/Advanced%20Micro%20Devices%20Inc_%20logo%20and%20chart%20data-by%20Poetra_%20RH%20via%20Shutterstock.jpg)

Cathie Wood has been active in semiconductors this spring, and Advanced Micro Devices (AMD) is the most spotlighted stock within those moves. Ark Invest bought AMD shares in February, then turned around and sold about 44,446 shares worth roughly $10.5 million in April. That kind of trading says more about portfolio management and risk control than a clean thesis call. It also comes after a rougher stretch for high-beta growth names, where investors have been rotating in and out of chip stocks fast.

The Ark Innovation ETF (ARKK) has also had a sharp rebound, finishing 2025 up by about 35%. Additionally, while the S&P 500 ($SPX) has climbed about 3% year-to-date (YTD) and 30% over the past 52 weeks, ARKK is seeing a much bumpier ride, climbing 66% for the past 12 months but trading relatiely flat YTD.

Against that backdrop, Wood’s AMD stock trim looks like a timing move, not a verdict on the company.

AMD Strengthens Position as AI Chip Leader

AMD is a major chipmaker known for its CPUs and GPUs, from Ryzen and EPYC to Radeon and Instinct. It makes processors for PCs, consoles, and servers, including AI accelerator chips. CEO Lisa Su has guided the firm into AI infrastructure. In 2025, AMD also broke revenue and profit records, riding trends like cloud and AI. It’s a semiconductor bellwether with a history of surging when AI spending heats up.

AMD stock has had a great past year. Shares have surged 169% over the past 12 months on the heels of AI enthusiasm, including strong chip demand and major deals with hyperscalers. However, so far this year — due to geopolitical tensions and broader market pressure — the stock has gained only 19% YTD. Technically, AMD is also trading above its 50-day and 200-day moving averages after a recent bounce, which is a bullish sign.

Valuation adds another layer to the story. The trailing price-to-earnings (P/E) ratio of 75.7 times is about double the semiconductor industry median, reflecting high expectations. At the same time, AMD's forward P/E-growth (PEG) ratio of around 0.92 times is below the sector median of 1.2 times, suggesting its projected growth may be priced more conservatively. In simple terms, AMD appears to be somewhere between fairly valued and slightly expensive, depending on how investors weigh its growth outlook against current pricing.

AMD Caps 2025 With Record-Breaking Q4

AMD ended 2025 on a strong note, posting record fourth-quarter results amid demand for its data-center chips and Ryzen processors. Revenue came in at $10.27 billion, up 34% from a year earlier, helped by solid growth in the data-center, client, and gaming businesses.

Data-center sales reached $5.38 billion, compared with $3.86 billion a year ago, while client CPUs brought in $3.09 billion and gaming GPUs added $843 million. Gross margin stayed healthy at about 54% on a GAAP basis. Operating expenses rose as AMD kept investing, but operating profit still doubled to about $1.75 billion.

Net income jumped to $1.51 billion, or $1.53 per share on an adjusted basis, above expectations. The company also generated about $2.3 billion in operating cash flow and roughly $2.1 billion in free cash flow after modest capital spending. AMD ended the year with $5.56 billion in cash, up from $3.81 billion a year earlier.

CEO Lisa Su said that 2025 was a "defining year" for the company. “We are entering 2026 with strong momentum across our business, led by accelerating adoption of our high-performance EPYC and Ryzen CPUs and the rapid scaling of our data center AI franchise,” Su continued. CFO Jean Hu added that the firm “achieved record non-GAAP operating income and free cash flow” in 2025 while investing for growth.

Looking ahead, AMD forecasts Q1 2026 revenue of $9.8 billion, representing growth of about 32% YOY. That reflects continuing momentum, and assumes $100 million from China Instinct GPU sales. AMD did not provide full-year 2026 targets, but analysts expect revenue of roughly $45 billion and continued profit growth.

Recent Developments

AMD has been busy this year. In mid-March, the company signed a memorandum of understanding (MOU) with Samsung to supply HBM4 for its upcoming MI455X AI GPU. This secures high-bandwidth memory for the next-gen Instinct chips, a boost for AMD’s GPU roadmap.

On the customer side, AMD is rapidly winning cloud business. Eight of the top 10 hyperscalers now use AMD GPUs and its EPYC servers are scaling fast. EPYC cloud instances grew 50% in 2025. All these moves reinforce AMD’s push into AI infrastructure, not just consumer PCs.

What Do Analysts Say About AMD Stock?

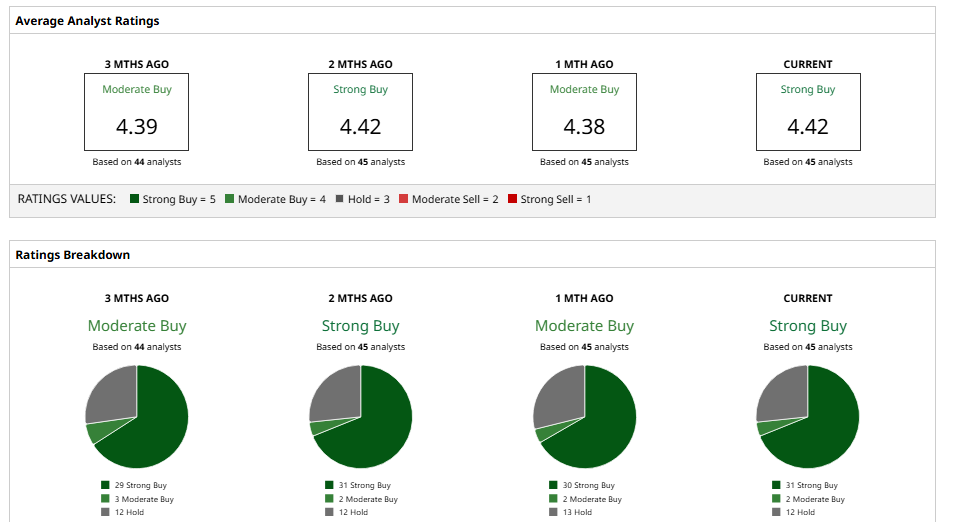

Wall Street analysts are very optimistic about AMD stock's growth prospects. The consensus rating is a “Strong Buy" based on 45 analysts with coverage. The average 12-month price target is $287.39, implying roughly 11% potential upside from current prices.

Analysts point out that AMD’s valuation has “reset” after recent weakness. Goldman Sachs notes that, while AMD’s P/E is below last year’s dizzying highs, the multiple is still far above the industry median. Meanwhile, some analysts believe investors are underestimating AMD’s growth. As one analyst wrote, the stock's forward PEG ratio trading below the sector median implies that the market hasn’t fully priced in AMD’s EPS growth.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/AI%20technology%20concept%20by%20NMStudio789%20via%20Shutterstock.jpg)