/Cooper%20Companies%2C%20Inc_%20phone%20and%20site-by%20T_Schneider%20via%20Shutterstock.jpg)

Valued at a market cap of $12.6 billion, The Cooper Companies, Inc. (COO) is a global healthcare company specializing in medical devices and services across vision care and women’s health. Headquartered in San Ramon, California, the company operates through two primary divisions: CooperVision and CooperSurgical. It is scheduled to announce its fiscal 2026 Q2 earnings in the near future.

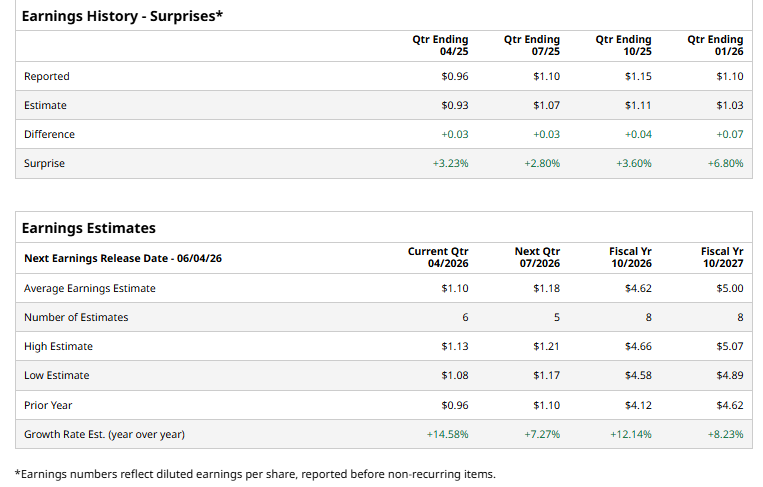

Ahead of this event, analysts expect this healthcare company to report a profit of $1.10 per share, up 14.6% from $0.96 per share in the year-ago quarter. The company has surpassed Wall Street’s bottom-line estimates in each of the last four quarters.

For fiscal 2026, ending in October, analysts expect COO to report a profit of $4.62 per share, up 12.1% from $4.12 per share in fiscal 2025. Its EPS is expected to further grow 8.2% year over year to $5 in fiscal 2027.

COO has declined 22% over the past 52 weeks, notably underperforming both the S&P 500 Index's ($SPX) 30.6% return and the State Street Health Care Select Sector SPDR ETF’s (XLV) 4.9% uptick over the same time period.

On Mar. 5, Cooper Companies reported a strong Q1 FY2026, with revenue reaching $1.02 billion, reflecting a 6% year-over-year growth. The performance was supported by steady demand across both business segments. CooperVision continued to benefit from a favorable mix shift toward higher-value products like daily disposable and specialty lenses, while CooperSurgical delivered stable growth driven by fertility and surgical solutions.

Profitability was the key highlight of the quarter. The company delivered a meaningful earnings beat, with adjusted EPS rising 20% year over year to $0.18, driven by margin expansion supported by cost discipline, pricing actions, and efficiencies from prior restructuring efforts. Looking ahead, management raised its full-year FY2026 guidance, signaling confidence in sustained demand, particularly in premium contact lenses and fertility-related offerings.

Wall Street analysts are moderately optimistic about COO’s stock, with an overall "Moderate Buy" rating. Among 17 analysts covering the stock, nine recommend "Strong Buy," one suggests a "Moderate Buy,” six indicate "Hold,” and one advises a “Strong Sell” rating. The average price target for COO is $90.60, indicating an 40.6% potential upside from the current levels.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/An%20Intel%20sign%20out%20front%20of%20a%20corporate%20office%20by%20wolterke%20via%20Adobe%20Stock.jpeg)

/A%20close-up%20of%20a%20SpaceX%20sign%20by%20Sundry%20Photography%20via%20Adobe%20Stock.jpeg)

/A%20close-up%20of%20the%20Broadcom%20logo%20on%20a%20smartphone%20by%20Timon%20via%20Adobe%20Stock.jpeg)