi program to seven new cities in the first half of 2026, including Dallas, Houston, Phoenix, Miami, Orlando, Tampa, and Las Vegas, while public road testing has already spread across five states. Longer term, Tesla's annual production goal is 2 million Cybercabs per year once several factories reach full design capacity, a figure that would dwarf anything any competitor has announced.

However, serious safety concerns remain, which Tesla should address quickly and effectively. Tesla's current supervised robotaxi fleet crashes at roughly four times the rate of human drivers, logging one crash per 57,000 miles compared to a human benchmark of one crash per 229,000 miles. Thus, the safety gap is challenging to paper over with ambition. There is also a leadership concern as three senior program leaders have departed since February 2026, leaving Tesla with no original program managers remaining for any of its production vehicles.

Q4 Beat

Tesla delivered results for the final quarter of 2025 that exceeded Wall Street forecasts for both revenue and earnings, yet the underlying performance revealed ongoing challenges that tempered any sense of optimism among investors.

The EV maker posted total revenue of $24.9 billion, marking a 3% decline compared with the same period a year earlier. Automotive revenue faced the steepest drop, falling 11% to $17.7 billion. Earnings per share came in at $0.50 per share, down 17% from the prior year, although the figure still managed to surpass the consensus estimate of $0.45 per share by a small margin. This marked the fourth straight quarter of year-over-year (YoY) declines in earnings per share. Over the past nine quarters, Tesla has beaten earnings estimates on only three occasions.

Notably, profitability also came under pressure as gross margins narrowed to 5.7% from 6.2% in the year-ago quarter. Operating cash flow decreased as well by 21% to $3.8 billion. Overall, at quarter end, the company held $44.1 billion in cash, which exceeded its short-term debt of $31.7 billion.

Meanwhile, vehicle production and deliveries weakened in the period after an earlier lift tied to the end of federal electric vehicle tax credits. Tesla produced 434,358 vehicles, a 5% increase from the previous year, while deliveries fell 16% to 418,227 units. Conditions remained difficult in the opening quarter of 2026, with production totaling 408,386 vehicles and deliveries reaching 358,023 units. Although these numbers missed the expected 365,000 deliveries, both production and deliveries showed YoY gains of 12.6% and 6.3%, respectively.

Positive developments emerged in select areas of the business, however. The number of active Full Self-Driving (FSD) subscriptions rose 38% from a year earlier to 1.1 million. The energy business maintained its upward trajectory, generating revenue that climbed 27% to $12.8 billion. Tesla also expanded its Supercharger network, increasing the number of stations by 17% to 8,182 locations and boosting the total count of connectors by 19% to 77,682.

On valuation metrics, Tesla shares continue to command a significant premium to the broader sector. The stock trades at a forward price-to-earnings ratio of 179.27, far above the sector median of 15.83. Its forward price-to-sales ratio stands at 13.85 versus a sector median of 0.89, while the price-to-cash flow multiple of 95.58 compares with an industry median of 10.02. These elevated multiples highlight persistent high expectations even as core business trends have softened.

Analyst Opinion on TSLA Stock

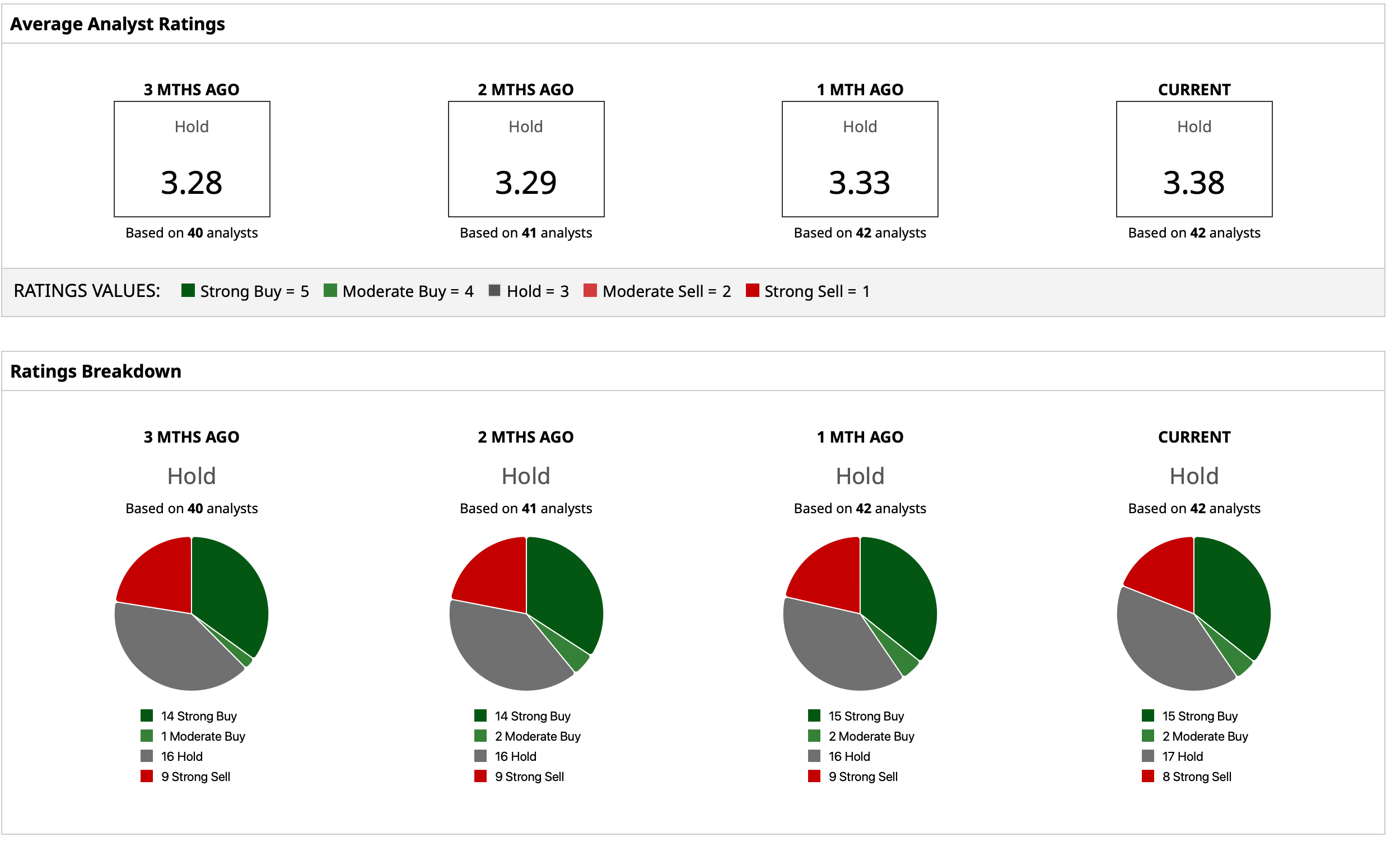

Amid all this, analysts continue to rate the TSLA stock a consensus “Hold.” The average target price of $404.20 denotes an upside potential of about 8% from current levels. Out of 42 analysts covering the stock, 15 have a “Strong Buy” rating, two have a “Moderate Buy” rating, 17 have a “Hold” rating, and eight have a “Strong Sell” rating.

On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/An%20aerial%20view%20of%20a%20data%20center%20cooling%20system%20by%20Sepia100%20via%20Adobe%20Stock.jpeg)