/The%20CoreWeave%20logo%20displayed%20on%20a%20smartphone%20screen_%20Image%20by%20Robert%20Way%20via%20Shutterstock_.jpg)

AI infrastructure stocks have had a rough time in 2026, with CoreWeave (CRWV) right in the middle of it. Based in Livingston, New Jersey, the cloud computing company, which rents out GPU-heavy data centers to AI developers, went public in March 2025 at $40 per share and quickly turned into one of the market's most talked-about names, climbing as high as $187 by June 2025.

Since then, CRWV stock has fallen 52% from that peak, hit by a disappointing fourth-quarter earnings miss, a softer-than-expected revenue outlook, and ongoing concerns about how long AI spending can stay this strong.

Even with the pullback, Ark Invest's Cathie Wood has been steadily adding to her position. Throughout February, Ark's exchange-traded funds bought CRWV stock nine times, picking up $49.43 million worth of shares. The buying continued into the spring. Between March 30 and April 1, Ark added more than 83,000 additional shares of CoreWeave valued at about $5.8 million, showing a clear pattern of repeated accumulation rather than a one-off trade.

Wood has built her reputation on buying into disruptive innovation when many others are selling. She did it with Tesla (TSLA) and Nvidia (NVDA). Now, Wood is doing it with CoreWeave. The question is: does Cathie Wood's conviction in this AI infrastructure play reflect a well-reasoned contrarian bet, or is she catching a falling knife?

CoreWeave’s Financial Pulse

CoreWeave is a specialized cloud infrastructure provider built for GPU-heavy AI work, including large-scale model training, inference, and other compute-intensive tasks that traditional cloud providers are not built to handle as efficiently.

CRWV stock has held up well despite recent volatility. The stock is up 100% over the past 52 weeks and 23% year-to-date (YTD), showing that investors are still willing to pay for its growth story.

That growth is clear in the numbers. CoreWeave closed fiscal 2025 with $5.13 billion in revenue, up 168% year-over-year (YOY), making it the “fastest cloud in history to reach $5 billion in annual revenue.” Q4 alone brought in $1.57 billion, topping analyst estimates.

The bottom line was a different story, however. The company reported a net loss of $1.17 billion for the year, with a diluted loss per share of $2.81. Operating income swung from a positive $113 million in Q4 2024 to a loss of $89 million in Q4 2025, showing how expensive this rapid expansion has been.

On an adjusted basis, the picture looks stronger. Adjusted EBITDA for 2025 came in at $3.09 billion, a 60% margin, while operating cash flow reached $3.06 billion. At the same time, CoreWeave spent $10.31 billion on capital expenditures, highlighting how heavily it is investing to keep up with AI demand. Total assets jumped to $49.3 billion, and total debt rose to around $21 billion, a level of leverage that investors need to watch closely.

What Is Powering CoreWeave’s Growth?

CoreWeave's $8.5 billion delayed draw term loan facility, known as the DDTL 4.0 Facility, is one of the biggest funding moves in the AI infrastructure space. It is rated A3 by Moody's and A (low) by DBRS, making it the first investment-grade financing backed by high-performance computing infrastructure and a specific customer contract. The setup allows CoreWeave to draw up to $7.5 billion at first before moving up to the full $8.5 billion as underlying assets stabilize, and the investment-grade rating helps the company secure capital at a lower cost as it pushes to scale its AI cloud platform.

Partnerships are adding another leg to that growth. Cline has integrated CoreWeave's W&B Inference directly into its ecosystem. This gives developers access to production-ready infrastructure built for training and inference, so autonomous coding agents can handle prompts, generate code, and run complex multi-step reasoning flows faster and at scale. As these agent-based AI workloads get more demanding, CoreWeave's low-latency setup becomes more important.

Hardware and platform upgrades are also key. At Nvidia's GPU Technology Conference, CoreWeave announced an expansion of its AI-native cloud platform, adding Nvidia HGX B300 to CoreWeave Cloud. Paired with new Weights & Biases features built for reinforcement learning and agent development, this upgrade puts CoreWeave in a strong position as the industry moves from one-off large model training toward ongoing RL and physical AI, where the next leg of compute demand is building.

How Analysts See the Road Ahead

For the current quarter, analysts are looking for an average loss per share of $1.18, compared with a loss of $0.60 in the same quarter a year ago, a sharp YOY drop of about 97%. However, they do see some gradual improvement ahead. For the next quarter, the consensus stimate is a loss of $0.99 versus a $0.54 loss last year, while full-year 2026 is pegged at –$4.16. In fiscal 2027, analysts believe this figure will improve 9% to –$3.79, pointing to a slow move toward healthier earnings as the business scales.

Deutsche Bank has also turned more positive on CoreWeave. The firm recently upgraded CRWV stock to “Buy” from “Hold” and raised its price target to $140, implying about 57% potential upside from current levels.

That call came after Nvidia's $2 billion investment and expanded partnership with CoreWeave to build more than five gigawatts (GWs) of AI factories by 2030. Analysts led by Brad Zelnick described the deal as strategic, noting that Nvidia’s access to land, power, and chips should help CoreWeave accelerate its buildout beyond the 2.9 GW backlog already lined up. The partnership could even pave the way for CoreWeave’s software to be included in Nvidia’s next-generation designs, which would support higher-margin cloud revenue.

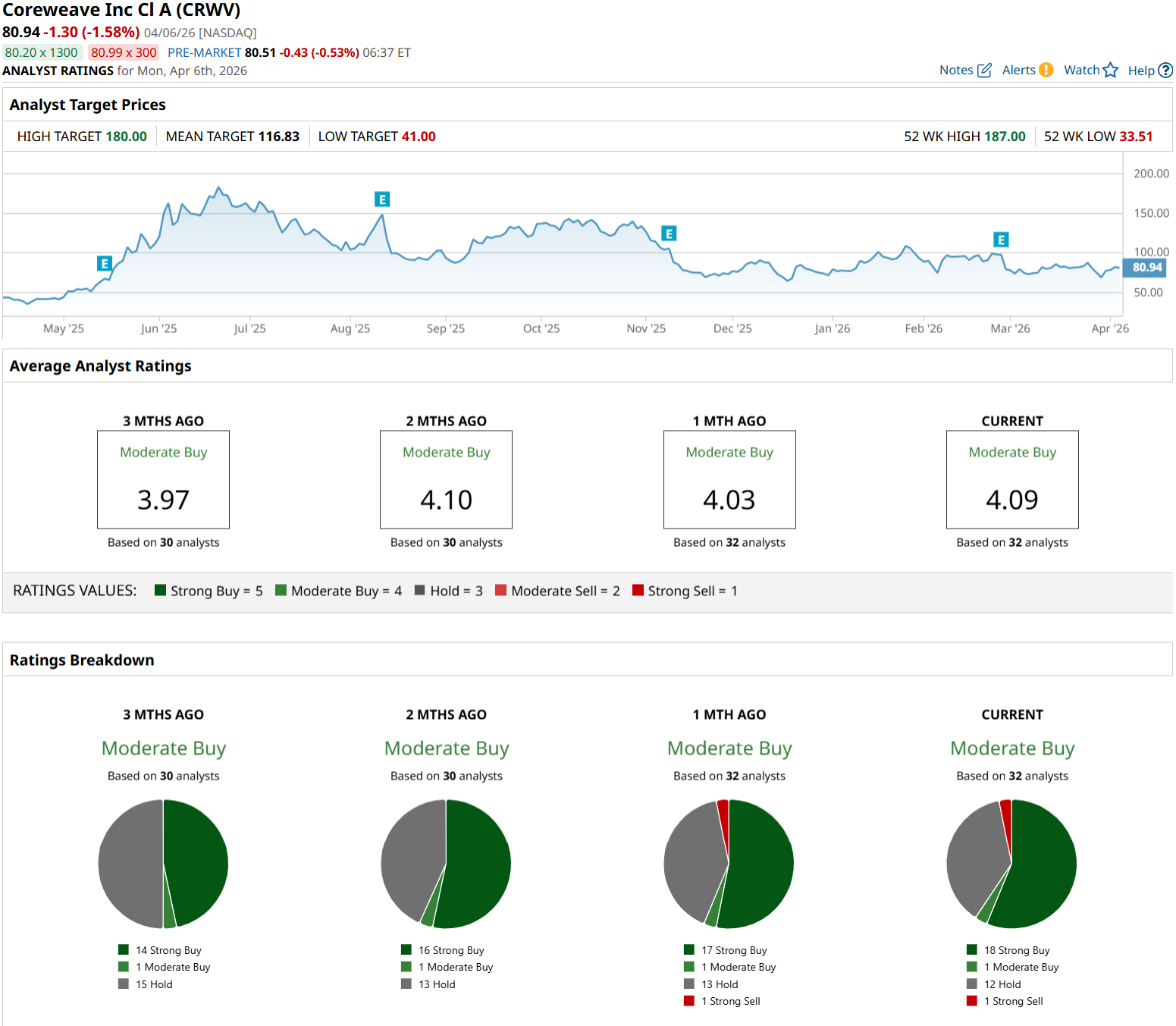

Broadly, Wall Street is leaning in the same direction. Based on 32 analysts covering CoreWeave, the stock has a consensus “Moderate Buy" rating. The average price target of $116.83 suggests roughly 31% potential upside from here.

Conclusion

For now, CoreWeave still looks like a stock for investors who can stomach serious volatility and think in years, not quarters. With scaling revenue, fat adjusted margins, and both Nvidia and Deutsche Bank leaning in its favor, the long-term setup arguably tilts bullish if management executes and AI demand holds up. However, widening GAAP losses, heavy leverage, and elevated expectations mean any stumble could hit CRWV stock hard. Accordingly, for investors who decide to follow Ark Invest in, a carefully sized, high-risk/high-upside satellite position probably makes more sense than a core holding.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Netflix%20open%20on%20tablet%20by%20rswebsols%20via%20Pixabay.jpg)

/Netflix%20on%20tv%20with%20remote%20by%20freestocks%20via%20Unsplash.jpg)