/3d%20rendering%20by%20Phonlamai%20Photo%20via%20Shuttershock.jpg)

Solar stocks can move fast, but Sunrun (RUN) just got a catalyst that could change the story. The residential solar installer surged double digits after announcing a major partnership with Tesla (TSLA) and Renew Home aimed at supplying flexible power to data centers and utilities.

The headline event is the agreement announced yesterday, June 24. Sunrun, Tesla, and Renew Home plan to deliver more than 16 gigawatts of flexible energy capacity, enough to support the equivalent of 17 large data centers during peak demand.

The model is simple but powerful. Instead of relying only on new power plants or transmission lines, the companies want to aggregate existing home assets such as Tesla Powerwall batteries, Sunrun storage systems, and Renew Home’s network of more than 8 million smart thermostats.

That matters in a market where data center power demand is rising quickly. Goldman Sachs expects U.S. data center electricity demand to reach 66 gigawatts by 2027. At the same time, at least 75 U.S. data center projects worth about $130 billion were delayed or blocked in the first quarter of 2026 because of electricity concerns.

About Sunrun Stock

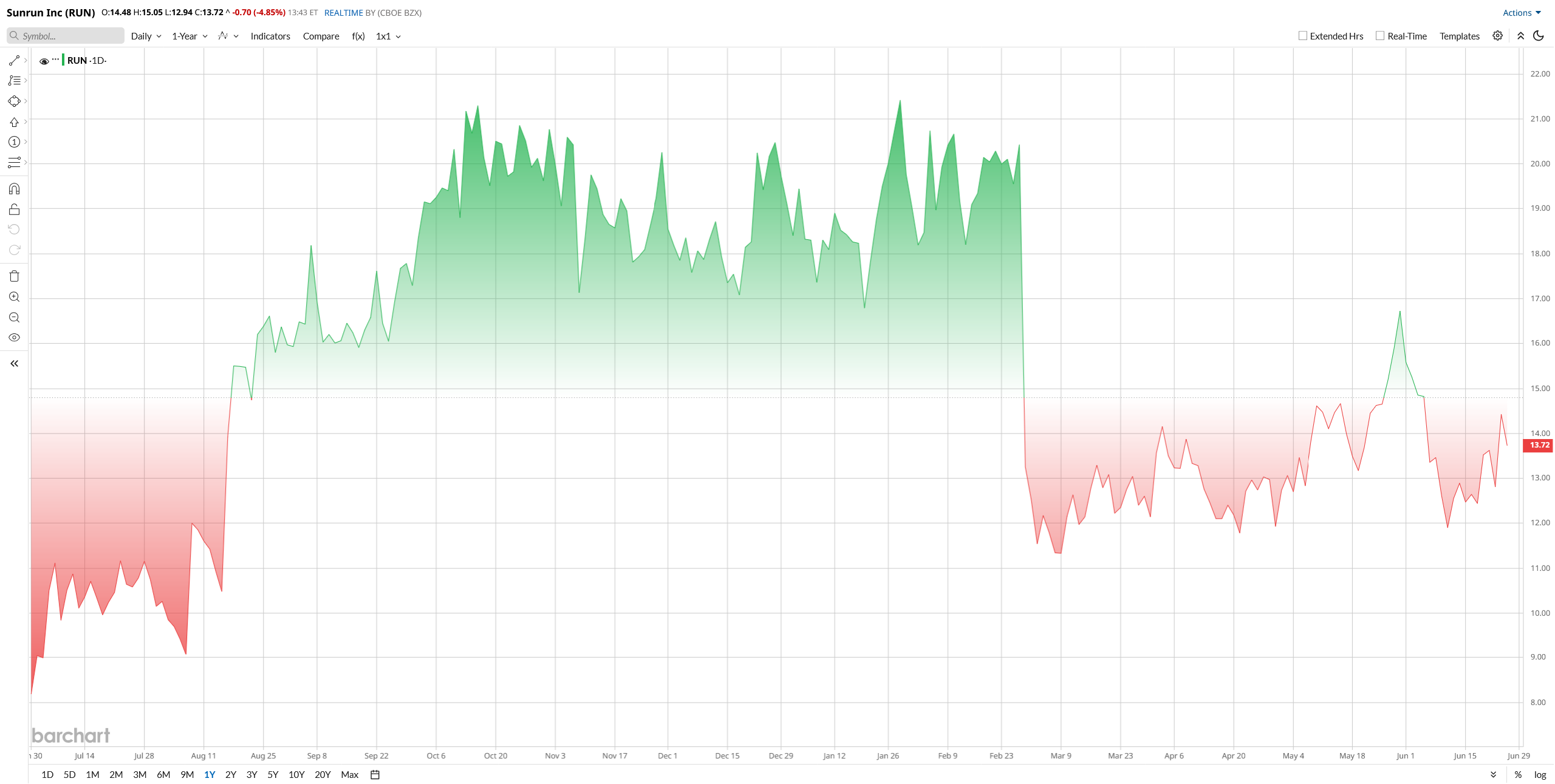

Sunrun had been under pressure this year, down more than 20% year-to-date (YTD) because of softer guidance, slower installations, and higher borrowing costs. Management warned that volumes could decline in 2026, which weighed on sentiment.

The Tesla deal changed that narrative in one session. The market is now looking at Sunrun less as a pure residential solar name and more as a distributed energy platform with a role in the AI infrastructure buildout. That shift explains why the stock erased most of its YTD losses so quickly. However, just as quickly as it rallied, the bears hit back and brought RUN stock back down today.

Even after the, admittedly, short rally, Sunrun does not look expensive on every measure. RUN stock trades at a trailing price-to-earnings (P/E) ratio of about 6, far below its five-year median of 36.36. Its EV-to-revenue ratio is 5.90, which sits about 7% below its 10-year median of 6.37. On a price-to-sales (P/S) basis, Sunrun trades around 1.03 times revenue, versus an electrical industry average of roughly 1.9 times.

Q1 Results Show Real Operating Progress

The latest quarterly report also helped build the bullish case. Sunrun’s first-quarter 2026 revenue came in at $722.2 million, up 43% from $504.3 million a year earlier and above analyst estimates of $688.5 million.

Adjusted earnings per share were $0.62, compared with $0.20 in the year-ago quarter and far ahead of the $0.01 analysts expected. Net income jumped to $167.6 million from $50 million in the same period last year.

Cash generation was still mixed. Sunrun reported a $148 million net decrease in cash and restricted cash, and cash generation was negative $31 million excluding equipment safe harbor investments. Even so, management kept full-year 2026 cash generation guidance at $250 million to $450 million.

Sunrun Is Doing More Than Chasing One Deal

The Tesla partnership is important, but Sunrun has also been reshaping its business. The company is leaning harder into a storage-first model and focusing on higher-value customers rather than volume alone.

That strategy showed up in several metrics. Sunrun added about 17,665 customers in the quarter, while its active sales force has grown more than 20% since the start of 2026. March bookings were also up more than 30% month over month.

The company’s storage attachment rate hit a record 73%, up from 69% a year earlier. Sunrun also said it extended its non-recourse warehouse facility to 2029 and increased commitments by $70 million to $2.7 billion. Year-to-date, it has raised $774 million in non-recourse asset-level debt financing. In total, the company has installed more than 251,000 solar and storage systems, representing about 4.3 gigawatt-hours of networked storage capacity.

Analysts Views on RUN Stock

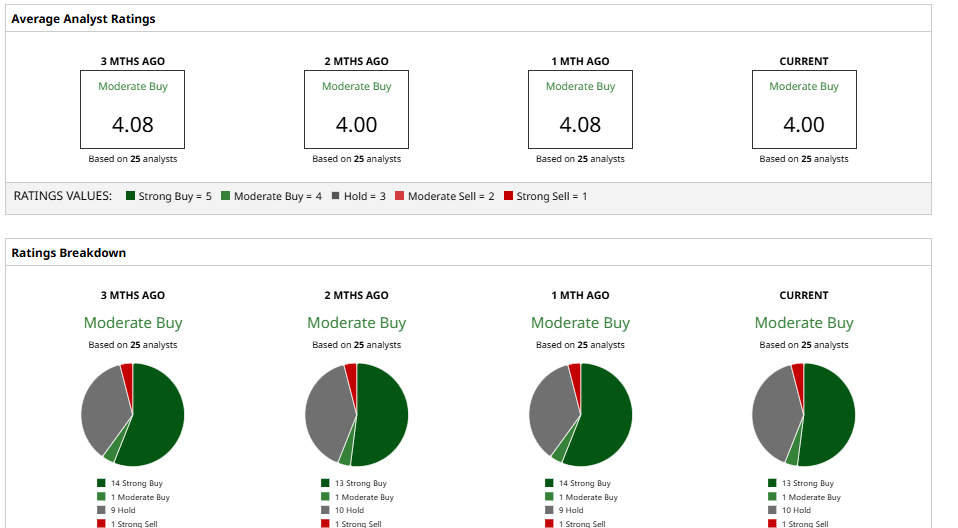

Wall Street is still mostly constructive. According to 25 analysts tracked by Barchart, RUN stock carries a consensus “Moderate Buy” rating with an average price target of $19, implying about 35% upside from recent prices.

UBS recently kept a “Buy” rating while cutting its target to $20 from $23. TD Cowen is at “Buy” with a $21 target, and RBC Capital has a “Buy” with an $18 target. Barclays remains more cautious with a “Hold” and a $14 target, while GLJ Research is the lone bear with a “Sell” and a $4.63 target.

The takeaway is simple. Sunrun is still a volatile stock, but the Tesla deal has given it a much bigger story and a clearer growth path. Now the market wants to see execution.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20Palantir%20sign%20displayed%20on%20an%20office%20building%20by%20Poetra_RH%20via%20Shutterstock.jpg)

/Bundle%20of%20optical%20fiber%20cables%20with%20lights%20by%20volff%20via%20Adobe%20Stock.jpeg)