Travel stocks have been hit hard by the Iran war and the ensuing oil price spike, and Booking Holdings Inc. (NASDAQ: BKNG) is now down nearly 15% year-to-date (YTD). But now that the market appears to have turned a corner, is it time to buy this beaten-down company? We’ll review the bull and bear cases and then consult the charts to make an informed decision before the summer travel season heats up.

Reasons to Be Bullish on Booking Holdings

The Online Travel Agency (OTA) industry replaced traditional travel agent business models as the internet and smartphones became ubiquitous.

OTAs offer platforms where thousands of hotels, airlines, and car rental agencies aggregate their offerings, allowing consumers to search for competitive prices and book vacations or experiences in one place.

The OTA takes a commission, which the airline or hotel happily pays to increase their own exposure to potential customers. Booking Holdings has become the top public company in this space thanks to a slew of operational tailwinds, some of which have emerged in the last few years.

Structural Business Advantages

Booking Holdings has several unique advantages over competitors such as Expedia Group Inc. (NASDAQ: EXPE) and Airbnb Inc. (NASDAQ: ABNB). Some of these structural edges include:

Network Effects: Booking Holdings has tremendous network effects, with nearly 30 million properties listed on its marketplace. This type of supply breadth attracts more consumers to the network, further entrenching the company as the respected OTA leader.

Direct Traffic: Booking’s app and website drive more direct traffic than competitors, and the company relies less on advertising and paid Google search clicks.

Business Model Shift: The company’s shift from an agency model to a merchant model means it collects payment upfront rather than waiting to receive a commission from the hotel or airline. This model helps improve unit economics and gives the company better control over its cash flow.

Additionally, BKNG remains compelling on valuation grounds. Despite smashing earnings expectations in Q4 2025, including 16% year-over-year (YOY) revenue growth, the stock trades at just 16X forward earnings, with a price-to-earnings-growth ratio just above 1X and 20% net margins. With $27 billion in annual revenue, investors are getting an industry-best stock at a historical discount. Another tailwind comes from the stock’s recent 25-to-1 split, which cut the price down significantly from over $4,000 per share. While most brokerages offer fractional shares, a price exceeding $4,000 did create a mental friction point for investors with smaller or more traditional accounts.

Reasons to Be Bearish on Booking Holdings

Large-cap stocks rarely drop 20% without a significant reason, and an investment in BKNG shares here isn’t a sure thing. Here are three reasons investors have gotten bearish on the stock:

Cyclical Industry Structure: Travel is part of the consumer discretionary sector, and trips are one of the first things consumers cut during economic slowdowns. Rising unemployment or inflation could dent travel demand, plus the threat of geopolitical risk continues to loom.

Headwinds From Fuel Surge: Fallout from the Iran war is likely to last long beyond the conflict. Fuel disruptions are already affecting major airlines, with many raising baggage fees to offset costs. An oil surge hurts travel in two ways: flights become more expensive, and consumers pull back due to their own strained budgets.

AI Disruption Stealing Market Share: Booking Holdings has decreased its reliance on Google search, but Alphabet Inc. (NASDAQ: GOOGL) is fighting back with AI tools like Overviews. Travel agents powered by AI bots risk cutting OTAs out of the picture, and this risk is ascending faster than Booking Holdings can create its own AI platforms.

Despite Headwinds, Chart Shows Increasing Bullish Activity

Booking Holdings has little risk of losing its status as the top dog in the OTA industry; it's the threats of AI disruption and economic turbulence that have been roiling the stock lately. However, it appears the worst of the oil surge has been priced in, and AI disruption remains a long-term threat that internal tools can still offset. BKNG stock is also beginning to show bullish signs of life on the daily chart.

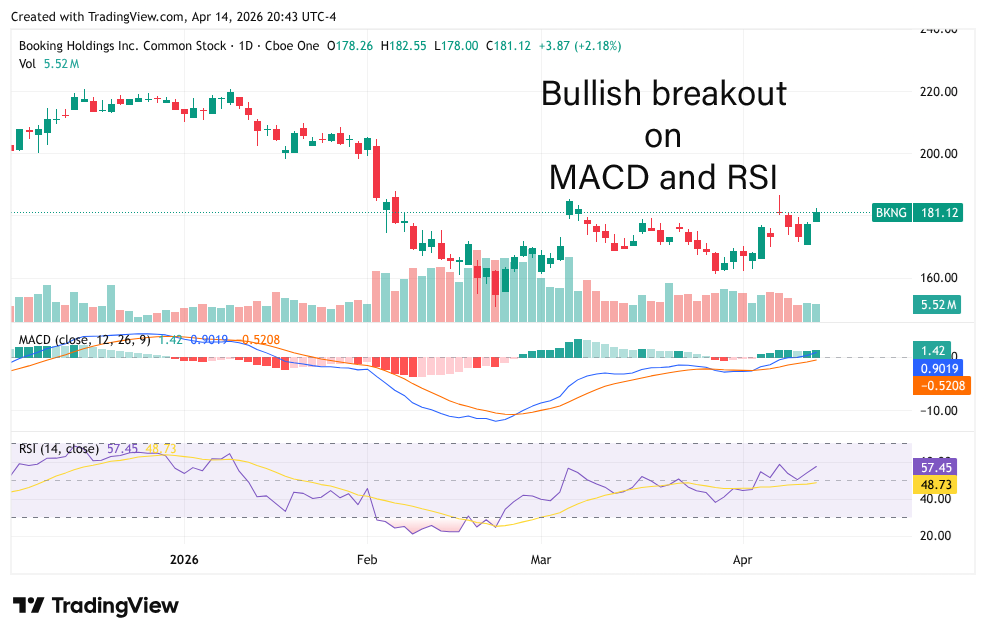

The stock has finally retaken its 50-day simple moving average (SMA), breaking above this crucial level for the first time since January. A floor appears to have been set around the $160 level, and the stock has been making higher lows since hitting bottom in February.

The bullish momentum was confirmed by two separate technical indicators, the Moving Average Convergence Divergence (MACD) and the Relative Strength Index (RSI). The MACD performed a bullish crossover in late February and has been showing brewing upward momentum ever since. And the RSI recently popped back over 50, which is generally considered the level where buyers begin to outweigh sellers. The fundamentals may show a conflicting picture, but the technical signs point to a reversal of this 20% decline.

Where Should You Invest $1,000 Right Now?

Before you make your next trade, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis.

Our team has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and none of the big name stocks were on the list.

They believe these five stocks are the five best companies for investors to buy now...

The article "Booking Holdings Down 15%, Is It Time to Buy?" first appeared on MarketBeat.

/Super%20Micro%20Computer%20Inc%20HQ%20photo-by%20Tada%20Images%20via%20Shutterstock.jpg)

/Microsoft%20logo%20on%20building%20by%20franz12%20via%20iStock.jpg)

/Microsoft%20Corporation%20logo%20on%20sign-by%20Jean-Luc%20Ichard%20via%20iStock.jpg)