Investors head into Netflix’s (NFLX) Q1 2026 with a lot of clarity. The focus is on pricing, ad momentum, and content engagement. After the company walked away from the Warner Bros. (WBD) deal, there is no uncertainty regarding where the capital could be allocated. Granted, the acquisition could have been a catalyst, but now that there isn’t any capital overhang, investors can focus on the core business.

The company is planning to spend around $20 billion annually on content creation. After the disappointing guidance posted in the previous quarter, a high spend like this is worrying investors. Apart from this factor, the company is going strong, and investors hope the company will be able to deliver on the guidance provided in the previous quarter. Netflix closed the previous quarter at 325 million subscribers, who were content with what they saw on the platform, as showcased by the low churn rate. The firm has also been able to raise prices and monetize content without facing any significant disruption or backlash from subscribers.

About Netflix Stock

Netflix operates as an entertainment services provider. It provides live programming, television series, feature films, and documentaries in different languages and genres. The company also enables members to watch streaming content on various internet-connected devices, including digital video players, TVs, TV set-top boxes, and mobile devices. Netflix was founded in 1997 and is based in Los Gatos, California.

Netflix posted an impressive performance of over 5.4% so far this year, while the S&P 500 Index ($SPX) is down more than 3% during the same period. The index was under pressure mainly due to the Iran war, but Netflix has so far proven to be a better hold during these turbulent times.

Netflix continues to trade at a discount to its historic valuations. On a forward price-to-earnings basis, the company’s stock is at a 17% discount right now compared to its 5-year average, with a price-to-earnings multiple of 31.19 times. Interestingly, its forward price-to-cash flow ratio of 35.62 times is 71% below the 5-year average of 122.52 times. This is a huge discount that also showcases the firm has healthy cash flows to pay for its capital-intensive content creation.

Further, the consensus earnings growth rates are worth a look. The company is expected to grow at over 23% this year and the next. The growth rate goes down after that, but Wall Street can hardly price in the type of content that will be popular so far into the future.

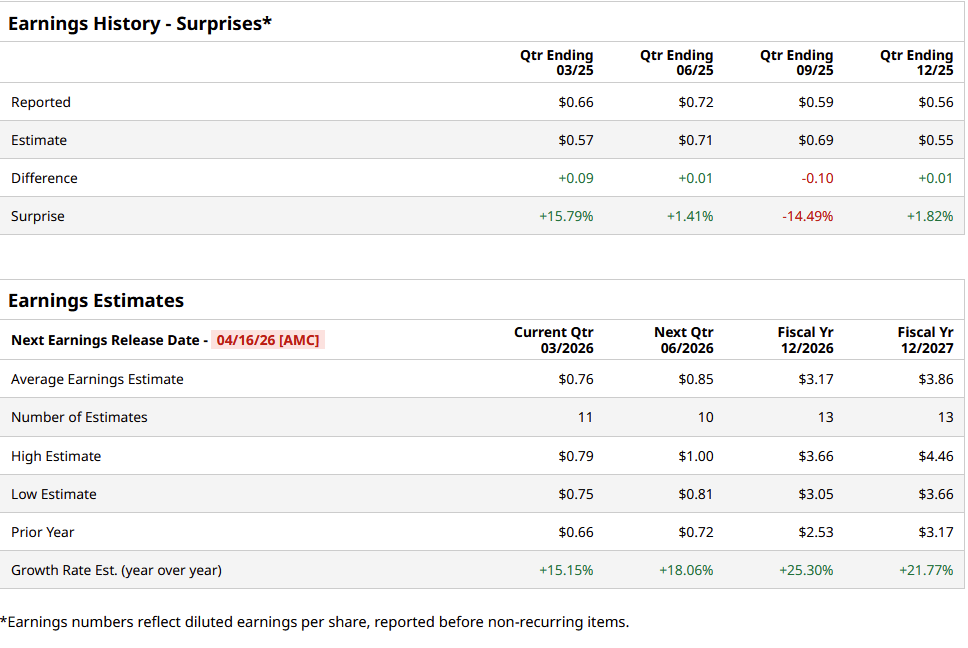

Netflix Posts Double-Digit Revenue Growth

Netflix reported its fourth-quarter FY 2025 earnings on Jan. 20. For the fourth quarter, net income reached $2.42 billion, with revenue increasing 18% year-over-year (YOY). For FY 2025, the company posted a revenue growth of 16% and an operating profit growth of around 30%. Advertising revenue rose 2.5 times in 2025 and is projected to double again in 2026. In the second half of 2025, total viewing hours were up 2% YOY.

The company expects its 2026 revenue to be in the range of $50.7 billion and $51.7 billion, representing around 14% increase from last year. The firm is targeting an operating margin of 31.5% in 2026. Netflix is scheduled to release its first-quarter FY 2026 earnings on April 16.

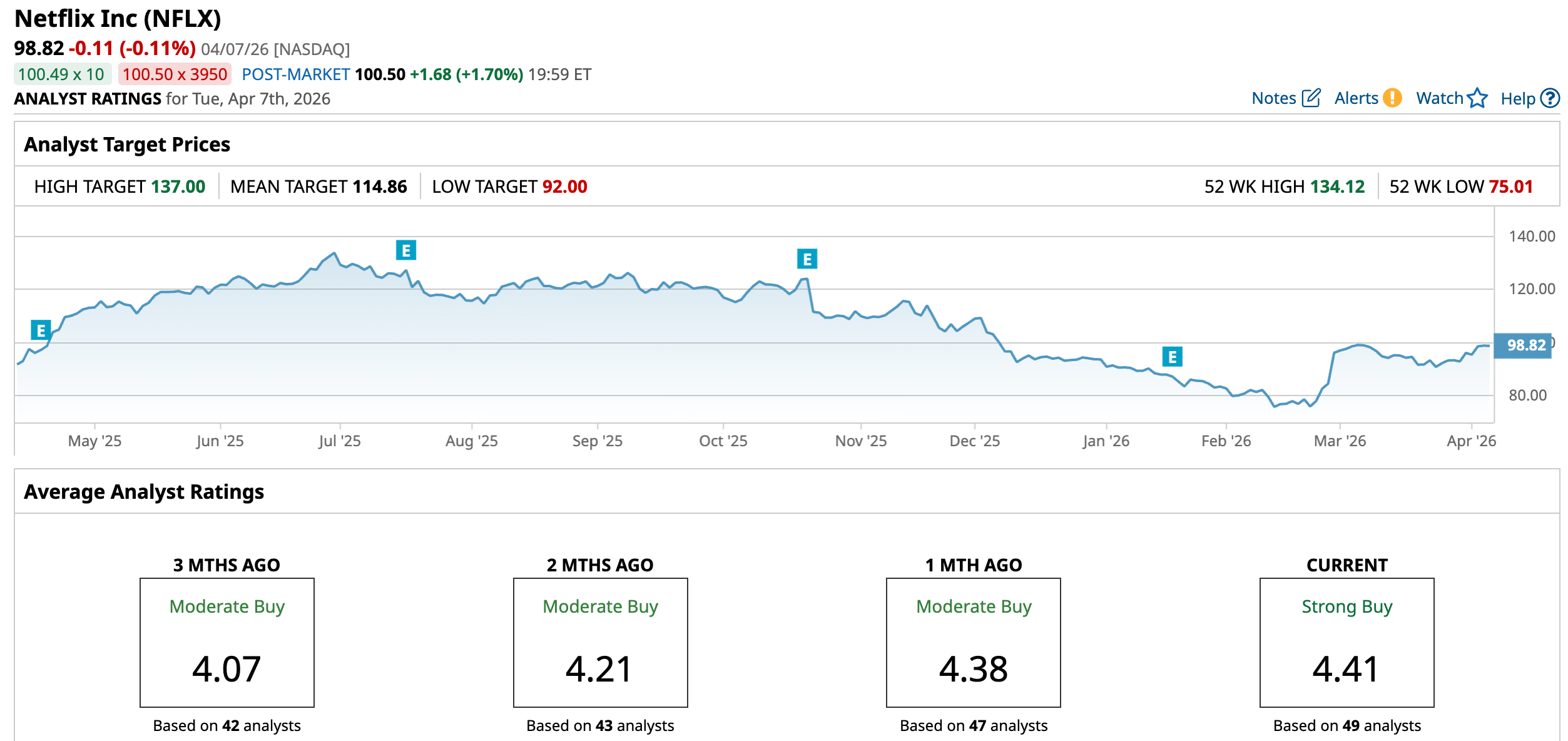

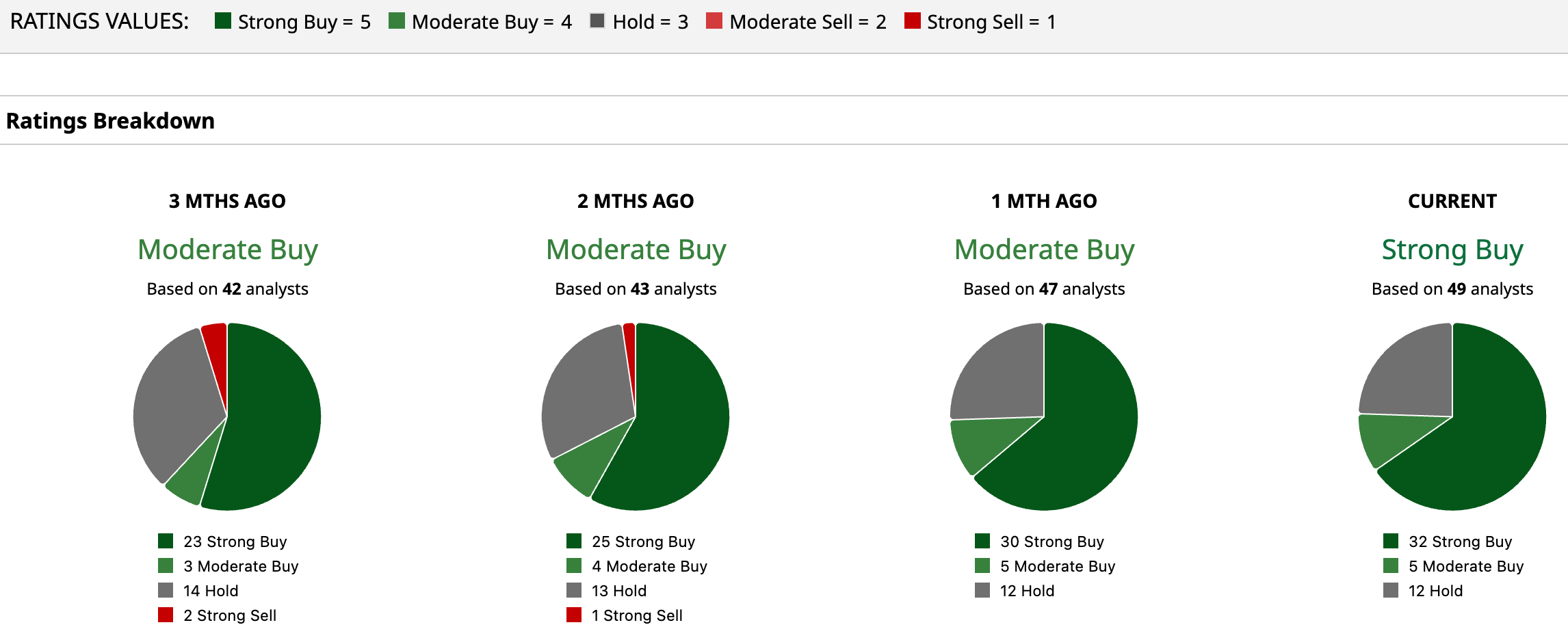

What Are Analysts Saying About Netflix Stock

Netflix received an upgrade ahead of its Q1 earnings report. On April 5, Goldman Sachs analyst Eric Sheridan upgraded the stock from “Neutral” to “Buy.” He also increased the firm’s price target on the shares from $100 to $120. According to the research firm, the stock now offers a more favorable risk/reward profile after dropping 18% in the last six months. Barclays also reaffirmed a “Buy” rating on Netflix stock, along with a $108 price target on April 1.

The stock is currently covered by 49 Wall Street analysts. It has strong analyst support, with a consensus “Strong Buy” rating. The mean price target of $114.86 reflects 16.23% upside from the current levels. The most bullish estimate indicates that the stock could surge to $137, reflecting more than 38.6% potential upside.

On the date of publication, Jabran Kundi did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20concept%20image%20showing%20a%20lightbulb%20with%20planet%20earth%20in%20a%20mossy%20green%20background%20by%20Capt_Pic%20via%20Shutterstock.jpg)

/The%20CrowdStrike%20logo%20on%20an%20office%20building%20by%20bluestork%20via%20Shutterstock.jpg)

/Friends%20choosing%20a%20movie%20on%20a%20streaming%20service%20by%20Stock-Asso%20via%20Shutterstock.jpg)