The cannabis industry has spent years navigating regulatory uncertainty, limiting the growth and profitability of marijuana companies despite strong demand. However, a fresh policy push from President Donald Trump's administration could mark a turning point for the sector. According to one report, the federal government may finally be ready to move forward with marijuana rescheduling — a move that could change the financial and operational prospects of cannabis operators.

For cannabis investors, this could signal a new phase of growth and opportunity in the sector.

A Long-Awaited Shift Gains Momentum

For decades, cannabis has fallen under Schedule 1 of the Controlled Substances Act. This has caused issues for cannabis firms attempting to operate legally at the state level while being restricted federally. Because of federal regulations, cannabis companies have struggled to secure financial support from banks, limiting funds for expansion.

Over four months ago, the Trump administration issued an executive directive to reclassify cannabis. Reclassification of state-licensed medical marijuana to Schedule 3 will ease restrictions around research, taxation, and regulation for cannabis operators. For example, Marijuana Moment states that it would eliminate IRS code 280E, allowing cannabis companies to deduct expenses, increase profitability, and attract institutional investment, possibly unlocking billions of dollars in value while speeding up research and medical use. However, this move does not legalize marijuana at the federal level. As part of that next phase, officials have scheduled a formal hearing to begin in late June.

It is important to note that the proposed rescheduling only applies to U.S. Food and Drug Administration (FDA) approved and state-licensed marijuana, while adult-use marijuana will continue to be classified as illegal at the federal level for now. Here are two cannabis stocks that stand to benefit from the policy shift when it finally happens.

Cannabis Stock #1: Tilray Brands (TLRY)

Among cannabis stocks, Tilray Brands (TLRY) stands out as one of the most diversified and internationally positioned companies in the sector. Unlike many of its peers, Tilray has built a presence beyond the United States, with operations spanning Canada, Europe, and the U.S. beverage market. This diversification has helped the company weather regulatory uncertainty, but the change in U.S. reform could unlock an entirely new growth engine. If rescheduling moves forward, Tilray could benefit in several ways, as access to capital, potential expansion opportunities in the U.S. medical market, and a more favorable tax environment could all boost its revenue and earnings.

In the third quarter of fiscal 2026, revenue climbed 11% year-over-year (YOY) to $206.7 million. The cannabis segment was a major growth driver, with net revenue rising 19% to $64.8 million from $54.3 million, driven by 73% YOY growth in international cannabis revenue and an 8% increase in Canadian adult-use and medical cannabis sales. Distribution revenue surged 35% YOY, mostly from higher medical cannabis sales in Europe.

Adjusted net income came in at $2.4 million compared to a loss of $2.9 million in the year-ago quarter. The company also strengthened its balance sheet with $264.8 million in cash and marketable securities, while lowering its debt by $4.2 million. For investors looking for a cannabis company with global exposure and multiple revenue streams, Tilray represents a compelling play now on reform-driven upside.

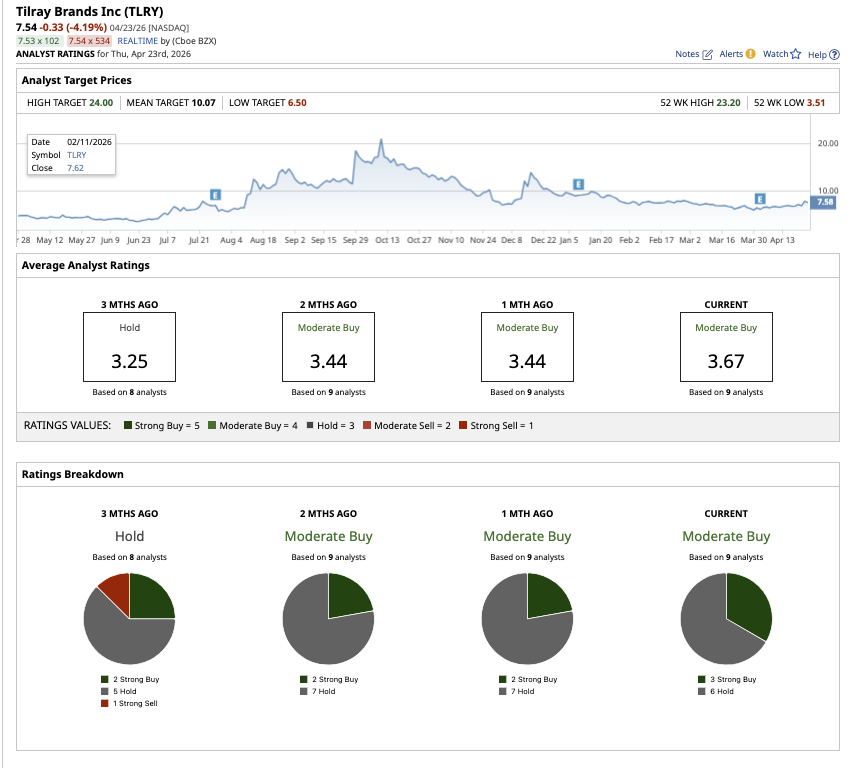

Overall, on Wall Street, TLRY stock is a consensus “Moderate Buy.” Out of the nine analysts covering the stock, three rate it as a “Strong Buy” while six have a “Hold" rating. While the stock is down 25% year-to-date (YTD), analysts expect shares to rally 51% from current levels based on the average target price of $10.07. Plus, the Street-high estimate of $24 indicates the stock could rise by as much as 260% in the next 12 months.

Cannabis Stock #2: Curaleaf (CURLF)

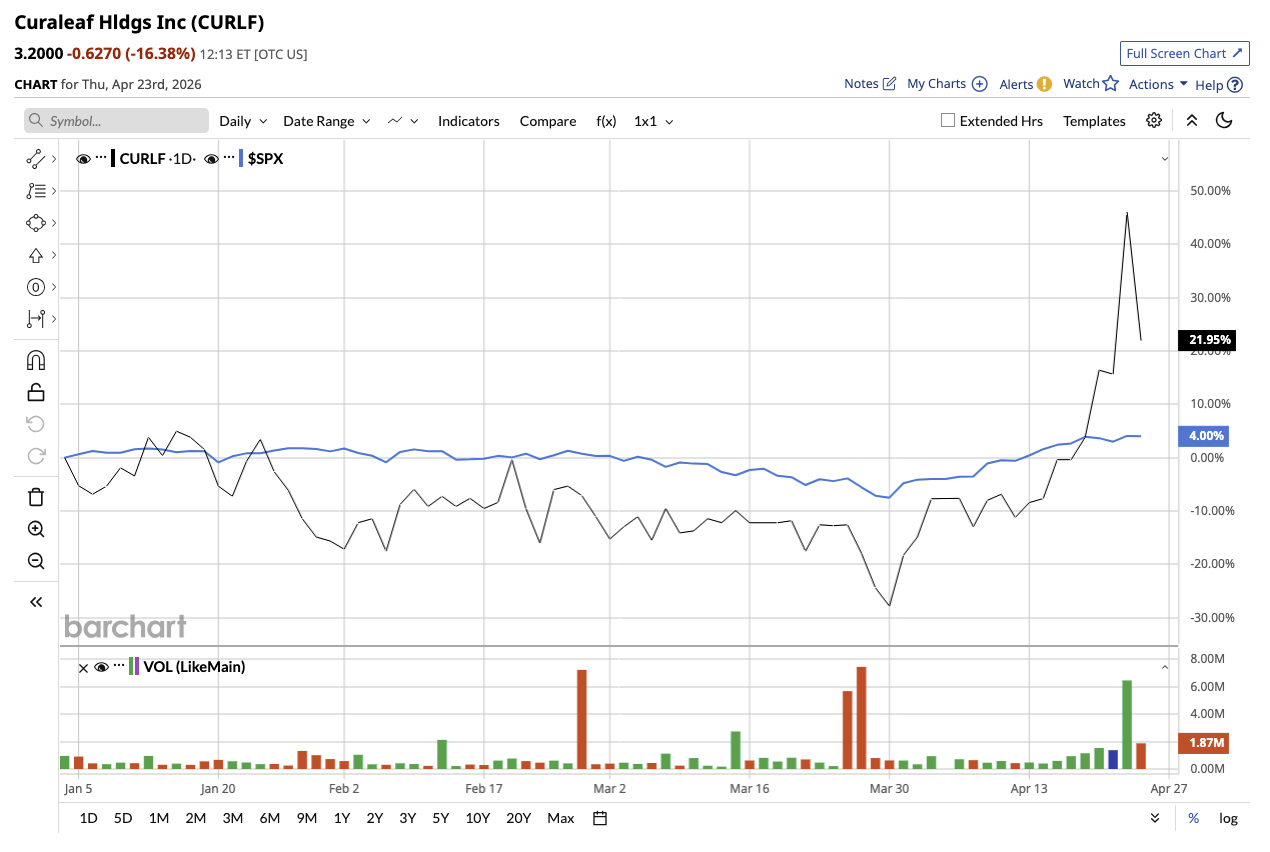

While Tilray offers international diversification, Curaleaf (CURLF) is a more direct bet on U.S. cannabis reform. The company is one of the largest multi-state operators in the United States, with more than 150 dispensaries across key markets. CURLF stock is up 29% YTD, outperforming the S&P 500 Index's ($SPX) gain of almost 5% YTD.

In the fourth quarter, Curaleaf reported a 2% YOY increase in revenue to $333.1 million, supported by a recovery across key domestic markets. International operations stood out, generating $51 million in Q4 revenue, an increase of 65% YOY. However, the bottom line suffered in the quarter, with an adjusted net loss of $39.5 million, or $0.05 per share. Nonetheless, the company generated $25 million in free cash flow during the quarter, ending the period with $101.6 million in cash. The firm also ended the year with $101.6 million in cash alongside $548.7 million in outstanding debt.

With easing tax burdens and operational restrictions, Curaleaf could see a significant improvement in profitability. The company’s scale and established infrastructure mean it is well-positioned to capitalize quickly if the regulatory environment becomes more favorable. For investors who want direct exposure to U.S. cannabis reform, Curaleaf remains one of the most closely watched names in the space.

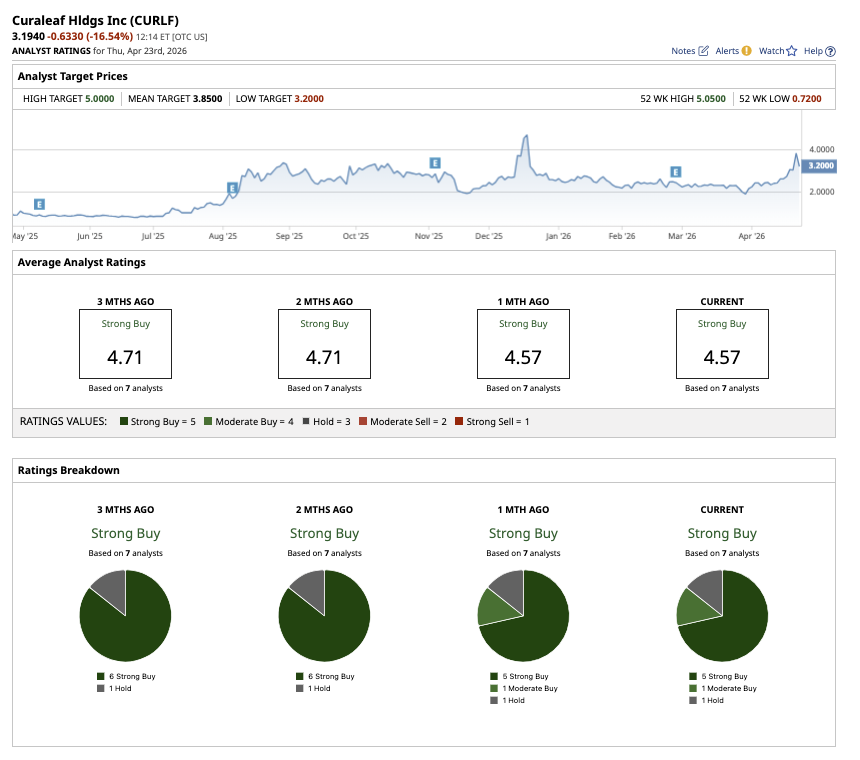

Overall, CURLF stock is a consensus “Strong Buy" on Wall Street. Out of the seven analysts covering the stock, five rate it as a “Strong Buy,” one analyst has a “Moderate Buy,” and one has a “Hold" rating.

Analysts expect the stock to rally 18% from current levels based on the average target price of $3.85. Plus, the Street-high estimate of $5 indicates potential upside of 54% over the next 12 months.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Nvidia%20logo%20by%20Konstantin%20Savusia%20via%20Shutterstock.jpg)

/Broadcom%20Inc%20HQ%20photo-by%20Sundry%20Photogrpahy%20via%20iStock.jpg)