The fight for crypto customers among big-name brokers is heating up. In late March, Interactive Brokers (IBKR) enabled direct crypto portfolio transfers, letting clients move existing crypto onto its platform and trade at just 0.12% to 0.18% in commissions, which is about as cheap as it gets. A few days later, it rolled that out to individual investors across the European Economic Area (EEA) and added 11 cryptocurrencies alongside stocks, options, and futures.

Coinbase (COIN) is pushing the other way, adding U.S. stock trading to its app via USDC settlements and starting to look more like a full-service broker. Crypto platforms are moving into brokerage, and traditional brokers are moving into crypto. The only thing missing was a big move from the largest retail broker in the United States.

On April 16, Charles Schwab (SCHW) finally stepped in. The firm officially unveiled Schwab Crypto, a spot trading platform that gives its 39.1 million active brokerage accounts direct access to Bitcoin (BTCUSD) and Ethereum (ETHUSD) at 75 basis points per trade, which is on the low end of industry pricing. It sits right next to clients’ existing holdings on Schwab.com, Schwab Mobile, and thinkorswim, so crypto becomes just another line item in the portfolio, not a separate world.

With this move from the company, SCHW stock is back under the spotlight. But do the fundamentals still make shares worth buying here? Or has the market already rewarded most of this story? Let’s find out.

Is the Core Business Still Delivering?

Charles Schwab is basically a giant brokerage and wealth‑management shop. It pulls in money by gathering client assets, then earning net interest income, trading revenue, and advisory fees on those balances.

Over the last 12 months, SCHW stock is up about 22%. However, the stock is actually down by around 7% so far this year.

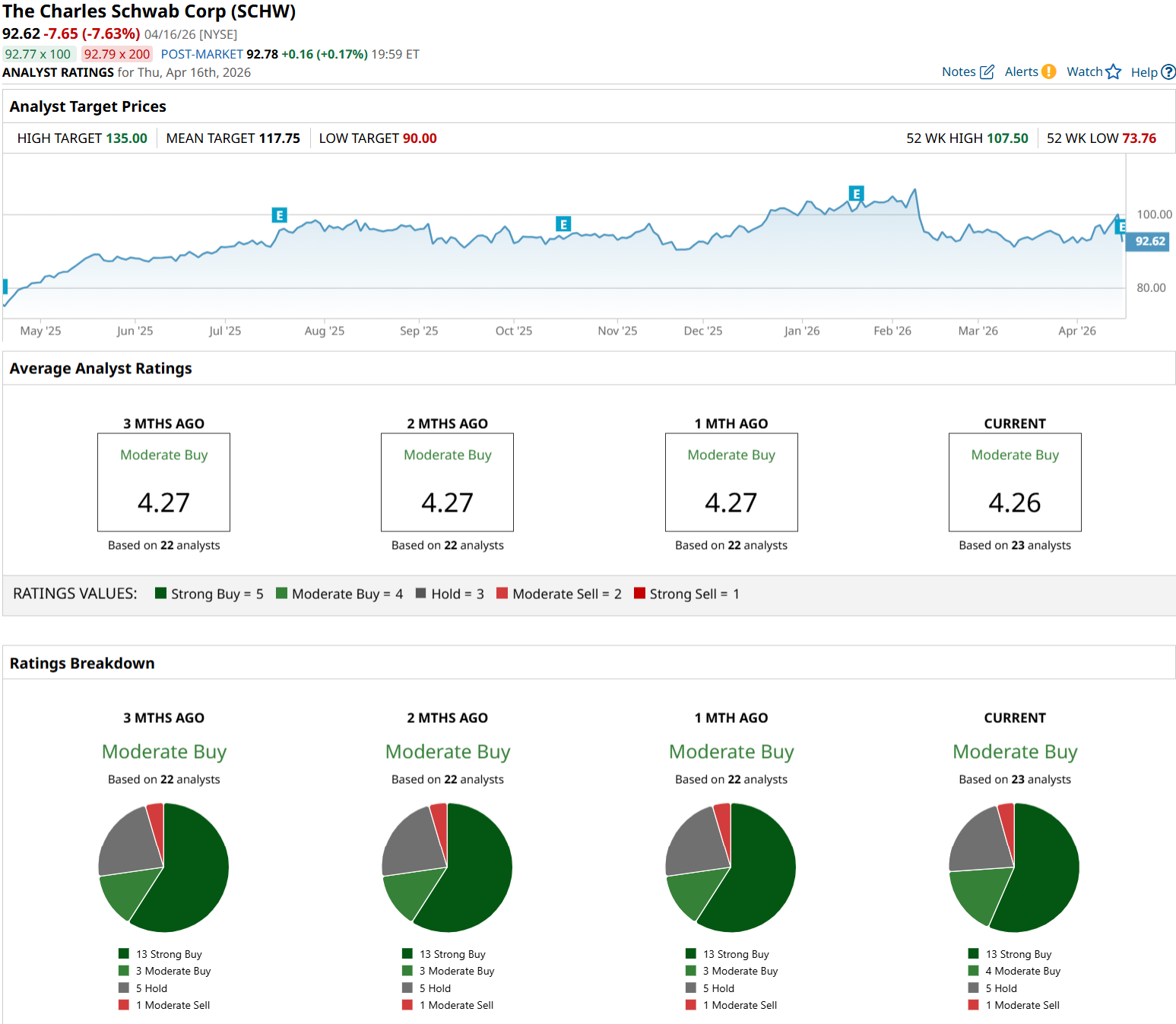

On the valuation front, SCHW trades at a forward price-to-earnings (P/E) ratio of roughly 16 times versus about 10.6 times for the sector, so investors are clearly willing to pay up for its growth profile and balance‑sheet strength. For income‑focused investors, the yield is on the low side but growing. The annual dividend yield is roughly 1.38%, backed by a recent $0.32 quarterly payout, a forward payout ratio of 21.03%, and two-straight years of dividend increases, compared with an average yield of about 3.18% across financials.

The latest quarter shows the business is still very much alive. Net income climbed to $2.48 billion, or $1.37 per share, from $1.91 billion, or $0.99, a year earlier. Revenue hit a record $6.48 billion, up 16% year-over-year (YOY). Client activity was also strong. Daily average trades jumped 34% to 9.9 million, trading revenue rose 20%, Schwab opened 1.3 million new brokerage accounts, and the company brought in $140 billion in net new assets in Q1 2026.

Evaluating Schwab’s Fundamental Growth Engine

Charles Schwab is leaning into private markets with its acquisition of Forge Global, which lets eligible investors get into pre‑IPO names through direct private share purchases, single‑company funds, and multi‑company funds. That basically drops a full private‑markets menu into Schwab’s existing public‑markets platform, so individual investors and RIAs can handle both sides in one place, and Schwab can deepen relationships with higher‑value, advice‑seeking clients.

It is also going younger. The Schwab Teen Investor account is a joint account for 13‑ to 17‑year‑olds and their parents or guardians, giving teens access to investment products, age‑appropriate education, and 24/7 support, plus $50 in fractional shares if they complete an online course within 45 days. Schwab’s survey work backs the push — 70% of teens say they’re very interested in investing, while 73% of parents believe it's important for their kids to learn about investing.

On top of that, the Charles Schwab Foundation is trying to widen the pipeline through the Schwab Moneywise Momentum Grants program, which is putting up to $2 million this year into nonprofits working on new ways to improve financial education. The goal is to help more people build practical, day‑to‑day money skills, and in the process support a larger base of informed, engaged current and future Schwab clients.

How Do Analysts See SCHW Stock After the Crypto Push?

Wall Street is still upbeat on Schwab. For the current quarter, analysts expect EPS of $1.46, up from $1.14 a year ago, which works out to about 28% growth. For the quarter following that, the consensus is $1.54 versus $1.31 last year, or roughly 17% growth. Looking further out, analysts see EPS rising from $4.87 in 2025 to $5.99 in fiscal 2026, suggesting growth of 23%.

On the ratings side, Keefe, Bruyette & Woods just started coverage on SCHW stock with an “Outperform” rating and a $110 target, highlighting Schwab’s scale and strong advisor demand as big earnings drivers. UBS also recently trimmed its target from $125 to $119, while Barclays cut its target from $126 to $117. Both firms still lean “Buy” but are a bit more cautious near term because of cash sorting and pressure on margins as rates and client cash behavior settle down.

Even so, the overall view is clearly positive. Analaysts have a consensus “Moderate Buy” rating with an average target of $117.85. Based on recent prices, that points to roughly 26% potential upside from here.

Conclusion

In the near term, SCHW stock looks much more like a hold‑to‑accumulate name rather than a clear sell. The core franchise is printing record profits, asset growth is robust, and analysts are modeling double‑digit EPS growth through 2027 on top of a modest but growing dividend. Meanwhile, the new spot crypto offering gives Schwab a credible answer to Interactive Brokers and Coinbase without changing the underlying playbook.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20corporate%20sign%20for%20SK%20Hynix%20by%20Tada%20Images%20via%20Adobe%20Stock.jpeg)

/2d%20illustration%20of%20Cloud%20computing%20by%20Blackboard%20via%20Shutterstock.jpg)

/Server%20racks%20by%20dotshock%20via%20Shutterstock.jpg)