/The%20CoreWeave%20logo%20displayed%20on%20a%20smartphone%20screen_%20Image%20by%20Robert%20Way%20via%20Shutterstock_.jpg)

The artificial intelligence (AI) infrastructure race is no longer confined to Big Tech, and CoreWeave (CRWV) just secured one of the clearest signals yet of the deep demand. In a landmark agreement, quantitative trading powerhouse Jane Street has committed $6 billion to CoreWeave’s AI cloud platform, alongside a $1 billion equity investment that makes it one of the company’s largest shareholders.

This isn’t just another customer win; it’s more of a validation moment. The deal underscores AI computing becoming mission-critical beyond traditional model developers, extending into capital markets where firms like Jane Street are increasingly reliant upon large-scale machine learning to drive trading strategies. Moreover, it highlights CoreWeave’s growing position as a key enabler of this shift, offering access to next-generation GPU infrastructure and specialized cloud services tailored for high-performance AI workloads.

Coming on the heels of multi-billion-dollar agreements with companies like Meta Platforms (META) and Anthropic, the Jane Street partnership reinforces a broader narrative that demand for AI compute is not only accelerating, but diversifying rapidly across industries. That diversification could prove critical in addressing prior investor concerns around customer concentration, while simultaneously expanding CoreWeave’s long-term revenue visibility.

Thus, the $6 billion commitment may represent a compelling reason for investors to take a fresh look at the stock today.

About CoreWeave Stock

CoreWeave, based in Livingston, New Jersey, was founded in 2017 and has transformed from its roots in cryptocurrency mining into a top-tier provider of GPU-optimized cloud infrastructure for AI training and inference. With a current market cap of about $50.1 billion, the company continues to expand its presence in the rapidly growing AI infrastructure market.

CoreWeave’s stock performance since its IPO has been marked by extreme volatility alongside strong absolute returns. The company went public in March 2025 at $40 per share and quickly became one of the standout AI trades, with the stock’s dramatic rise within months of listing as demand for GPU-backed cloud capacity surged.

That early surge gave way to a sharp correction, with the stock currently down 36.7% from the peak of $187, reached on June 20, 2025.

Despite these swings, CoreWeave has still delivered strong absolute returns over the past year, with gains of 202.75% and 65.26% year-to-date (YTD).

The most recent leg higher has been particularly sharp, with the stock rising 27.4% over the past five trading sessions. This move has been driven by a cluster of high-impact catalysts. A major multi-year agreement with Anthropic to support its Claude AI models signaled continued demand from leading AI developers, while an expanded $21 billion deal with Meta reinforced CoreWeave’s role to provide AI cloud capacity through December 2032. The momentum was further amplified by the announcement of a $6 billion AI cloud agreement with Jane Street, alongside a $1 billion equity investment, which broadened the company’s customer base into financial services and addressed prior concerns around client concentration.

The stock is currently trading at 5.14 times forward sales, which is a premium compared to its peers.

Steady Top Line Growth

CoreWeave reported its fourth-quarter and full-year 2025 results on Feb. 26, marking its first full year as a public company and underscoring both the scale of AI-driven demand and the financial strain of rapid capacity expansion.

In the fourth quarter, revenue reached $1.6 billion, up 110.4% year-over-year (YOY), reflecting continued demand for AI compute infrastructure. However, this top line strength was offset by a significant deterioration in profitability. The company reported a loss per share of $0.89, compared with $0.34 a year earlier and below the consensus estimate. Adjusted EBITDA grew strongly, up roughly 84.7% YOY to about $898 million.

For the full year, CoreWeave delivered $5.1 billion in revenue, representing about 167.9% YOY growth, positioning it among the fastest-growing companies in the AI infrastructure space. Despite this, profitability moved in the opposite direction. Full-year loss per share came in around $2.81, compared to $4.30 in the prior year.

One of the most important structural metrics was backlog, which expanded dramatically to $66.8 billion, more than four times from the beginning of the fiscal year and providing strong forward revenue visibility.

Moreover, Q1 2026 revenue guidance stood at $1.9 billion to $2.0 billion, while the company is targeting $12 billion to $13 billion in full-year 2026 revenue. Also, CoreWeave outlined a plan of $30 billion to $35 billion in 2026 capital expenditures.

However, analysts anticipate losses to deepen in fiscal 2026, with loss per share expected at 54.7% YOY to -$4.16, before improving 8.9% to -$3.79 in fiscal 2027.

What Do Analysts Expect for CoreWeave Stock?

Cantor Fitzgerald raised its price target on CoreWeave to $156 and maintained an “Overweight” rating, citing the company’s $6 billion Jane Street deal and a series of major contracts as drivers of stronger backlog, faster near-term revenue growth, and improved customer diversification.

Also, Evercore ISI raised its price target on CoreWeave to $150 and reiterated an “Outperform” rating after the $6 billion Jane Street expansion.

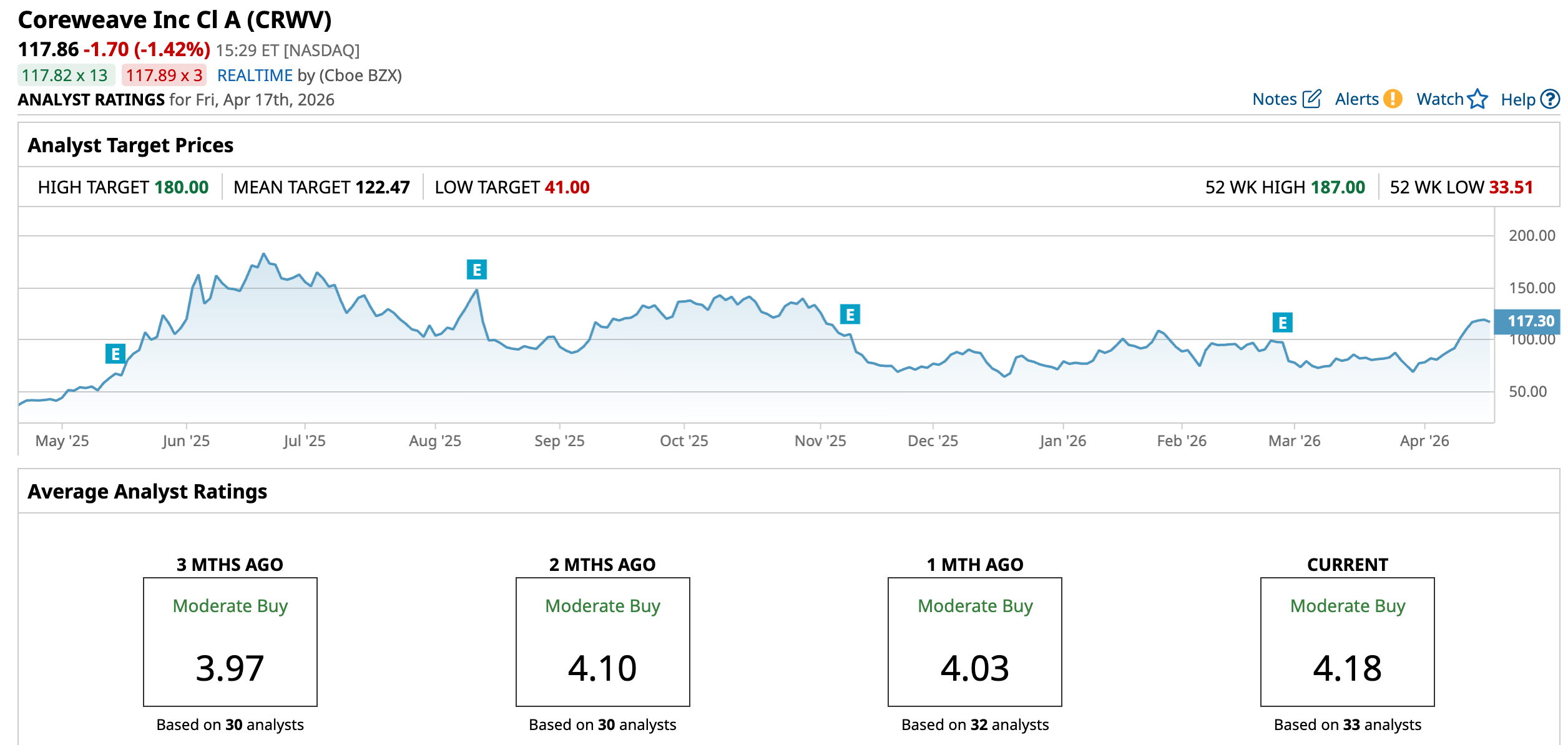

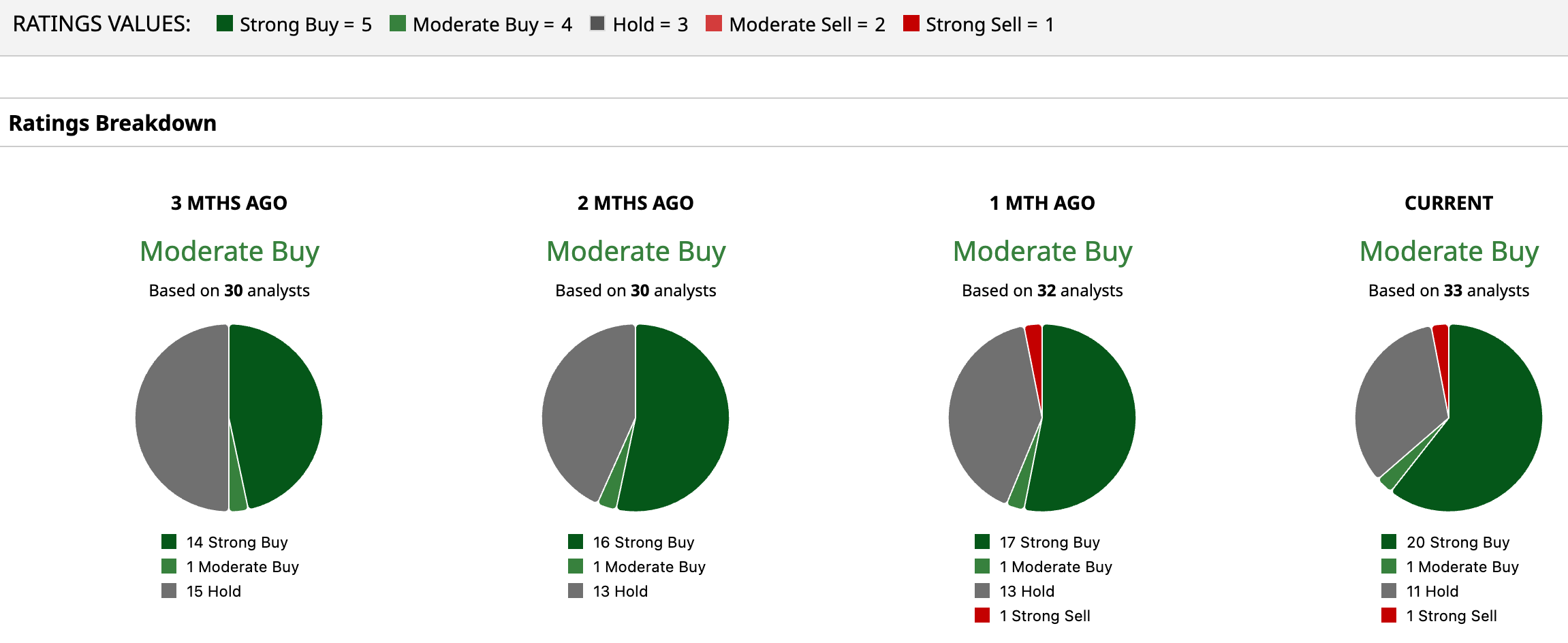

CoreWeave stock has a consensus “Moderate Buy” rating overall. Out of 33 analysts covering the stock, 20 recommend a “Strong Buy,” one gives a “Moderate Buy,” 11 analysts stay cautious with a “Hold” rating, and one advises a “Strong Sell.”

CRWV’s average analyst price target of $122.47 indicates a 3.9% upside potential. Plus, the Street-high target price of $180 suggests 52.7% upside ahead.

On the date of publication, Subhasree Kar did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/2d%20illustration%20of%20Cloud%20computing%20by%20Blackboard%20via%20Shutterstock.jpg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)