/International%20Business%20Machines%20Corp_%20logo%20on%20phone-by%20rafapress%20via%20Shutterstock.jpg)

International Business Machines Corporation (IBM) posted one of its strongest quarterly results in years, and the tech stock still sold off. Valued at a market cap of $218 billion, IBM stock is down 29% from all-time highs after a 9% decline last week. Should you buy the dip in IBM stock today?

Why IBM's Q1 2026 Results Deserve a Second Look

IBM grew revenue 6% in Q1, the strongest first-quarter revenue growth the company has posted in over a decade.

Its free cash flow rose 13% year-over-year (YoY) to $2.2 billion. IBM's chief financial officer, Jim Kavanaugh, called it the highest first-quarter free cash flow in a decade and the best free cash flow margin in the company's reported history.

- Operating earnings per share rose 19%.

- Adjusted EBITDA climbed 17%.

- Operating pre-tax margins expanded by 140 basis points.

These are the numbers of a business that is executing at a very high level.

Part of the reason is that IBM did not raise its full-year guidance. That disappointed some investors who were expecting management to upgrade the outlook after such a strong start.

IBM CEO Arvind Krishna acknowledged that the company rarely raises guidance after a single quarter and said the decision was prudent given an uncertain macro environment.

But here is the key detail: IBM is still projecting roughly $1 billion of added free cash flow for the full year of 2026. That growth is expected to be driven primarily by expanding adjusted EBITDA.

Software Business Is Accelerating

The exciting part of IBM's Q1 story lies in what is happening within its software segment.

- Software revenue grew 8% in the quarter and is forecast to rise by 10% for the full year of 2026, an acceleration from earlier guidance. That upgrade was driven in part by the early closing of its Confluent acquisition, which brings real-time data streaming capabilities to IBM's artificial intelligence platform.

- Data revenue grew 16% in the first quarter, and IBM now expects that segment to grow more than 20% for the full year.

- Red Hat, the open-source platform that sits at the heart of IBM's hybrid cloud strategy, grew 10% and is accelerating. Red Hat's OpenShift product is now a $2 billion annual recurring revenue business. Kavanaugh said virtualization contracts have topped $600 million since the beginning of 2024.

- Annual recurring revenue across the software business exited the quarter approaching $25 billion, up 10% YoY.

The AI Tailwind for IBM Stock

Krishna spent considerable time on the earnings call explaining why IBM is structurally positioned to benefit from the rise of AI, not just ride the initial wave of excitement.

As enterprises move beyond experimenting with AI and begin deploying it at scale, they need to draw on their internal data. That means more demand for IBM's data infrastructure, its Red Hat platform, and its automation tools.

IBM is also seeing a new monetization opportunity in its mainframe business. The company's Z platform can now run AI inferencing directly alongside financial transactions in real time.

Kavanaugh said IBM's flagship mainframe can handle up to 450 billion AI inferences per day with a response time of 1 millisecond. Financial services clients are already using this capability to run fraud detection on every single transaction rather than a small sample.

Clients that have deployed IBM's WatsonX Code Assistant for Z are growing computing capacity three times faster than those that have not, according to a company statement. IBM's internal AI development tool, called Project Bob, is now broadly available and delivering average productivity gains of 45% across its developer workforce.

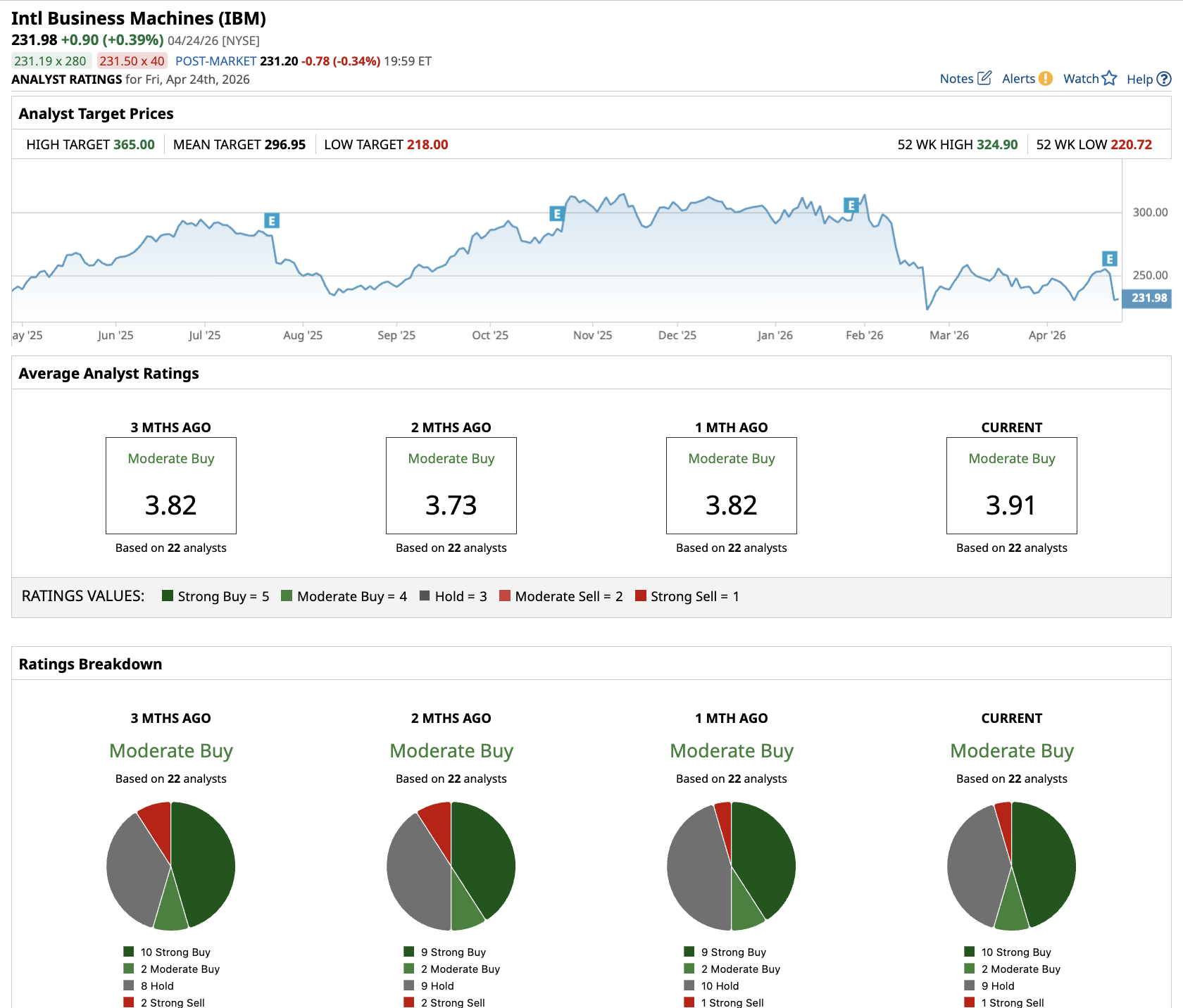

What Is the Stock Price Target for IBM?

Out of the 22 analysts covering IBM stock, 10 recommend “Strong Buy,” two recommend “Moderate Buy,” nine recommend “Hold,” and one recommends “Strong Sell.” The average IBM stock price target is $296.95, above the current price of about $232.

Analysts forecast IBM to expand free cash flow from $14.73 billion in 2025 to $21.87 billion in 2030. If IBM stock is priced at 15x forward FCF, it could surge over 50% within the next four years. If we adjust for dividends, cumulative returns could be closer to 65%.

The selloff in IBM stock may look like a stumble. But under the surface, this is a company with $1 billion in incremental free cash flow on the way, accelerating software growth, and an AI strategy that is starting to show up in the actual numbers.

On the date of publication, Aditya Raghunath did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20headquarters%20By%20Peter.jpeg)

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)