At times, the market’s reaction can diverge from the underlying business performance, and Netflix (NFLX) just experienced that. The streaming giant released its Q1 numbers last week. And despite impressive revenue and margin growth, the stock slipped as investors focused on a softer outlook, timing of subscription price hikes, and a mix of moving pieces – from its ties with Warner Bros. Discovery (WBD) to leadership shifts involving Reed Hastings. Investors were expecting more, and the gap between expectations and guidance triggered a sharp pullback in NFLX stock.

But not everyone sees this as a red flag. Doug Anmuth of JPMorgan is not too worried about the recent dip in NFLX stock. He believes the company is still executing well and has plenty of room to grow. The analyst points to record engagement levels, saying Netflix’s content is doing a strong job keeping users hooked and driving retention.

Beyond JPMorgan, the broader analyst view is not overly negative either after the company’s Q1 report. Most see this dip as a reaction to short-term guidance rather than any real crack in the business.

So, is this dip worth buying into? Let’s take a closer look at NFLX stock.

About Netflix Stock

Netflix is one of those companies everyone already knows about. Based in California, it started as a DVD-by-mail rental service and then completely changed the game by moving into streaming. Today, it’s a global entertainment leader with a market capitalization of $410.9 billion.

The platform uses smart artificial intelligence (AI)-driven recommendations to keep viewers engaged and watching longer. Over time, Netflix has stayed sharp with moves like launching an ad-supported plan in 2022 and cracking down on password sharing in 2023. It has also expanded into live content, including NFL games and comedy specials.

Now operating in over 190 countries with over 325 million paid subscribers, Netflix offers movies, series, documentaries, and even games. Its focus on original content has helped it reshape how the world consumes entertainment.

Shares of the mega-cap streamer has been moving through a mixed phase of strength and reset. Over the past 52 weeks, the stock is down 2.70%, reflecting cooling sentiment after earlier highs. It is still roughly 30% below its June 2025 high of $134.12, showing aggressive pullback from its top.

Over the past six months, Netflix has slipped 23.56%, as growth worries and guidance concerns weighed on sentiment. However, the short-term picture looks steadier, with the stock up 8.5% over three months and 3.11% in the past month. However, NFLX slipped 8.23% in the past five days as near-term sentiment cooled following a softer-than-expected Q2 outlook.

Technically, momentum had been building, with rising volume and a strengthening trend before the pullback began. The 14-day RSI recently touched overbought territory above 70, but has since cooled and now sits at 44.29, a more neutral level. Plus, the MACD oscillator signals bullishness, with the MACD line above the signal line and a positive histogram indicating improving momentum.

Even after the post-earnings dip, prominent brokerage firms frame the stock’s weakness as a potential buy-the-dip setup rather than structural damage. This mix of technical cooling and supportive sentiment suggests a stock still in transition.

NFLX stock is not trading at bargain levels, priced at 27.08 times forward adjusted earnings and 7.98 times forward sales, both above sector averages. Still, investors are paying for a story of expansion. With moves into ads, live content, gaming, and stronger content pipelines, the company is trying to build multiple growth drivers that could justify today’s premium over time.

Netflix Slips Despite Beating Q1 Numbers

Netflix started 2026 on a strong note with its Q1 earnings results released on April 16, delivering numbers that, at first glance, looked hard to fault. Revenue came in at $12.25 billion, up 16.2% year-over-year (YOY) and ahead of expectations. EPS amounted to $1.23, nearly doubling from $0.66 a year ago, also comfortably beating Wall Street’s estimates. A key driver behind the upside was stronger operating income, supported in part by a one-time $2.8 billion termination fee linked to its deal with Warner Bros. Discovery.

The advertising business continued to gain traction, with over 60% of new sign-ups in ad-supported markets opting for the lower-priced tier. Advertiser count surged 70% YOY to more than 4,000 clients, signaling growing acceptance of Netflix’s ad model. The management projects nearly $3 billion in ad revenue this year.

Cash generation was another highlight, with operating cash flow rising to $5.3 billion from $2.8 billion last year, pushing non-GAAP free cash flow to $5.1 billion.

Plus, Netflix is steadily widening its use of AI to enhance the member experience. In Q1, it acquired InterPositive to equip creators with a broader suite of generative AI tools. Alongside this, the company is reworking its mobile interface, with plans to roll out a vertical video feature by the end of the month.

However, the market reaction was clearly negative, with Netflix’s shares slipping nearly 10%, reflecting investor concerns around the forward trajectory rather than past execution. Management held firm on its full-year 2026 revenue guidance, signaling a more measured stance after a strong start to the year. Top line for the year is projected to be between $50.7 billion and $51.7 billion, implying 12% to 14% YOY growth. This growth is expected to be supported by steady membership gains, selective pricing actions, and a projected near doubling of its ad revenue base. Operating margin is anticipated to be around 31.5% for fiscal 2026.

However, near-term pressure is evident. For Q2, the company guided revenue growth of around 13%, reaching $12.57 billion and reiterated that content spending will remain heavier in the first half of the year due to the timing of major title releases. It also cautioned that Q2 will see the highest annual increase in content amortization for 2026, before easing in the second half.

Operating margin for Q2 is expected to be around 32.6%, down from 34.1% a year ago, largely reflecting elevated content investment. Management, however, expects margins to improve in the second half of the year, supporting the path toward its full-year target.

Adding a layer of transition risk, co-founder Reed Hastings is set to step down as chairman in June, prompting questions around leadership continuity.

Analysts tracking the company expects Q2 revenue to be around $12.6 billion, while EPS is projected to be $0.79. Looking ahead, EPS is forecasted to grow by 26.1% YOY to $3.19 in fiscal 2026, with the bottom line for fiscal 2027 projected to reach $3.88 per share, up 21.6% annually.

Overall, the outlook reflects steady growth but with short-term margin and sentiment pressures shaping investor focus.

What Do Analysts Expect for Netflix Stock?

JPMorgan reiterated an “Overweight” rating on the streaming giant’s stock with a $118 price target. Beyond JPMorgan, a broad set of analysts have stepped in to defend the bullish case on Netflix, even as weak guidance shook investor confidence.

Laura Martin of Needham argues the bigger story lies in Netflix’s expansion into complementary verticals like podcasts, gaming, and other IP-led ecosystems – moves that can deepen engagement, reduce churn, and steadily enhance pricing power. Plus, Needham maintained its “Buy” rating and $120 price target on NFLX after its Q1 results.

Jefferies’ James Heaney believes the sell-off reflects overly optimistic expectations around U.S. pricing and margins rather than any fundamental deterioration. Echoing that, Sean Diffley at Morgan Stanley points out that price hikes take time to reflect, suggesting the guidance may have been misinterpreted rather than weak. He also notes that Netflix’s failed pursuit of Warner Bros. Discovery, ultimately lost to Paramount Skydance (PSKY), underscored management discipline, showing willingness for large deals but with a high bar on valuation. The bank reiterated the “Overweight” rating on the stock and maintained its $115 price target.

Independent voices add another layer. While some view Netflix’s outlook as deliberately conservative, others note that investors may be overlooking the potential for margin expansion.

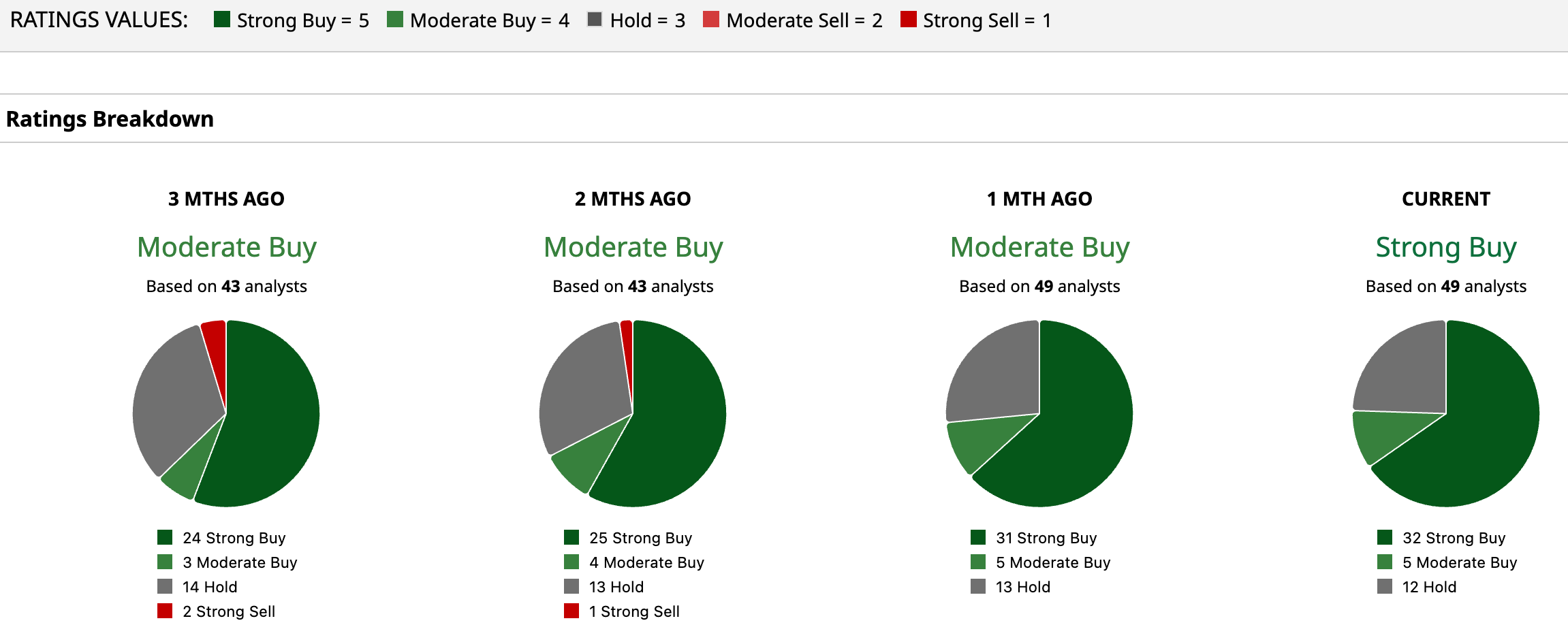

Overall, Wall Street is highly bullish on NFLX, giving a consensus “Strong Buy” rating, an upgrade from “Moderate Buy” a month back. Of the 49 analysts rating the stock, a majority of 32 analysts have recommended a “Strong Buy,” five suggest a “Moderate Buy,” and the remaining 12 analysts have a “Hold” rating.

Meanwhile, the stock has a mean price target of $115.63, which suggests an upside potential of 21.9% from current price levels. Meanwhile, the Street-high target of $137 implies the streaming giant’s stock could rise as much as 44.5%.

On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20close-up%20of%20a%20General%20Motors%20corporate%20sign%20by%20lindaparton%20via%20Adobe%20Stock.jpeg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Zoetis%20sign%20at%20their%20Canadian%20By%20JHVEPhoto.jpeg)

/Microsoft%20headquarters%20By%20Peter.jpeg)

/A%20SoFi%20logo%20on%20an%20office%20building%20by%20Tada%20Images%20via%20Shutterstock.jpg)