/International%20Business%20Machines%20Corp_%20logo%20on%20phone-by%20rafapress%20via%20Shutterstock.jpg)

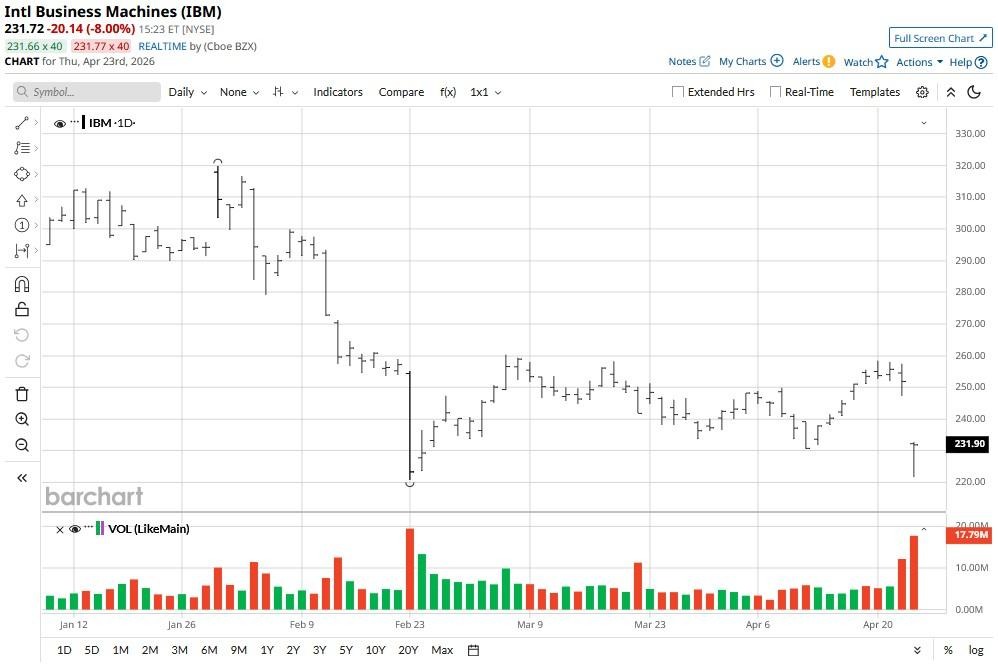

IBM (IBM) shares cratered on April 23 as investors read a sluggish 11% increase in the firm’s Q1 software revenue as evidence that AI disruption fears may not be particularly overblown after all. Despite a headline beat and reiterated full-year outlook, they treated IBM’s software weakness as unacceptable, especially because its management said, “Middle East developments didn’t impact us in Q1.”

The post-earnings decline saw IBM crumble below its 20-day and 50-day moving averages (MAs), indicating bears are beginning to seize control across multiple timeframes.

IBM stock has been a disappointment for investors amid AI disruption concerns in 2026, currently down some 24% versus its year-to-date high.

Should You Load Up on IBM Stock Today?

While IBM touted its Watsonx AI platform on the earnings call, the market focused on a sequential deceleration in its high-margin Red Hat unit that signaled AI might be a double-edged sword for Big Blue.

Fears intensified that generative AI tools, like those from Anthropic, are starting to automate tasks, specifically COBOL modernization, which was once a lucrative, labor-intensive mainstay for IBM.

Investors are now questioning whether artificial intelligence is purely driving growth, or perhaps cannibalizing IBM’s legacy high-margin revenue streams as well.

Note that IBM shares’ relative strength index (14-day), despite its year-to-date crash, is in the late 30s currently, indicating significant further room for downside.

Why Else Are IBM Shares Unattractive?

At 20x forward earnings, IBM isn’t a particularly inexpensive name to own, given that automated AI coding assistants seem to be disrupting its consulting business.

Plus, the firm currently has nearly $55 billion in debt on its balance sheet, which makes it much less attractive for institutional investors.

Note that IBM shares have a history of closing April in the red and gaining just 0.16% in May. This seasonal pattern further erodes the incentive to own them in the near term.

In short, with software margins under pressure and infrastructure cycles peaking, the legacy victim narrative is actually overshadowing IBM’s quantum and AI ambitions.

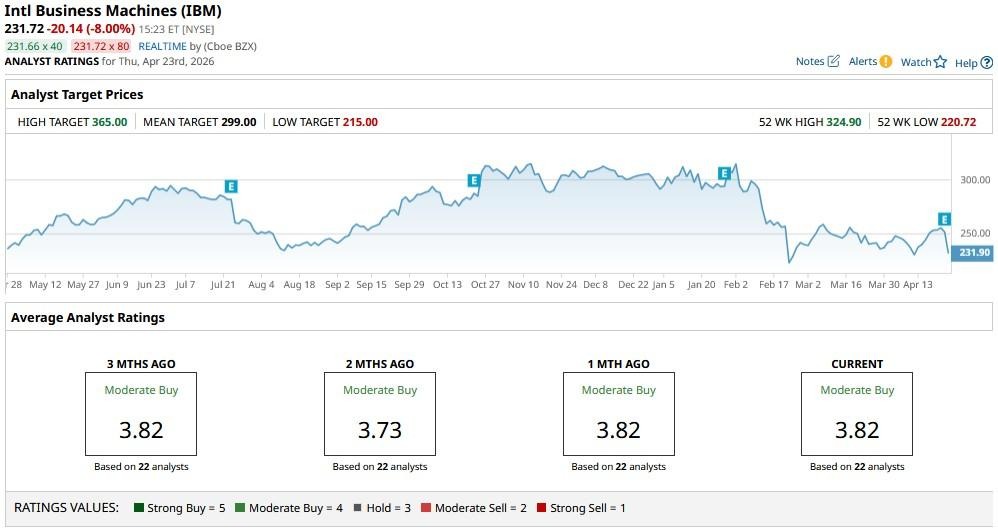

Wall Street Remains Bullish on IBM

Investors should note, however, that Wall Street believes IBM’s ongoing selloff has gone a bit too far.

The consensus rating on IBM stock remains at a “Moderate Buy” with the mean price target of about $299, indicating potential upside of roughly 30% from here.

On the date of publication, Wajeeh Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Accenture%20plc%20buiding%20with%20logo-by%20JHVEPhoto%20via%20iStock.jpg)