/Tesla%20Inc%20tesla%20by-%20Iv-olga%20via%20Shutterstock(1).jpg)

Tesla (TSLA) released its Q1 2026 deliveries on Thursday, April 2. Markets had somber expectations from the company, but it failed to clear even the low bar, with deliveries coming in at 358,023 while consensus estimates called for the number to be around 370,000.

The deliveries did rise 6% year-over-year (YoY), but the increase came from a lower base, as Tesla’s Q1 2025 deliveries had tumbled 13%. The company was conducting a Model Y refresh during the quarter, which affected production. Moreover, there was significant backlash against CEO Elon Musk back then amid his association with the Department of Government Efficiency (DOGE).

However, while Tesla’s deliveries rose by single digits in Q1, its production surpassed deliveries by 50,363 units, which marked the highest-ever inventory buildup for the company, which has been battling tepid demand for over two years now. Notably, Tesla’s deliveries fell YoY in both 2025 and 2024, and while deliveries rose in Q1 2026, it would be a tall ask for the company to report an annual increase this year.

The macro environment looks challenging for Tesla and other electric vehicle (EV) players. Stateside, the expiration of the EV tax credit is expected to weigh heavily on demand for at least the next few quarters. In China, which is Tesla’s biggest market after the U.S., competition remains elevated.

Meanwhile, while no one really expected wonders from Tesla’s EV deliveries, the company’s energy business, which reported record deployments in Q4 2025, also saw a decline in deployments in Q1. The stock plunged 5% following the Q1 update, which is testimony to the fact that while Tesla has been positioning itself as an artificial intelligence (AI) play, its automotive business still matters to the market.

TSLA Stock Forecast

Sell-side analysts weren’t too perturbed by Tesla’s Q1 delivery miss, and William Blair analyst Jed Dorsheimer said that the team wasn’t “surprised” as Tesla “is actively sacrificing its EV business in favor of a fully autonomous future.” Notably, Tesla has ended the production of Model S and X as it prepares to retool the Fremont factory to produce Optimus humanoid.

These two models, anyway, accounted for a low single-digit percentage of Tesla’s total deliveries, and the bulk of the sales came from the Model 3 and Model Y. The company is next focusing on the Cybercab, whose deliveries are set to commence later this year.

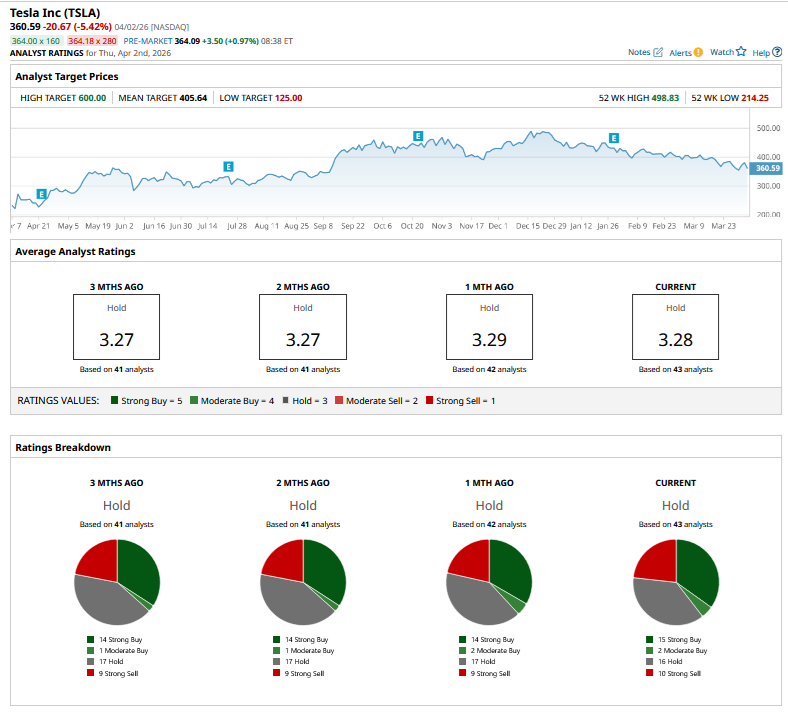

Wedbush analyst Dan Ives, who is among the most prominent Tesla bulls, said that while Tesla’s Q1 deliveries were “underwhelming,” they did not come as a “shock” given the state of the EV industry and the company’s focus on AI. Ives, however, maintained his $600 target price on TSLA, which happens to be the Street high.

Baird and Truist did lower their target prices following the report, with the latter cutting it from $438 to $400, but markets aren’t really losing sleep over the delivery miss as investors look ahead to AI products like robotaxis and Optimus. Overall, TSLA remains as divisive a stock as it has been and has a consensus rating of “Hold” with a mean target price of $405.64.

Should You Buy the Dip in TSLA Stock or Sell Instead?

I have always maintained that the automotive business is quite important for Tesla, as first, it provides the largesse that the company can then plow into new ventures, and second, losing out in the EV race raises doubt over Tesla’s ability to compete with Chinese companies in humanoids.

However, the new businesses would start to become increasingly important for Tesla as the company expands its robotaxi fleet and works towards full autonomy. Thereafter, Optimus might steal the show if the product comes anywhere close to the numbers Musk has forecast. On that note, Musk’s predictions should always be taken with more than a pinch of salt.

Among others, Tesla formally withdrew the forecast of 20 million annual deliveries by 2030 and has virtually given up on the 50% annual delivery growth guidance. Cybertruck numbers are also nowhere close to what Musk predicted, and for all practical purposes, that product has been a failure.

From projecting a million robotaxis by 2020 and perpetual promises of full autonomy “by the end of the year,” Tesla hasn’t been a shining example of meeting projections and has actually been a case of “overpromising and underdelivering.”

That said, Tesla has gradually expanded its target market with the unveiling of AI chips and, more recently, “Macrohard,” which is a joint project between the company and xAI, Musk’s startup. The company’s automotive business might also stabilize as legacy automakers in the U.S. have scaled back their EV bets. Moreover, the transition to EVs that took a backseat over the last few quarters might regain traction amid soaring gasoline prices.

I believe it makes sense to buy the dip in TSLA, particularly for those looking to play the physical AI story, even as the stock remains a high-risk bet given the not-so-cheap valuations and the multiple scenarios for the company's nascent AI business.

On the date of publication, Mohit Oberoi had a position in: TSLA. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Arista%20sing%20at%20headquarters%20of%20an%20American%20multinational%20technology%20company%20Arista%20Networks%20-%20Santa%20Clara%2C%20California%2C%20USA%20-%202020%20By%20MichaelVi.jpeg)

/AI%20(artificial%20intelligence)/AI%20Data%20Center%20by%20Gorodenkoff%20via%20Shutterstock.jpg)