Let’s dig into the relative performance of CVS Health (NYSE:CVS) and its peers as we unravel the now-completed Q4 health insurance providers earnings season.

Upfront premiums collected by health insurers lead to reliable revenue, but profitability ultimately depends on accurate risk assessments and the ability to control medical costs. Health insurers are also highly sensitive to regulatory changes and economic conditions such as unemployment. Going forward, the industry faces tailwinds from an aging population, increasing demand for personalized healthcare services, and advancements in data analytics to improve cost management. However, continued regulatory scrutiny on pricing practices, the potential for government-led reforms such as expanded public healthcare options, and inflation in medical costs could add volatility to margins. One big debate among investors is the long-term impact of AI and whether it will help underwriting, fraud detection, and claims processing or whether it may wade into ethical grey areas like reinforcing biases and widening disparities in medical care.

The 12 health insurance providers stocks we track reported a slower Q4. As a group, revenues beat analysts’ consensus estimates by 0.8% while next quarter’s revenue guidance was in line.

While some health insurance providers stocks have fared somewhat better than others, they have collectively declined. On average, share prices are down 1.8% since the latest earnings results.

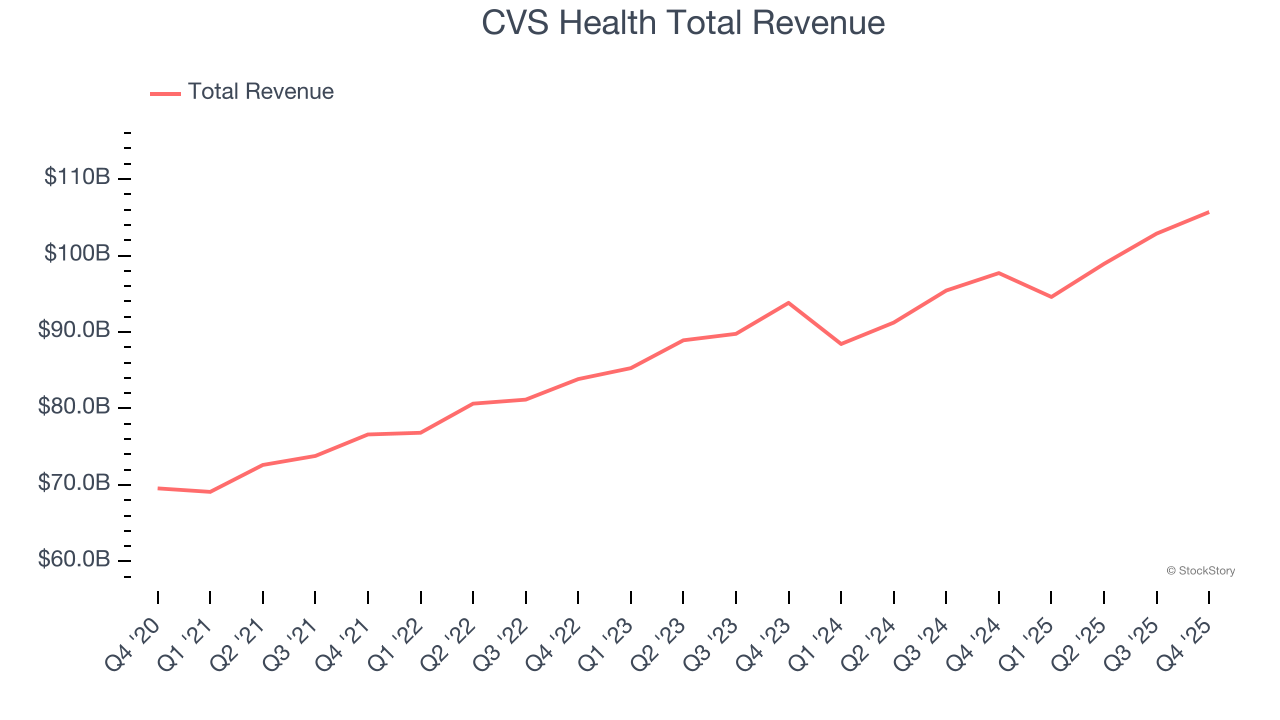

CVS Health (NYSE:CVS)

With over 9,000 retail pharmacy locations serving as neighborhood health destinations across America, CVS Health (NYSE:CVS) operates retail pharmacies, provides pharmacy benefit management services, and offers health insurance through its Aetna subsidiary.

CVS Health reported revenues of $105.7 billion, up 8.2% year on year. This print exceeded analysts’ expectations by 2%. Overall, it was a satisfactory quarter for the company with a decent beat of analysts’ revenue estimates but a slight miss of analysts’ full-year EPS guidance estimates.

CEO Commentary"Our fourth quarter and full-year results demonstrate the progress we are making in transforming the health care experience with our unique collection of businesses. From lowering drug prices, to improving navigation of health care, to being the front door of care across our country, we are well positioned to achieve our ambition to be the most trusted health care company in America."

Interestingly, the stock is up 1.2% since reporting and currently trades at $76.66.

Is now the time to buy CVS Health? Access our full analysis of the earnings results here, it’s free.

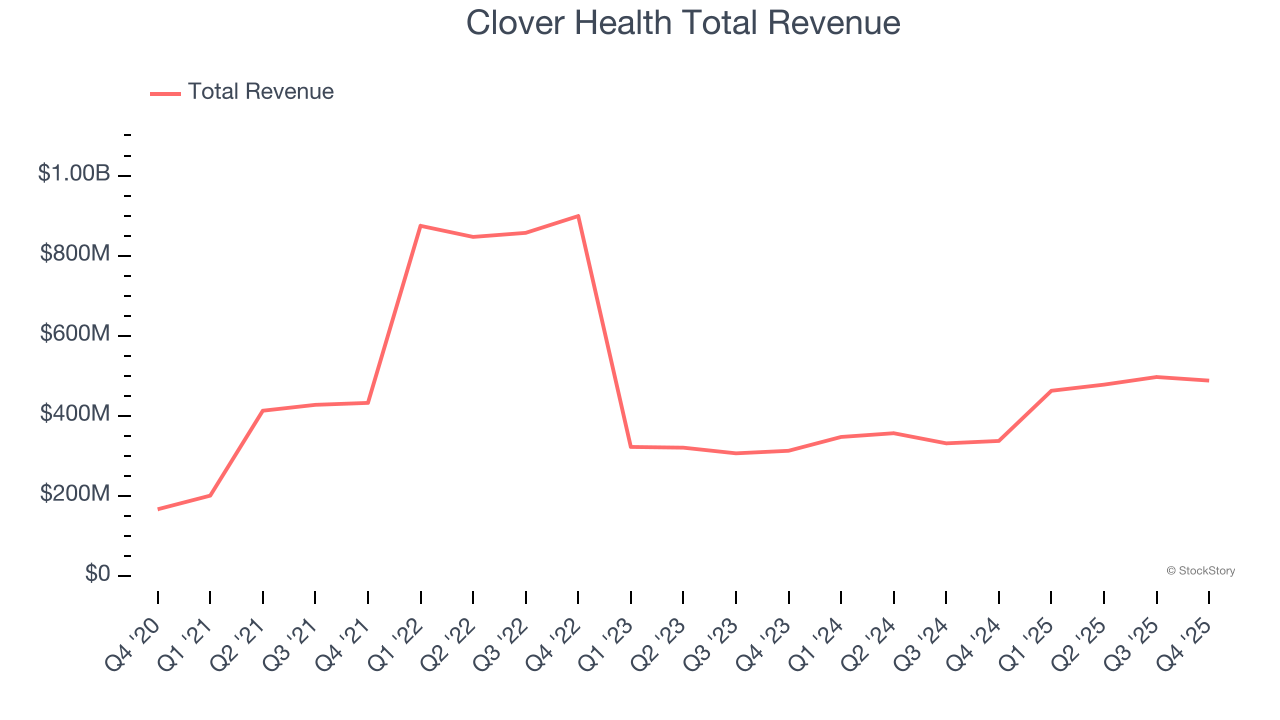

Best Q4: Clover Health (NASDAQ:CLOV)

Founded in 2014 to improve healthcare for America's seniors through technology, Clover Health (NASDAQ:CLOV) provides Medicare Advantage plans for seniors with a focus on affordable care and uses its proprietary Clover Assistant software to help physicians manage patient care.

Clover Health reported revenues of $487.7 million, up 44.7% year on year, outperforming analysts’ expectations by 4.4%. The business had a strong quarter with a solid beat of analysts’ revenue estimates and EPS in line with analysts’ estimates.

Clover Health delivered the biggest analyst estimates beat and fastest revenue growth among its peers. The company added 4,577 customers to reach a total of 113,803. However, the results were likely priced into the stock as it’s traded sideways since reporting. Shares currently sit at $2.16.

Is now the time to buy Clover Health? Access our full analysis of the earnings results here, it’s free.

Weakest Q4: Molina Healthcare (NYSE:MOH)

Founded in 1980 as a provider for underserved communities in Southern California, Molina Healthcare (NYSE:MOH) provides managed healthcare services primarily to low-income individuals through Medicaid, Medicare, and Marketplace insurance programs across 21 states.

Molina Healthcare reported revenues of $11.38 billion, up 8.3% year on year, exceeding analysts’ expectations by 3.7%. Still, it was a softer quarter as it posted full-year revenue and EPS guidance estimates.

As expected, the stock is down 15.8% since the results and currently trades at $148.92.

Read our full analysis of Molina Healthcare’s results here.

UnitedHealth (NYSE:UNH)

With over 100 million people served across its various businesses and a workforce of more than 400,000, UnitedHealth Group (NYSE:UNH) operates a health insurance business and Optum, a healthcare services division that provides everything from pharmacy benefits to primary care.

UnitedHealth reported revenues of $113.2 billion, up 12.3% year on year. This result met analysts’ expectations. More broadly, it was a slower quarter as it recorded full-year revenue guidance missing analysts’ expectations and revenue in line with analysts’ estimates.

The stock is down 9.9% since reporting and currently trades at $316.85.

Read our full, actionable report on UnitedHealth here, it’s free.

Humana (NYSE:HUM)

With over 80% of its revenue derived from federal government contracts, Humana (NYSE:HUM) provides health insurance plans and healthcare services to approximately 17 million members, with a strong focus on Medicare Advantage plans for seniors.

Humana reported revenues of $32.64 billion, up 11.8% year on year. This number surpassed analysts’ expectations by 1.8%. Taking a step back, it was a slower quarter as it logged a significant miss of analysts’ full-year EPS guidance estimates.

The company added 7,500 customers to reach a total of 15 million. The stock is up 10.9% since reporting and currently trades at $201.

Read our full, actionable report on Humana here, it’s free.

Market Update

Late in 2025 into early 2026, there was hand wringing around artificial intelligence. For software companies, the fear was that AI would erode pricing power and compress margins as new tools made it easier to replicate what once required expensive enterprise platforms. Crypto investors had their own version of the same anxiety: if AI agents could trade, allocate capital, and manage wallets autonomously, what exactly was the long-term value of today’s crypto infrastructure?

These concerns triggered a noticeable rotation away from these sectors and into safer havens. But markets rarely dwell on one narrative for long. Spring 2026 came, and the focus shifted abruptly from technological disruption to geopolitical risk. The US’ conflict with Iran became the dominant driver of market psychology, and when geopolitics takes center stage, the script changes quickly. Investors stop debating growth rates and start worrying about oil supply, inflation, and global stability.

Want to invest in winners with rock-solid fundamentals? Check out our Top 5 Growth Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.

/Advanced%20Micro%20Devices%20Inc_%20office%20sign-by%20Poetra_RH%20via%20Shutterstock.jpg)

/CPU%20Chip.jpg)

/Super%20Micro%20Computer%20Inc%20HQ%20photo-by%20Tada%20Images%20via%20Shutterstock.jpg)