/Advanced%20Micro%20Devices%20Inc_%20logo%20and%20chart%20data-by%20Poetra_%20RH%20via%20Shutterstock.jpg)

Gil Luria of DA Davidson spent a good while watching Advanced Micro Devices (AMD) from the bleachers before deciding the time had come to get off the fence. He flipped his rating from “Neutral” to “Buy” and launched his price target from $220 to $375, a 70.5% leap that earned its place as one of the boldest calls Wall Street served up this year.

AMD stock took the compliment and ran with it on Friday, April 24, gaining 13.9% intraday to carve out a fresh 52-week high of $352.99. Luria anchored the $375 target to 32 times calendar year 2027 EPS and simultaneously bumped his 2026 revenue estimate by $2 billion and his gross profit estimate by $1.5 billion, clearing both Wall Street consensus and Advanced Micro’s own guidance by a comfortable margin.

Intel Corporation (INTC) handed Luria the smoking gun. Intel's Q1 fiscal 2026 report showed revenue of $13.6 billion, clearing the midpoint of its own guidance by $1.4 billion almost entirely on the back of a scorching surge in server Central Processing Unit (CPU) demand.

The plot thickens structurally because artificial intelligence (AI) workloads are moving away from pre-training toward inference, agentic AI, and multi-agent computing, pulling the Graphics Processing Unit (GPU)-to-CPU ratio from roughly 8:1 all the way toward parity.

Luria drew a straight line from Intel's windfall to Advanced Micro’s opportunity, noting that if Intel added roughly $2.5 billion annually on CPU tightness alone, AMD commands the same headroom.

He also pointed out that demand running ahead of supply hands Advanced Micro the leverage to raise prices across its entire portfolio and finally put the margin skeptics to rest. With demand running miles ahead of supply and the CPU era making a full-blown comeback, Luria's note essentially tells the margin skeptics to update their spreadsheets.

About Advanced Micro Stock

Headquartered in Santa Clara, California, Advanced Micro Devices is a global semiconductor powerhouse that designs high-performance CPUs, GPUs, and AI accelerators for a living.

Advanced Micro’s product bench runs deep, covering Ryzen processors, Radeon graphics, EPYC server chips, Field-Programmable Gate Arrays (FPGAs), and adaptive System on a Chip (SoCs), giving the company a foot in nearly every door worth knocking on across the computing world, all while sitting comfortably atop a market cap of roughly $567 billion.

Advanced Micro’s shares have been on an absolute tear over the past 52 weeks, skyrocketing 244.9%. The momentum rolled right into 2026, with the stock climbing 55.65% year-to-date (YTD) and tacking on another 65% over just the last month.

The last five trading sessions alone added 21.24% to the ticker, riding the coattails of a noticeably warming analyst sentiment that has the market paying close attention.

AMD stock currently trades at 52.82 times forward adjusted earnings and 12.12 times sales, both figures sitting at a premium not only to the broader industry but also to the company's own five-year average multiples. It signals that the market has priced in a great deal of optimism about the future direction of AMD stock.

Advanced Micro Surpasses Q4 Earnings

Advanced Micro strutted into Feb. 3 with Q4 fiscal 2025 earnings that made Wall Street do a double take. Revenue shot up 34.1% year-over-year (YOY) to $10.3 billion, leaving analyst estimates of $9.7 billion eating dust. Adjusted EPS punched 40.4% above the year-ago figure to land at $1.53, comfortably clearing Street forecasts of $1.32.

The Datacenter segment carried the heaviest load, swelling 39% YOY to $5.4 billion and proving once again that AI infrastructure spending shows no signs of pumping the brakes.

Every segment of the business pulled its weight at the table. The Embedded segment, the slowest horse in the stable, still trotted forward 3% YOY to $950 million, with expectations riding high for it to pick up steam as the year rolls on. The Client and Gaming segment threw its hat firmly in the ring with a sharp 37% climb to $3.9 billion.

Non-GAAP operating income charged ahead 40.9% from the year-ago figure to $2.9 billion. Non-GAAP net income went the distance and grew 41.8% YOY to $2.5 billion. Free cash flow stepped up 90.2% to $2.1 billion over the prior year's quarter, and adjusted EBITDA came in at $3 billion, up 38.7% from the same quarter last year.

Advanced Micro’s Q1 fiscal 2026 earnings report, penciled in for Tuesday, May 5, after the market close, now sits at the top of every semiconductor watcher's calendar as one of the most eagerly awaited prints in the sector.

The management has called for Q1 fiscal 2026 revenue of approximately $9.8 billion, give or take $300 million. The midpoint of that range marks YOY growth of approximately 32% and a sequential pullback of approximately 5%, with non-GAAP gross margin expected to hold at approximately 55%.

On the other hand, analysts tracking the stock see Q1 fiscal 2026 EPS growing 33.3% YOY to $1.04. They have set their sights on the full-year fiscal 2026 bottom line to rise 76.8% to $5.78, followed by another 59.2% climb to $9.20 in fiscal year 2027.

What Do Analysts Expect for Advanced Micro Stock?

AMD stock continues to draw strong backing from the Street. Investment firm Stifel Nicolaus has stepped in alongside DA Davidson. Analyst Ruben Roy lifted his price target to $320 from $280 and keeps a “Buy” rating in place, signaling confidence that AI infrastructure demand would keep running ahead of expectations and fuel steady expansion.

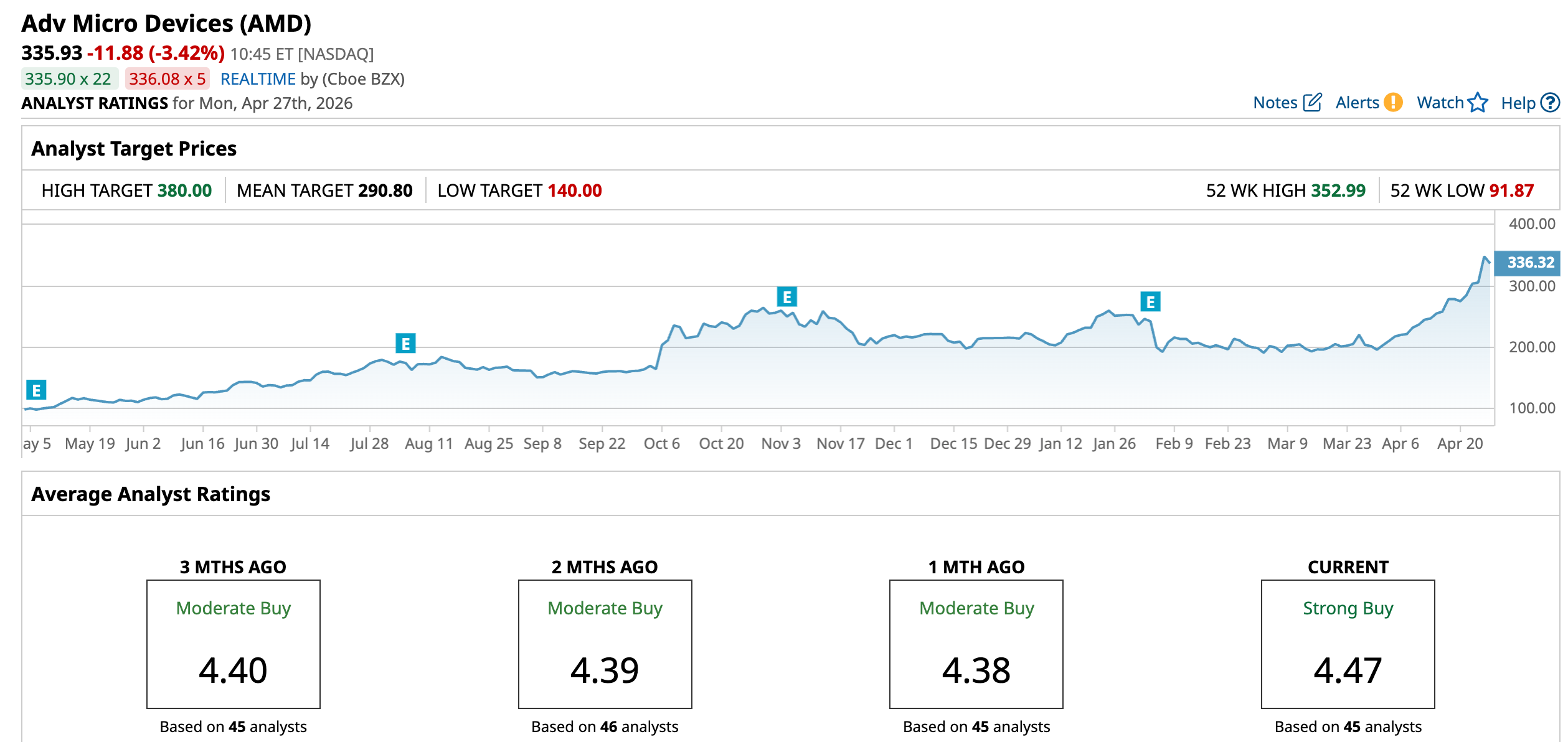

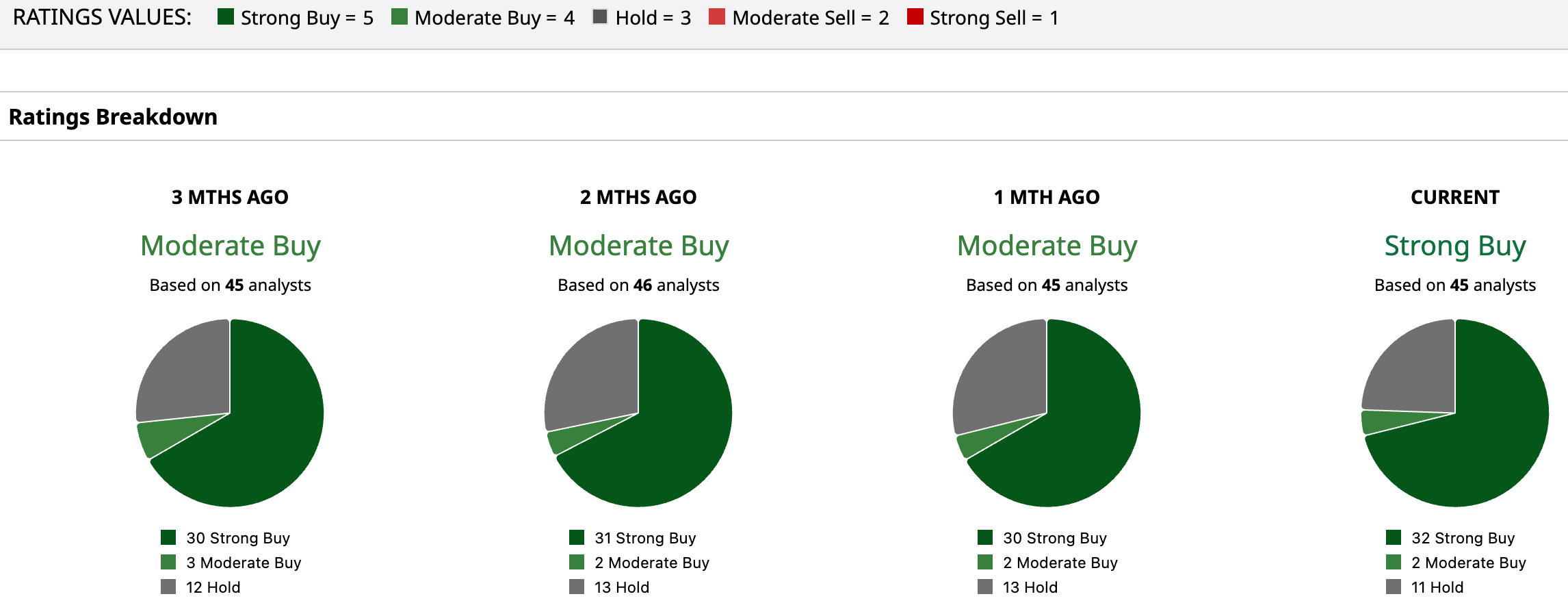

Wall Street has stamped AMD stock with an overall rating of “Strong Buy.” A total of 45 analysts weigh in, where 32 have issued “Strong Buy” calls, two lean toward “Moderate Buy,” and 11 choose to stay cautious with “Hold” ratings.

The stock already trades above its average price target of $290.80, which shows momentum has not waited for consensus to catch up. At the upper end, the Street-High target of $380 points to a gain of 13.12% from current levels, reinforcing the view that optimism around AI driven growth still has room to run.

On the date of publication, Aanchal Sugandh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Netflix%20open%20on%20tablet%20by%20rswebsols%20via%20Pixabay.jpg)

/Netflix%20on%20tv%20with%20remote%20by%20freestocks%20via%20Unsplash.jpg)